Econosights

The outlook for tourism in Australia

Senior Economist Diana Mousina outlines the outlook for tourism in Australia.

9 min read

Key points

International tourist arrivals are still well below pre pandemic levels in Australia, which means that there is significant room for tourism to increase in 2023.

A booming tourism sector is positive for accommodation and recreation, hospitality and transport sectors and will help to offset the drags on the economy in 2023 from slowing consumer spending and declining residential construction.

The re-opening of China’s economy will help to boost tourism in Australia, as Chinese arrivals were the largest group of inbound overseas visitors into Australia pre pandemic. The tertiary education sector will also benefit from a rebound in Chinese student arrivals. Education arrivals will also benefit from a rebound in Chinese arrivals, However, it will take months for travel between China and Australia to return to normal levels.

Introduction

A boost to inbound tourism will be a positive growth driver for Australia in 2023, with increasing net exports helping to offset some of the negatives from a weakening consumer sector and a decline in housing construction. However, this won’t be enough to prevent Australian GDP growth from slowing this year. We expect GDP to rise by just under 1.5% over the year to December (compared to 4.6% year on year to December 2022). We outline the outlook for tourism in Australia in this Econosights.

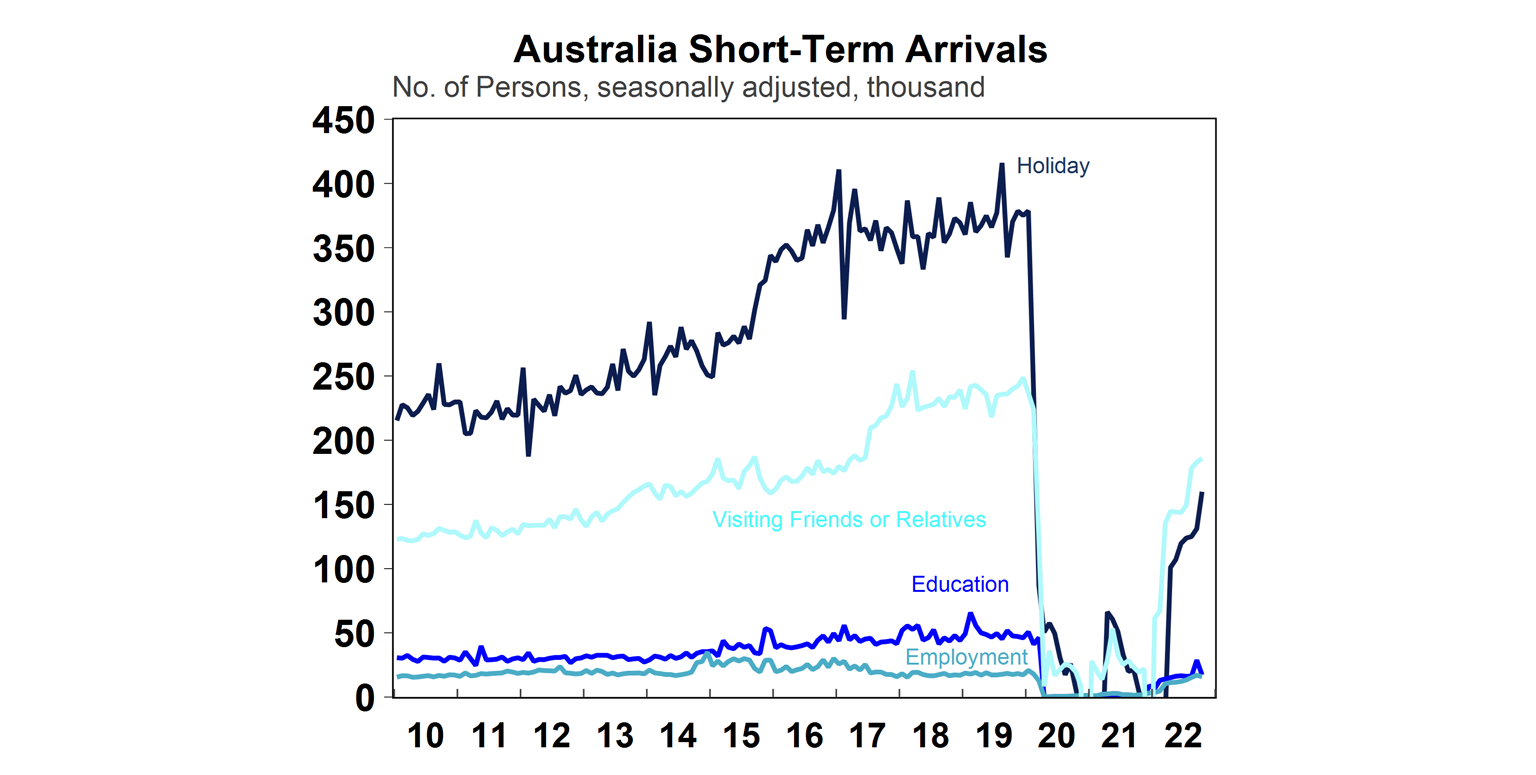

Inbound arrivals still not back to pre-Covid levels

Australian inbound short-term arrivals (those coming for less than a year) are still ~40% below pre-Covid levels (see the chart above) despite the international border being open for around a year. Visitor arrivals to see family/friends have recovered the most, followed by education arrivals but holiday travel is lagging behind and is still ~60% below its pre-Covid levels. This means that there is significant upside for holiday travel to rise over the next 1-2 years. Permanent migration is recovering back to its pre-Covid levels but for the purpose of the tourism sector (which this report concentrates on), we will focus on short-term tourism-related arrivals.

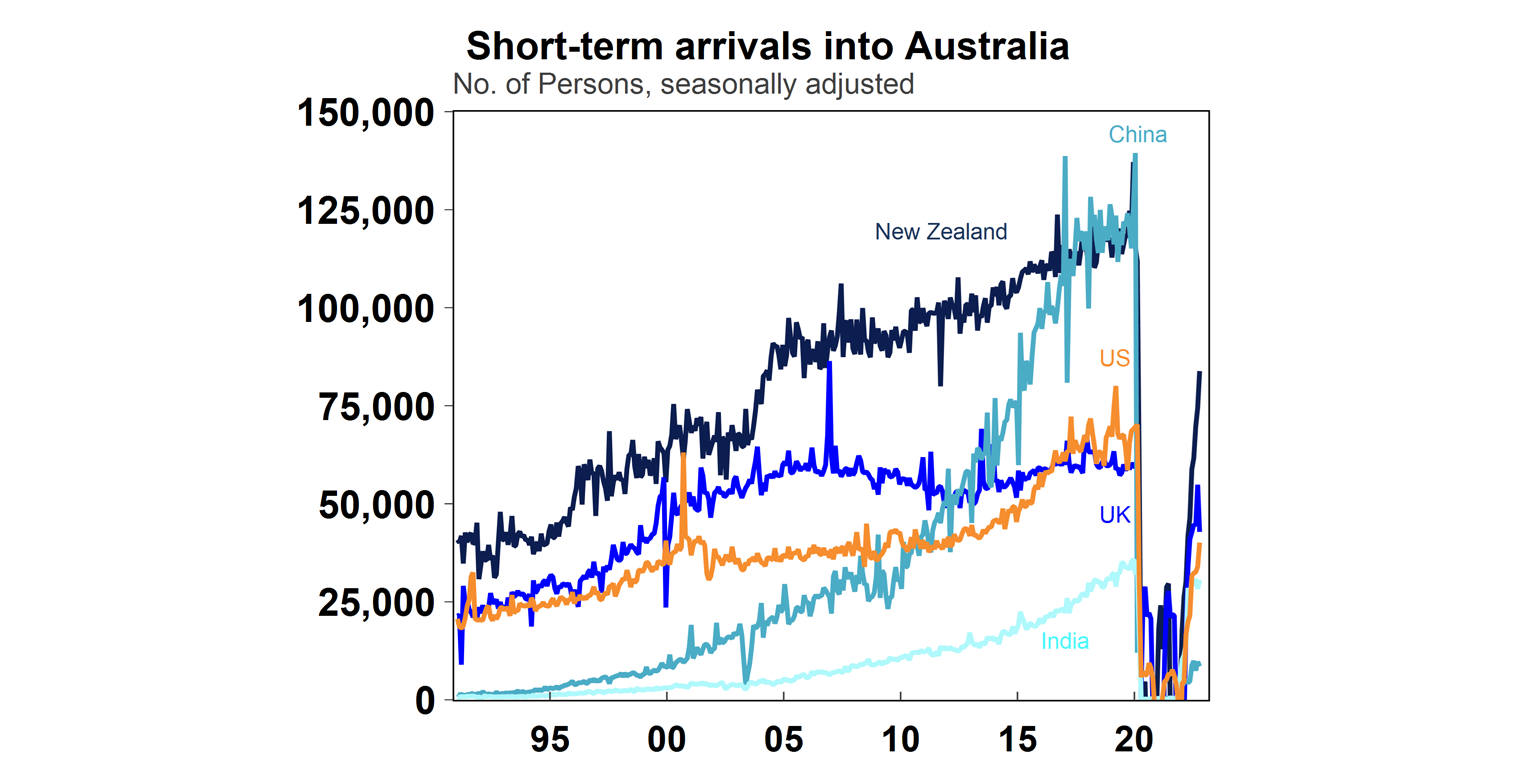

It has taken time for travel into Australia to recover because of: extensive Australian international border closures compared to the rest of the world, high inflation lifting airfare and travel costs and ongoing health concerns and logistic challenges related to Covid (like testing requirements). A shortage of Chinese arrivals since 2020 (which used to make up a decent 15% of Australian short term visitors) due to prolonged Covid-19 restrictions has also weighed on tourism in recent years. China is now re-opening its economy and reinstating inbound and outbound tourism which will lead to a pick-up in Chinese arrivals in coming months (although it will take a while to get Chinese arrivals back to “normal” due to initially limited airline capacity and health concerns about travelling).

The outlook for tourism in Australia

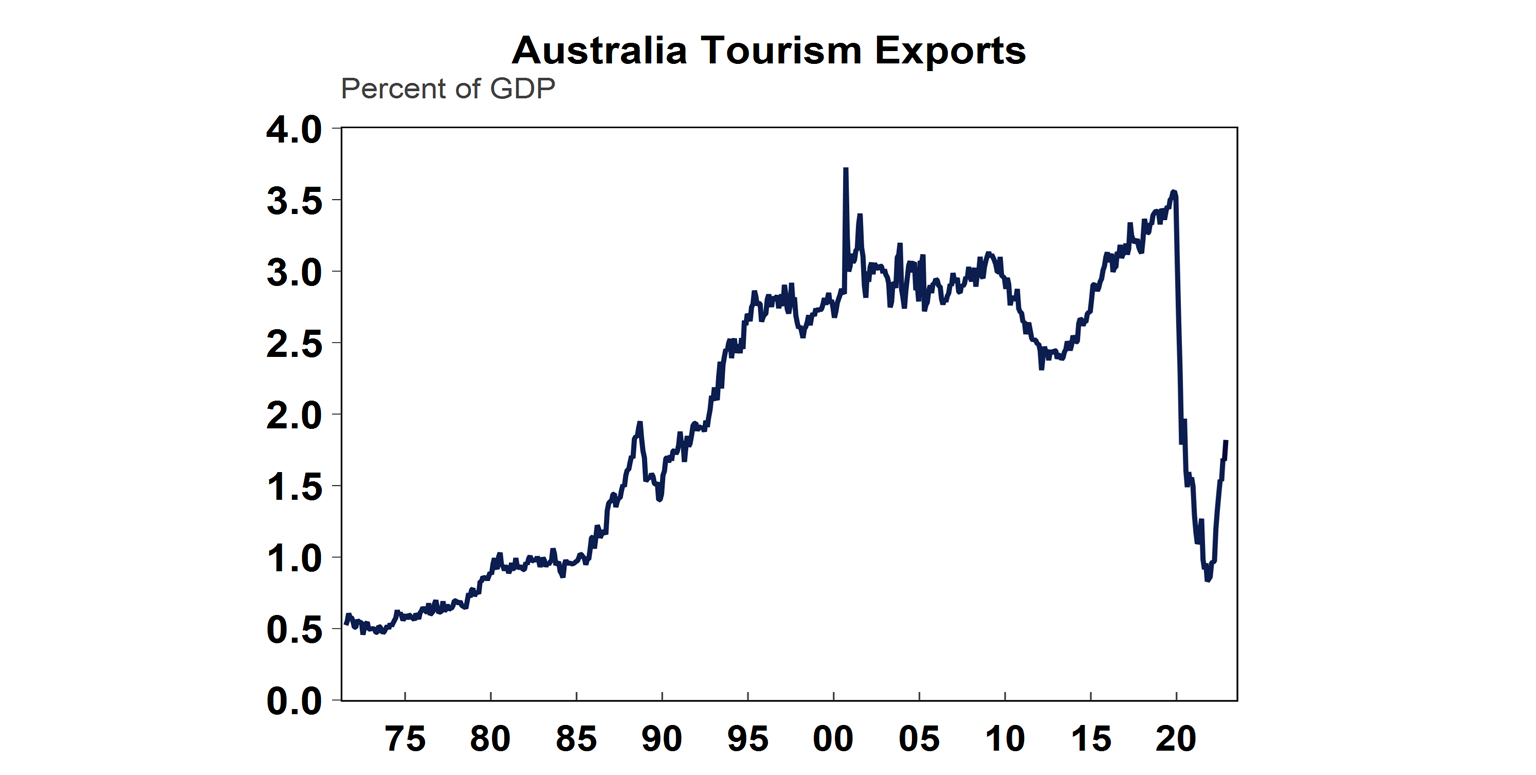

The value of tourism “exports” (people coming into Australia) is worth 1.8% of GDP (see the chart below), compared to 3.5% pre-pandemic, which leaves significant room for tourism to positively contribute to GDP this year (if tourism went back to pre-Covid levels it could add more than 1 percentage points to GDP growth in 2023). Tourism imports (or Australians going overseas) is considered an outflow and works against rising tourism exports but offshore travel may be more constrained this year as consumers feel the strain of rising mortgage repayments, a decline in cash savings and a lift in the unemployment rate.

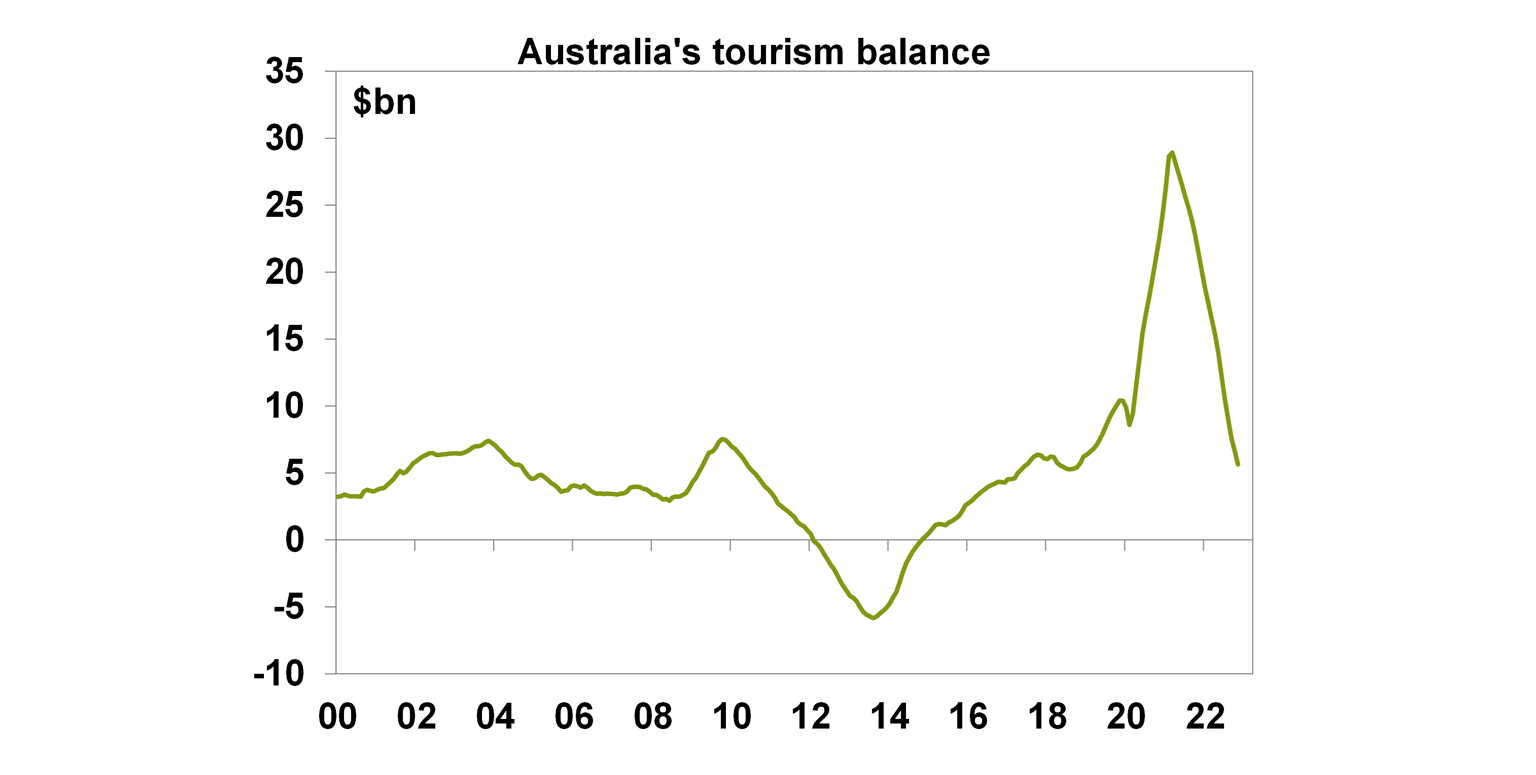

Australia’s tourism balance improved during the pandemic because outbound tourism (Australians spending money overseas) fell by more than the value of inbound tourism (see the chart below). The value of the tourism balance is now declining again as Australians are travelling offshore again.

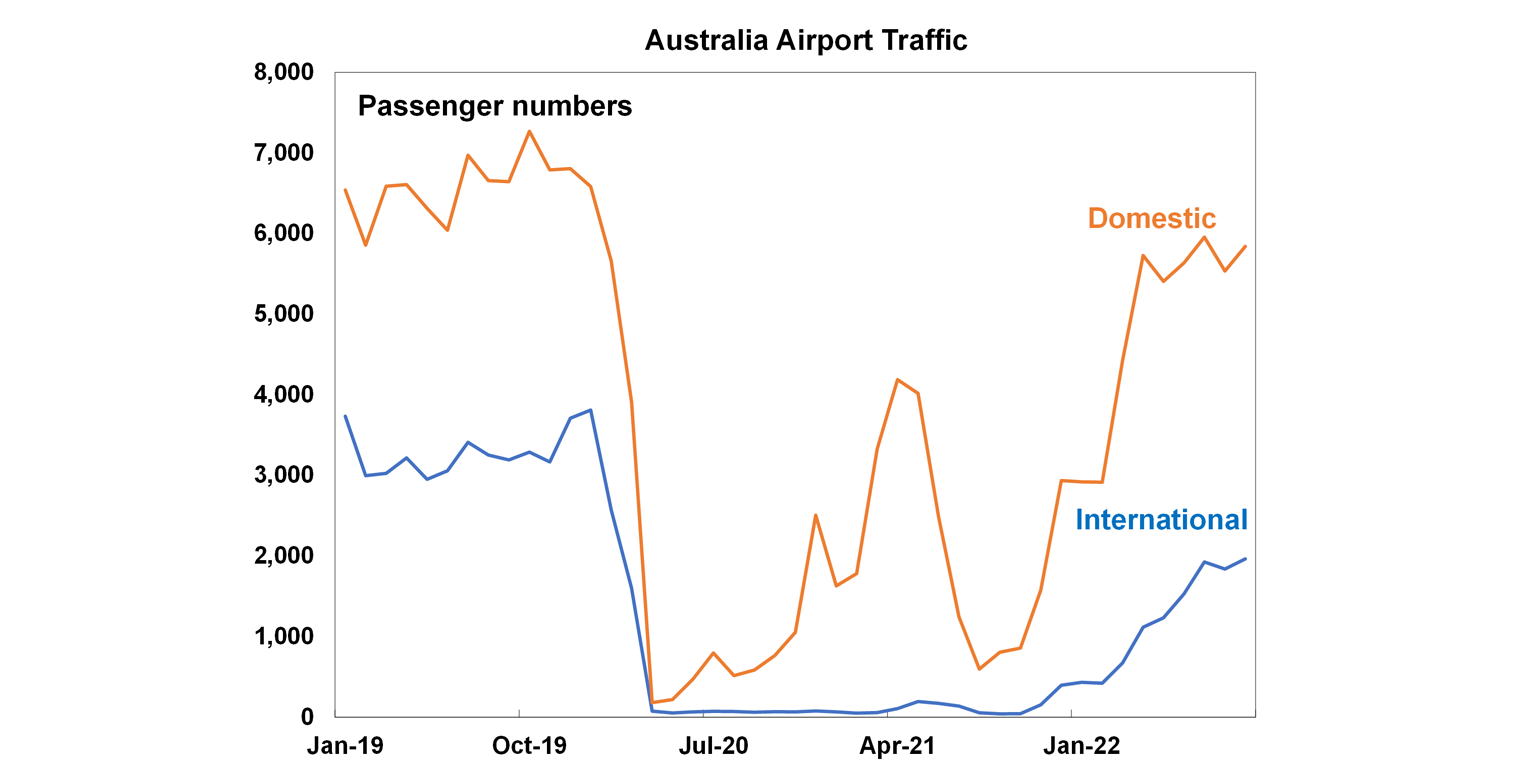

Closed international borders meant that Australians had no choice but to travel domestically which also boosted the value of the domestic tourism industry. Domestic tourism benefited significantly from closed borders in 2020/21, with domestic air travel now close to its pre-Covid levels. International travel is still well below its pre-Covid levels (see the chart below for domestic and international airport traffic). International airport traffic will rise further this year but it may be a while until it gets back to its pre-Covid levels, for example, Australia’s main tourism body, Tourism Research Australia, anticipates arrivals to only get back to pre-Covid levels by 2025.

So on balance, the resumption of arrivals into Australia is a small benefit to the Australian economy, but it won’t be enough to prevent GDP growth from slowing this year as due to some of the larger drags on the economy (a weakening in consumer spending and a small negative drag from housing construction). We expect GDP growth to rise by just under 1.5% over the year to December.

Tourism employment is also set to benefit this year, after lagging the recovery in the broader employment market. Since Covid-19, the labour market has strengthened significantly - total employment is 6% higher, the participation rate has risen by the 0.7 percentage points and the unemployment rate has fallen by 1.5 percentage points. But, tourism jobs have not recovered. Tourism currently accounts for 4% of jobs, while pre Covid it was just over 5%. Rising tourism-related jobs as arrivals pick up will help to offset weakness in the jobs market across other sectors, as we expect to see the unemployment rate increasing this year as the economy slows from the impact of the tightening in monetary policy.

Education arrivals

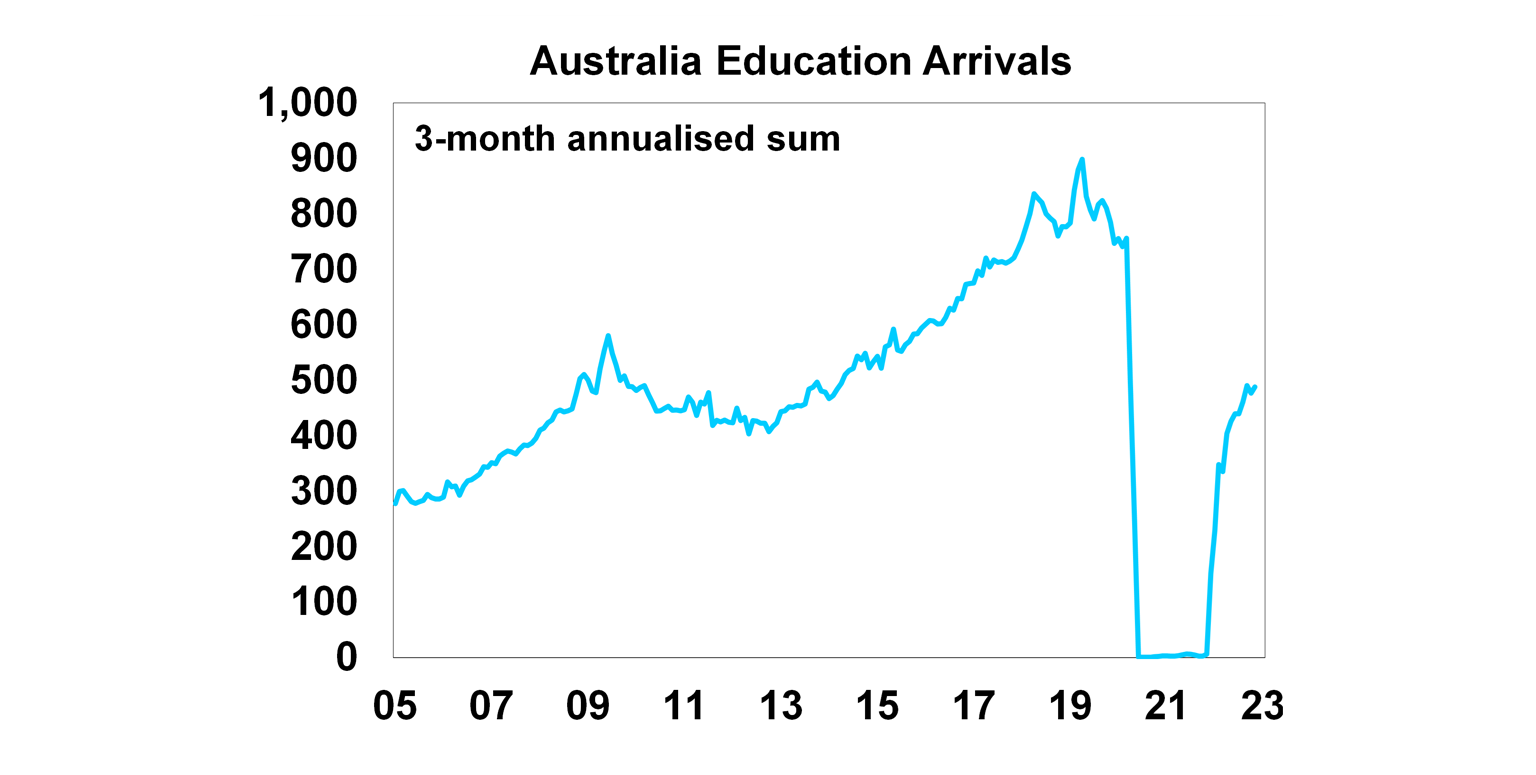

Besides tourism, education arrivals are another major sector of inbound arrivals into Australia, which were worth around $40bn or 2% of GDP at its peak before the pandemic. Education arrivals have been picking up swiftly (see the chart below) but are still around 30% below pre-Covid levels. The re-opening of China will help to lift education arrivals as Chinese students previously made up around a third of all student arrivals.

Conclusion

Australian inbound short-term arrivals are still well below pre-Covid levels but have significant room to rise in 2023. China’s reopening will provide a decent boost to inbound arrivals as Chinese tourists and students used to make up significant shares of arrivals, but it will take some time for travel to resume to normal levels due to initially limited airline capacity and health concerns around travelling. The recovering tourism sector in Australia will be a positive growth driver in 2023 and help to offset other weak parts of the economy, including slowing consumer spending and negative growth in residential construction. But, Australian GDP growth is still expected to be low this year, rising by just 1.5% over the year to December which is much lower than usual for Australia (usually GDP growth is between 2.5-3% per annum).

You may also like

-

Weekly market update - 27-03-2026 A negative start to the weak due to signals from Trump that he would strike Iranian power plants and energy infrastructure, no signs of a broad reopening in the Strait of Hormuz and further deployment of 2,000 US soldiers of the elite US Army’s 82nd Airborne Division turned into mid-week confidence on signs of “constructive conversations” between the US and Iran and Trump indicating a pause on further strikes until March 27th. -

Oliver's Insights - Charts for uncertain times Most of the time share markets are relatively calm, but periodically they tumble and generate headlines like “billions wiped off share market.” -

An SMSF lending specialist answers common questions about SMSF property investing AMP Bank lending specialist Aldwin Calubad answers the most common – and most misunderstood – questions Australians ask about SMSF property investing.

Important information

Any advice and information is provided by AWM Services Pty Ltd ABN 15 139 353 496, AFSL No. 366121 (AWM Services) and is general in nature. It hasn’t taken your financial or personal circumstances into account. Taxation issues are complex. You should seek professional advice before deciding to act on any information in this article.

It’s important to consider your particular circumstances and read the relevant Product Disclosure Statement, Target Market Determination or Terms and Conditions, available from AMP at amp.com.au, or by calling 131 267, before deciding what’s right for you. The super coaching session is a super health check and is provided by AWM Services and is general advice only. It does not consider your personal circumstances.

You can read our Financial Services Guide online for information about our services, including the fees and other benefits that AMP companies and their representatives may receive in relation to products and services provided to you. You can also ask us for a hardcopy. All information on this website is subject to change without notice. AWM Services is part of the AMP group.