Investment markets and key developments

Major global share markets fell over the last week, as higher bond yields weighed. For the week US shares fell 0.5%, Eurozone share lost 1%. Japanese shares fell 0.4% and Chinese shares fell 0.6%. This still left US shares up 4.8% in May and global shares up 3.8% after the weakness seen in April. The Australian share market fell 0.3% for the week on the back of the weak global lead, higher than expected inflation data for April, lower metal and energy prices and uncertainty about what the failure of BHP’s bid for Anglo American might mean for it. This left the local share market up 0.5% in May. Bond yields pushed higher again, not helped by weak bond auctions in the US possibly suggesting that investors may be getting concerned about the widening US budget deficit which is now above 6% of GDP and will likely worsen if Trump wins the upcoming election. Oil, metal and iron ore prices fell, but the $A rose helped by a slightly weaker $US.

The ride for shares is likely to remain volatile and constrained as valuations remain stretched, sentiment towards shares remains upbeat which is negative from a contrarian perspective, uncertainty remains regarding the outlook for interest rate cuts in the US and Australia and geopolitical risks around the Israel/Iran conflict and US election are high. We continue to see further gains in shares this year as disinflation continues, central banks ultimately cut interest rates and recession is avoided or proves mild, but the risks of a deeper correction beyond that seen in April have increased.

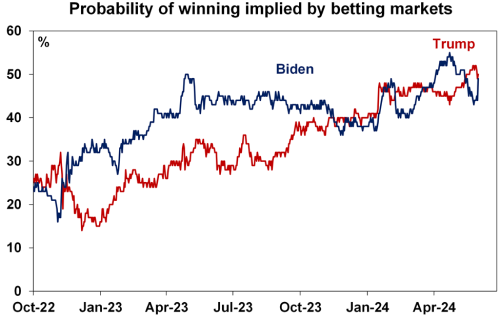

Trump found guilty in the hush money trial, but will it impact his election prospects? The US election in November has significant potential to impact investment markets because of the radical policy differences Trump offers versus Biden. Trump’s tax cut and deregulation policies would be seen as positive for share markets (assuming bond investors don’t baulk at his likely higher budget deficits) but his policies to dramatically hike tariffs setting off a new bigger trade war, curtail immigration and weaken Fed independence point to higher inflation, weaker global growth and a threat to Australian exports. Markets have been ignoring the election so far but given the policy differences they are likely to start focussing on it soon, particularly given his conviction and the 27th June debate. Trump is leading Biden in polls by around 1 point, but around 14% are undecided and 15-25% of his supporters have indicated they will reconsider if he is convicted of a crime. Against this, the guilty verdict may just serve to galvanise support amongst his base. Straight after the guilty verdict the PredictIt betting market saw the probability of a Biden victory rebound to just below that of Trump. But there is a long way to go yet.

Source: PredictIt, AMP

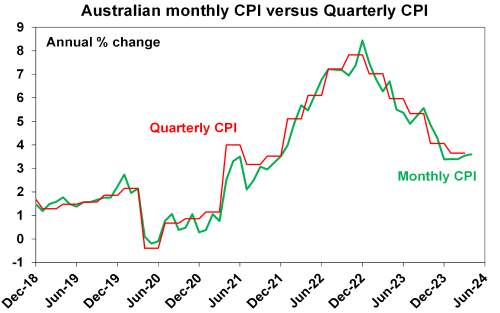

Australian inflation surprisingly rose in April. The uptick in the Monthly Inflation Indicator to 3.6%yoy from 3.5%yoy was disappointing and contrary to our own expectations for a fall. The main drivers were weather related food prices, tobacco, health insurance premiums, fuel prices and continued rapid increases in rents and general insurance.

Source: ABS, AMP

Worryingly for the RBA, underlying measures of inflation edged higher with the trimmed mean inflation rate rising to 4.1% with ongoing sticky services inflation.

Source: ABS, AMP

The further uptick in inflation keeps the risk of another RBA rate hike high and reinforces that rates will be high for longer. This was reflected in money market expectations that swung back towards pricing in the risk of another rate hike and pushed back expectations for a rate cut till late next year. But as can be seen in the next chart, money market expectations for the cash rate can bounce around a lot.

Source: ABS, AMP

But inflation is likely to resume its downtrend and the economy is looking weaker, so we still see the next RBA move as being a cut. The RBA is likely to again consider the case for another rate hike at its 18 June meeting just like it did at its May meeting. However, while the risk of another hike is high (particularly in August if June quarter inflation is higher than the RBA expects) the most likely scenario is that rates will remain on hold: the rise in monthly inflation to 3.6%yoy in April may not have been a surprise to the RBA as its forecasting 3.8%yoy inflation this quarter; the monthly CPI Indicator is very volatile; much of the monthly rise in May looks to have been seasonal with the CPI up 0.7%mom but the seasonally adjusted CPI up 0.2%mom; May tends to be a weaker month with the CPI falling in 4 of the last 6 Mays; cost of living measures will help pull down headline inflation in the second half of the year; and weak spending in the economy (evident in retail sales and construction over the last week) will continue to bear down on inflation by making it harder for companies to raise prices. In short, the April rise in inflation is not enough to push up the RBA’s inflation forecasts for inflation to be back in the target band in 2025 and 2026, which would be necessary for it to hike again. To borrow from the minutes to its last meeting it remains appropriate for the RBA to continue to “look though short-term variation in inflation” and “to avoid excessive fine-tuning.” At this point we are continuing to see the first cut coming at year end but note that there is a high risk that it will be delayed into 2025.

Major global economic events and implications

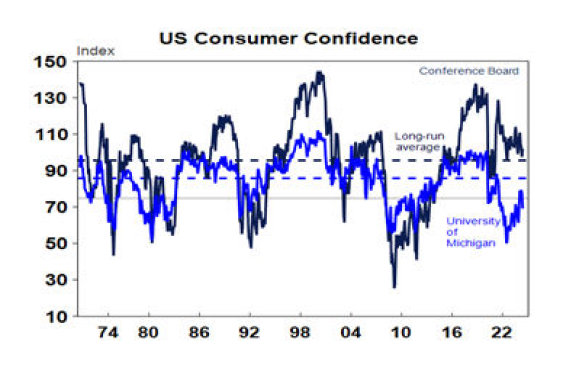

More mixed US economic data. The Conference Board’s measure of consumer confidence improved in May and the net proportion of respondents reporting that jobs are plentiful improved slightly. But the trend remains down in the latter, home price growth slowed in March, March quarter GDP growth was revised down to 1.3% annualised from 1.6%, with downwards revisions to wages growth and core inflation and personal income and spending were weak in April with real spending down 0.1%mom.

Source: Macrobond, AMP

Meanwhile, US core private final consumption (PCE) inflation improved in April after three hot months, falling to 0.2%mom (or 0.249% to be precise) taking annual core PCE inflation to 2.75%yoy, the lowest since March 2021. Core services ex housing inflation also trended lower. This is good news for the Fed, but it will probably need to see three months of core PCE inflation around 0.2%mom before starting to cut. We continue to see the first Fed cut being in September.

Eurozone unemployment fell to 6.4% in April and economic sentiment improved slightly (but remained weak) in May, but bank lending was unchanged. Over the last year bank lending has fallen 0.3%yoy. Eurozone inflation rose slightly to 2.6%yoy in May from 2.4%yoy in April, with core inflation rising to 2.9%yoy from 2.7%yoy. This is unlikely to prevent the ECB from cutting rates in the week ahead as inflation is still trending down, but its guidance for future cuts will be cautious and dependent on inflation falling as forecast.

Japanese economic data was mixed. Consumer confidence fell in May to its lowest level since October and industrial production unexpectedly fell but retail sales rose solidly and unemployment was unchanged.

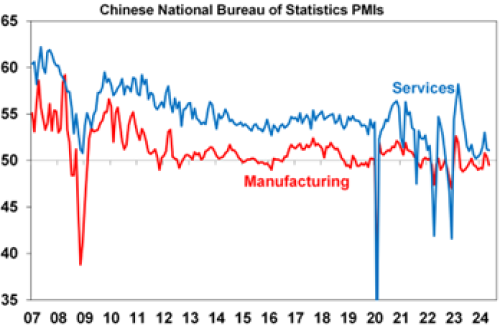

Chinese business conditions PMIs softened in May and suggest downside risks to our GDP forecast for 4.5-5% growth this year. That said, they bounce around a lot.

Source: Bloomberg, AMP

Australian economic events and implications

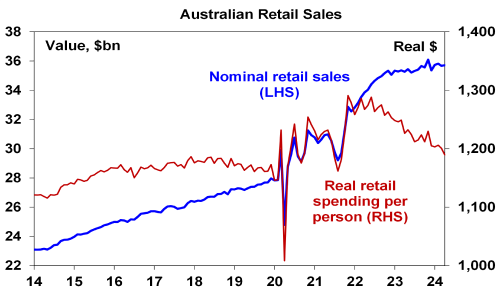

Australian economic data releases over the last week were mostly soft. Consistent with poor levels of consumer confidence, retail sales rose a less than expected 0.1% in April after a 0.4% fall in March. The level of retail sales may look high verses their pre-Covid trend but adjusted for inflation and massive population growth they have fallen into a hole – almost back to the Delta lockdown lows! High rates along with cost-of-living pressures are continuing to work to cool demand, which will lead to lower inflation with a lag.

Source: ABS, AMP

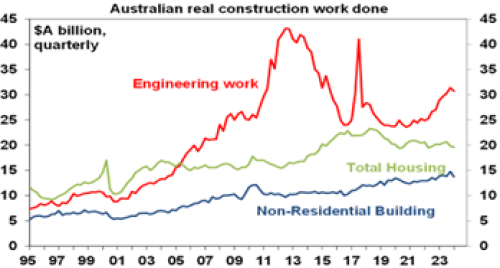

March quarter construction unexpectedly fell sharply. Falls were broad based across home building, non-residential construction and engineering.

Source: ABS, AMP

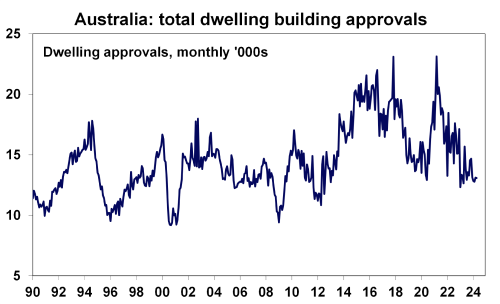

Continued weak housing approvals point to weak ongoing residential homebuilding. There is still a big pipeline of homes approved but not completed but approvals are running around 160,000 homes per annum, which is way below the roughly 250,000 we need to match underlying demand at present on the back of the population surge and the objective of Australian governments to build 240,000 homes pa over the next five years.

Source: ABS, AMP

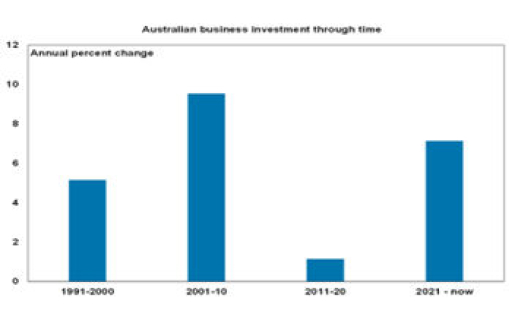

Partly offsetting the weakness in consumer spending and construction last quarter, business investment rose 1%qoq in the March quarter driven by non mining equipment, particuarly in information media and telecommunications with continued strength in intellectural property reflecting the growth in data and technology. Much of this equipment will be imported so there is an offset in terms of the support for GDP growth but the boost to non-mining investment is welcome in terms of boosting productivity growth. So far this decade, business investment is looking far stronger than was the case last decade.

Source: ABS, AMP

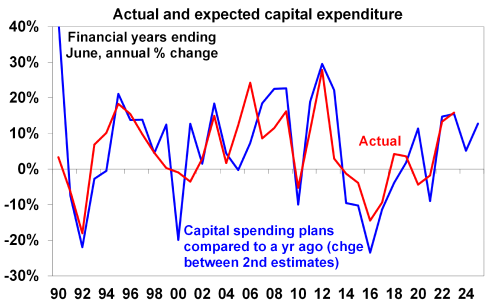

What’s more, business investment plans for this financial year and next compared to those made a year ago imply nominal capex growth of around 12% each year suggesting that investment growth remains reasonably resilient.

Source: Bloomberg, AMP

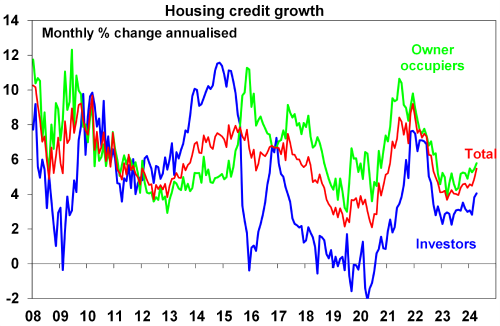

Private credit growth picked up slightly in April but remains moderate at 5.2%yoy. Housing credit growth continues to edge higher reflecting the lagged impact of stronger housing finance commitments.

Source: RBA, AMP

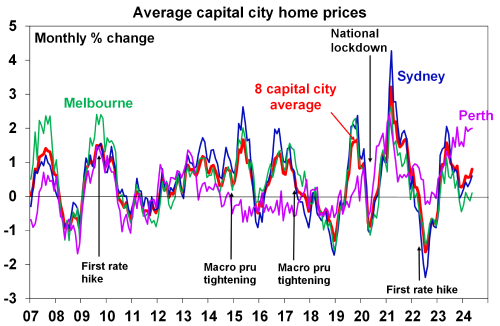

CoreLogic home price data showed a lift in average price growth for the five big capital cities to 0.8% in May as the housing shortage continues to dominate the drag from high mortgage rates. There remains a huge divergence between cities with Perth, Brisbane and Adelaide booming but Melbourne subdued. The housing shortage continues to point up for home prices, but the delay in rate cuts and talk of rate hikes risks renewed falls in property prices as its likely to cause buyers to hold back and distressed listings to rise. The latter already appears to be occurring in some cities, notably Melbourne.

Source: CoreLogic, AMP

What to watch over the next week?

In the US, the focus will be on jobs data (Friday) with May payrolls expected to have risen 180,000, unemployment expected to remain unchanged at 3.9% and hourly wages growth likely to remain around 3.9%yoy. Job openings and quits data (Tuesday) for April are expected to have shown a further slowing. Meanwhile the ISM manufacturing and services conditions indexes (due Monday and Wednesday respectively) are expected to have shown slight improvements in May.

Both the Bank of Canada (Wednesday) and European Central Bank (Thursday) are expected to kick of rate cutting cycles with both cutting their key policy rates by 0.25% following the decline in inflation. They are both likely to foreshadow further cautious easing ahead if inflation continues to fall as expected. This will take Canada’s policy rate down to 4.75% and the ECB’s deposit rate to 3.75% and its main refinancing rate to 4.25%.

Chinese trade data for May (Friday) is likely to show a renewed slowing in imports but a further improvement in exports.

In Australia, March quarter GDP data on Wednesday is likely to show a further slowing in GDP growth to 0.2%qoq or 1.2%yoy, from 1.5%yoy in the December quarter on the back of a large (-0.6 percentage points) detraction from trade, flat consumer spending and falling dwelling investment offset by modest growth in capex and public spending. The risk of a fall is high but either way we will likely see a continuation of the per capita recession for a fourth quarter. In other data, expect CoreLogic data for May (Monday) to show a slight acceleration in national home price growth to 0.8%mom, and April housing finance to have increased 1%mom with the trade surplus remaining around $5bn (both Thursday). New RBA Deputy Governor will participate in a “Fireside Chat” on Friday.

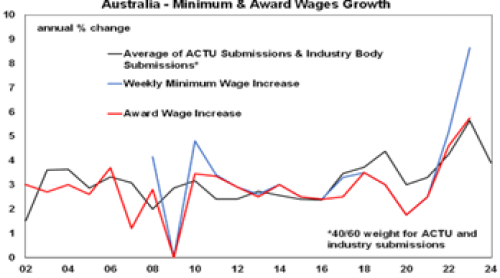

The Fair Work Commission is due to deliver its decision on the annual increase in award wages on Monday. A smaller rise is expected compared to last year. This directly impacts around 21% of workers. Last year’s decision to increase the minimum wage by 8.65% and awards by 5.75% contributed around 0.7 percentage points to wages growth helping to push it above 4%yoy and is likely a contributor to sticky services inflation at present. A rough guide to the likely increase is to take an average of the ACTU (for a 5% rise) and industry (for a rise just below 3%) submissions which is just below 4%. This would be reasonable – a rise around 4% would give workers a real wage rise, it’s not so high as to add to the risk of a wage price spiral, it’s in line with current wages growth and in line with the rough assessment that 4% wages growth is consistent with 2 to 3% inflation. How the FWC responds to the ACTU’s claim for an extra 4% for female dominated sectors will be important though.

Source: FWC,Macquarie Macro Strategy, AMP

Outlook for investment markets

Easing inflation pressures, central banks moving to cut rates and prospects for stronger growth in 2025 should make for reasonable investment returns this year. However, with a high risk of recession, delays to rate cuts and significant geopolitical risks, the remainder of the year is likely to be rougher and more constrained than the first three months were.

We expect the ASX 200 to return 9% this year and rise to around 7900. A recession is probably the main threat.

Bonds are likely to provide returns around running yield or a bit more, as inflation slows, and central banks cut rates.

Unlisted commercial property returns are likely to be negative again due to the lagged impact of high bond yields & working from home.

Australian home prices are likely to see more constrained gains this year as the supply shortfall remains, but still high interest rates constrain demand and unemployment rises. The delay in rate cuts and talk of rate hikes risks renewed falls in property prices as its likely to cause buyers to hold back and distressed listings to rise.

Cash and bank deposits are expected to provide returns of over 4%, reflecting the back up in interest rates.

A rising trend in the $A is likely taking it to $US0.70 over the next 12 months, due to a fall in the overvalued $US, but in the near term the risks for the $A are on the downside as the Fed delays rate cuts and given the still high risk of an escalating conflict in the Middle East.

Weekly market update 28-06-2024

28 June 2024 | Blog Dr Shane Oliver observes strong financial year returns - but can it continue?; Trump odds up after debate - watch trade war risks; risk of another RBA hike up but not fait accompli; Australian jobs market cooling; another big Australian budget surplus and more. Read more

Oliver's insights - investing 40 years

25 June 2024 | Blog Dr Shane Oliver shaes his nine most important lessons from investing over the past 40 years. Read more

Weekly market update 21-06-2024

21 June 2024 | Blog This week, narrowing US share gains; drip feed of falling global inflation & rates is good sign for RBA; Federal & state governments making the RBA's job harder; the pros & cons of nuclear; and more. Read moreWhat you need to know

While every care has been taken in the preparation of this article, neither National Mutual Funds Management Ltd (ABN 32 006 787 720, AFSL 234652) (NMFM), AMP Limited ABN 49 079 354 519 nor any other member of the AMP Group (AMP) makes any representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided and must not be provided to any other person or entity without the express written consent AMP. This article is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives and does not constitute a recommendation, offer, solicitation or invitation to invest.

The information on this page was current on the date the page was published. For up-to-date information, we refer you to the relevant product disclosure statement, target market determination and product updates available at amp.com.au.