Investment markets and key developments

Global share markets mostly fell over the last week on the back of softer than hoped for big tech earnings, concerns about growth and political uncertainty in the US. US shares got a boost on Friday from better inflation data but fell 0.8% for the week with weakness remaining concentrated in IT shares as a rotation away from tech continues to support small caps with the Russell 2000 up 3.5% for the week and 10.4% this month. Eurozone shares rose 0.3% for the week, but Japanese shares fell 6% not helped by talk of further BoJ monetary tightening in the week ahead which has in turn pushed up the Yen. And Chinese shares fell 3.7% dragged down by the lack of decisive stimulus coming out of the Third Plenum despite several stimulus moves over the last week. Australian shares were dragged lower by the global falls with a fall of 0.6% for the week. The ASX 200 is still above its March record high though. Bond yields fell in the US and Europe but rose slightly in Japan and Australia. Oil, metal and iron ore prices fell as did the $A and the $US was little changed.

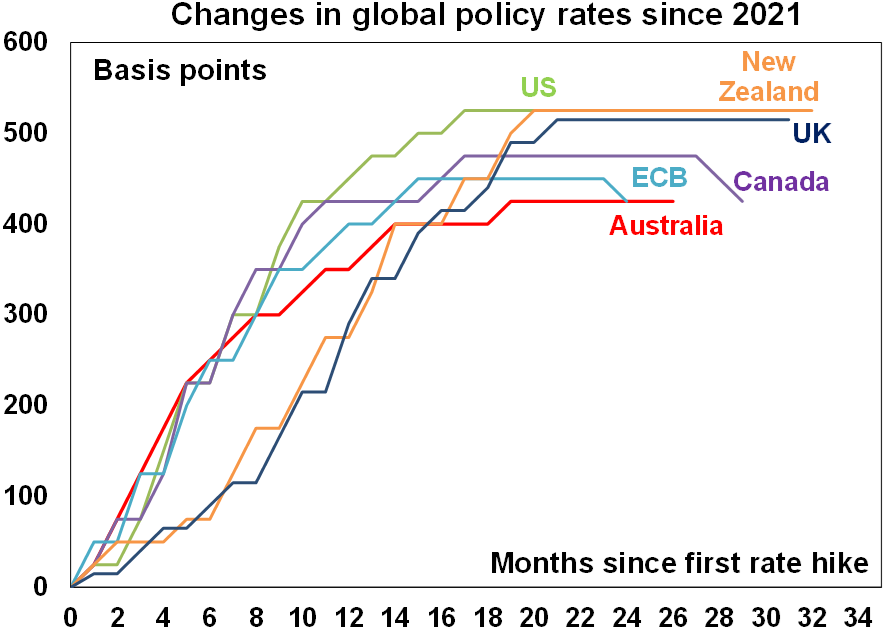

The good news is that global interest rates are continuing to roll over as the focus for central bankers shifts from getting inflation down to avoiding recession. This was highlighted in the past week by the Bank of Canada cutting its key policy rate by 0.25% for a second consecutive time taking it to 4.5%, with more cuts likely ahead as BoC Governor Macklem was dovish citing labour market slack and concerns about household spending. The BoC is now likely to cut twice more this year.

In the US the risk of recession is growing with former New York Fed President Bill Dudley arguing that the rise in unemployment in the US is approaching levels that in the past have signalled recession and inflation pressures have abated so the Fed should preferably cut in the week ahead. While Dudley is just one view, he is pretty balanced and if he is thinking that way several others at the Fed are likely to be too. So, while a Fed cut looks unlikely until September as it waits for more confidence on inflation and stronger than expected June quarter GDP growth suggests no urgency, a surprise cut can’t be ruled out at its meeting in the week ahead with the money market attaching a 21% probability. By September though a rate cut is fully priced in by the money market with nearly three cuts now priced in by year end. August, September and October are also likely to see cuts from the UK, NZ and the ECB so a global easing cycle in developed countries will be well underway. Emerging markets have already clearly moved in that direction with China easing again in the last week – albeit only marginally. Lower interest rates will be positive for shares on a 6 to 12 month view, providing recession is avoided.

Source: Bloomberg, AMP

The bad news is that shares may be entering another correction on the back of a growth scare. For some time we have been concerned that shares are at high risk of another correction as valuations are stretched, investment sentiment looks somewhat optimistic, recession risk is high, there has been a heavy reliance on tech and specifically AI shares to keep the key US share market going and geopolitical risk particularly around the US election but also around the Middle East (with now a Houthi/Israel front), China and Ukraine is high. Concerns about a reversal in the Japanese carry trade may also be impacting, although this should be minor as even with another BoJ hike in the week ahead and other central banks cutting, Japanese rates will still be well below rates in other countries. July is normally a seasonally strong month and US, Japanese, global and Australian shares made record highs this month, but August and September are historically more difficult. So, as we enter the seasonally weak period of August and September a correction may now be starting to unfold and so may have further to run.

Source: Bloomberg, AMP

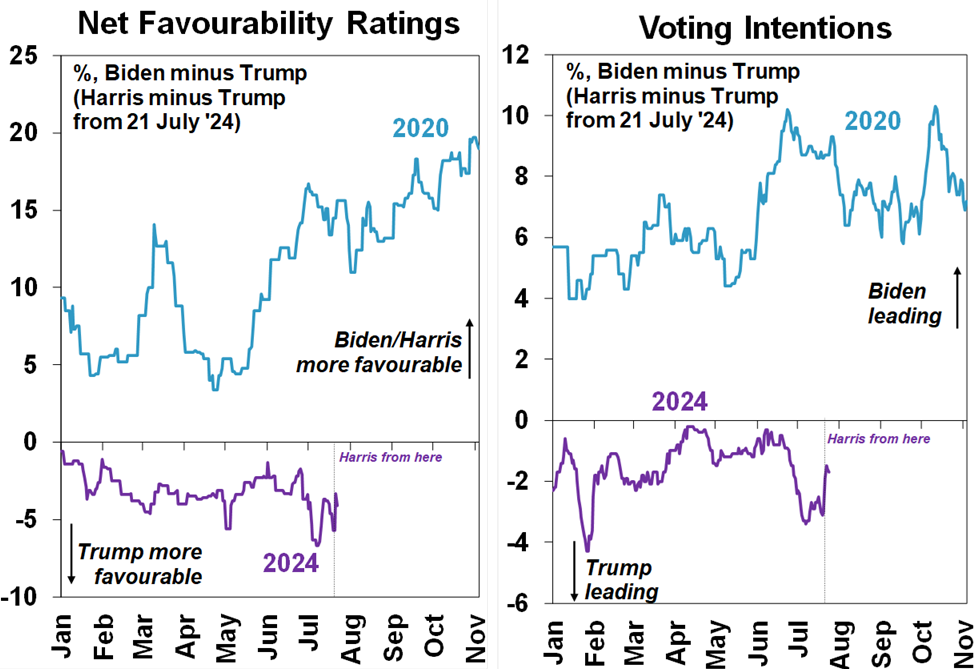

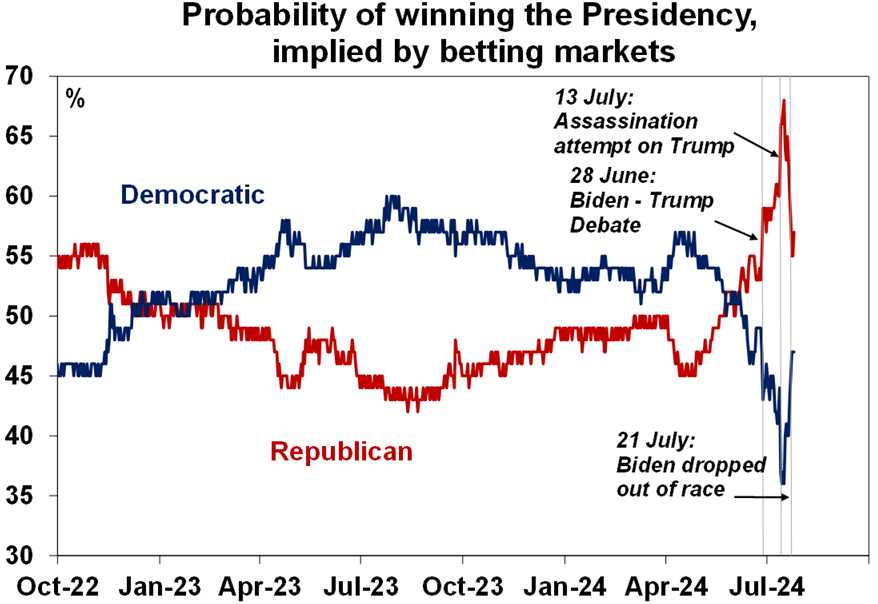

How does the US election fit into this? Election or not, shares are at risk of a correction. We saw one commence a year ago and there was no election then! But investors don’t like uncertainty and this US election is promising plenty of that given the big policy differences between the two sides. Vice President Kamala Harris does not appear to offer any major policy differences to those of President Biden. But Trump offers far more uncertainty. His policies to deregulate (eg “drill baby drill”) and extend tax cuts are positive on their own for shares but he also promises a new and bigger trade war, less immigration which may add to wages growth and hence inflation pressure, a potentially less independent Fed and a bigger budget deficit. This could drive positive Trump trades in fossil fuels versus renewables, small caps versus multinationals, the $US and US versus non-US shares but at an aggregate level its probably more negative for shares than positive via higher than otherwise bond yields and we know from the 2018 US trade wars that it was not positive for shares. This starting to impact share markets particularly as after the debate, assassination attempt and Republican National Conference Trump was looking increasingly likely to win. The replacement of Biden with Harris who is almost certain to win the Democrat’s nomination has made the election a bit more competitive, with, in particular, less chance of a Republican clean sweep (with Republican’s winning the presidency and control of the House and Senate) which history shows is the worst combination for share market returns. Without a clean sweep it will be much harder for Trump to fully implement his agenda. As can be seen in terms of favourability ratings, voting intentions and betting markets’ probability of winning, the Democrats prospects have improved since Harris replaced Biden, but Trump is still ahead. That said there is still a long way to go.

Source: Real Clear Politics, AMP

Source: PredictIt, AMP

What does the ongoing fall in global inflation and the start of a global rate cutting cycle mean for Australia and the RBA? As is well known Australian inflation has been lagging the fall in global inflation and this along with a still tight jobs market (eg 4.1% unemployment compared to 6.4% in Canada) means that another RBA rate hike is a high risk. Much is now riding on June quarter inflation data to be released in the week ahead. However, easing global inflation pressures and central banks starting to cut is a good sign for the RBA as we followed global inflation and rates on the way up and will likely do the same on the way down. In particular, with monetary policy already restrictive and the lagged impact of rate hikes yet to fully flow through the RBA needs to be very careful as global central bankers and possibly now share markets are starting to sniff out rising recession risks. If the US and other major countries slide into recession Australia will not be immune particularly with China’s growth rate flagging recently which is now being reflected in renewed weakness in commodity prices at a time when our economy is already close to stalling leaving us at high risk of recession. Sure, tax cuts will provide a boost but it will likely be offset by a hit to growth from falling immigration levels. At the same time, there is no reason why Australian inflation won’t resume falling as it did after a pause earlier this year in the US, forward looking jobs indicators are warning of higher unemployment ahead, Australian wages growth looks to have peaked - and by the way at 4.1%yoy is way below Canada’s 6.4%yoy pace and they are now cutting rates! - which will slow services inflation and headline inflation is likely to fall sharply in the September quarter which will make another rate hike hard to explain. As such, while we see June quarter inflation on Wednesday coming in at 3.9%yoy for the headline rate and 4%yoy for the trimmed mean, which is higher than the RBA was expecting back in May, the hurdle for another hike should be very high. Our view is that the RBA probably won’t hike again unless underlying inflation as measured by the trimmed mean comes in at 1.1%qoq or 4.1%yoy or higher. See the “what to watch over the next week” section for more details.

Another take on a classic Beach Boys song, God Only Knows. I love the comment from someone on YouTube about it: “For the non-musicians amongst us; This song was written in 2 different keys, A Major and D major (Bass line) played at the same time. That is simply mind blowing considering that music is math. There are 12 steps (notes etc) to a key. To write at 24 notes "in your head" is simply unfathomable, yet Brian Wilson was able to "hear" this in his head and then transpose this into a song. Simply incredible! Say what you want, but this song transcribes our normal abilities as humans to put into a normal song's structure, yet he was able to. Enjoy greatness when you hear it people. THIS song is greatness.” @Eddieedmo4266.

Major global economic events and implications

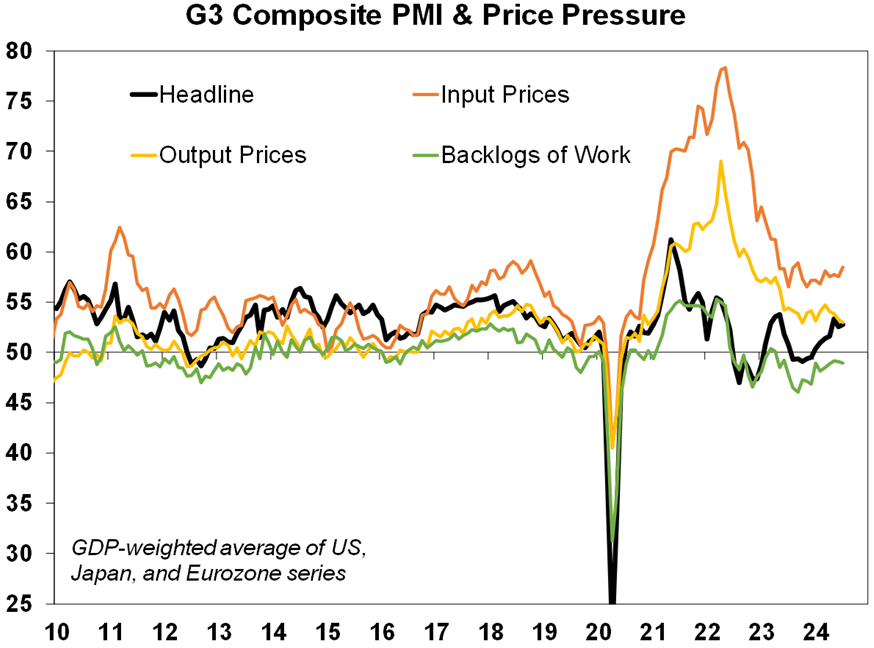

July business conditions PMIs were mixed with falls in Europe and Australia, but increases in Japan, the UK and the US. The G3 average was little changed. Conditions in manufacturing were generally weak and services were generally up. But note that manufacturing is usually more cyclical and tends to lead services, so its ongoing weakness is a warning. Employment also weakened. G3 input prices rose slightly possibly due to higher shipping costs flowing from Red Sea problems but output prices fell with work backlogs remaining weak. This is mostly positive for inflation.

Source: Bloomberg, AMP

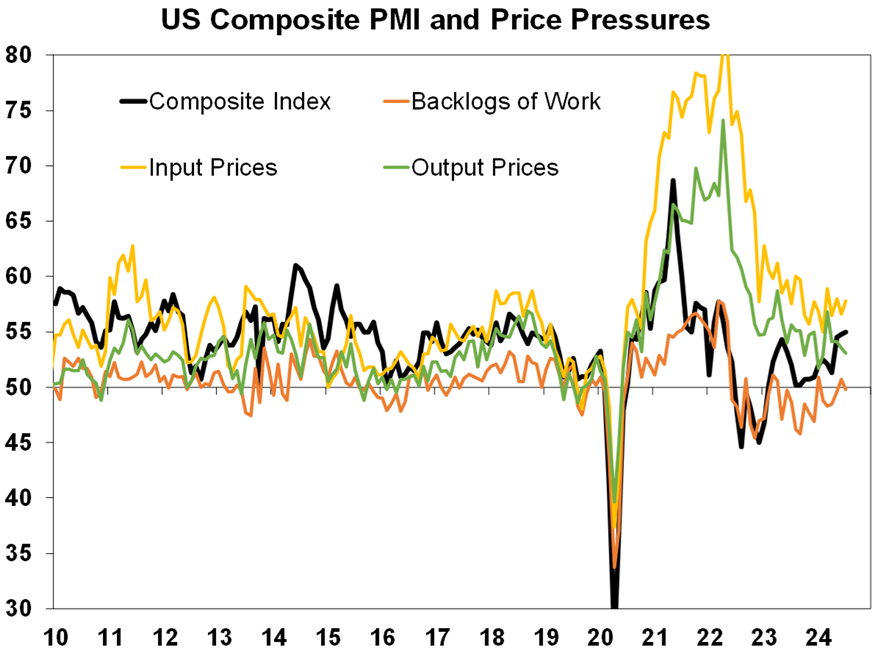

US business conditions PMIs rose in July, but again with manufacturing down and services up. Input prices rose and output prices fell.

Source: Bloomberg, AMP

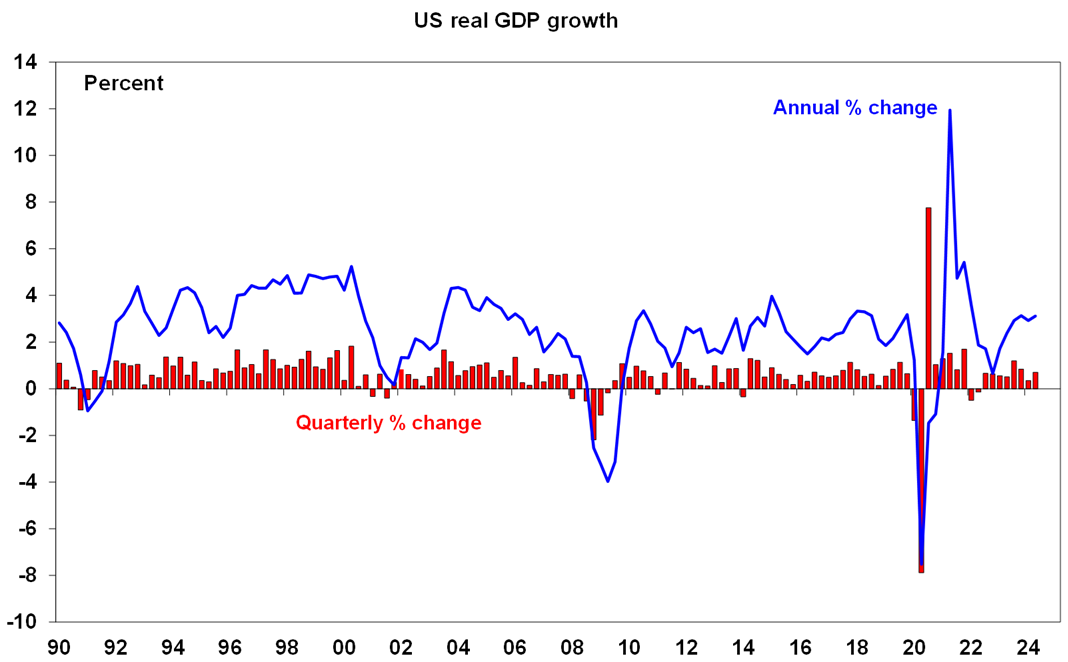

Other US economic data was mixed. US June quarter GDP growth came in stronger than expected at 2.8% annualised with strong growth in consumption and capex. It’s a backward-looking indicator so doesn’t alter the case for the Fed to start cutting but may be interpreted as reducing the urgency to do so. More timely data for June showed underlying capital goods orders & shipments trending sideways, home sales down again and soft personal income and spending growth. Jobless claims fell after a sharp rise the prior week. June core private final consumption inflation data was benign at 0.2%mom/2.6%yoy confirming the resumption of disinflation and consistent with rate cuts starting in September.

Source: Bloomberg, AMP

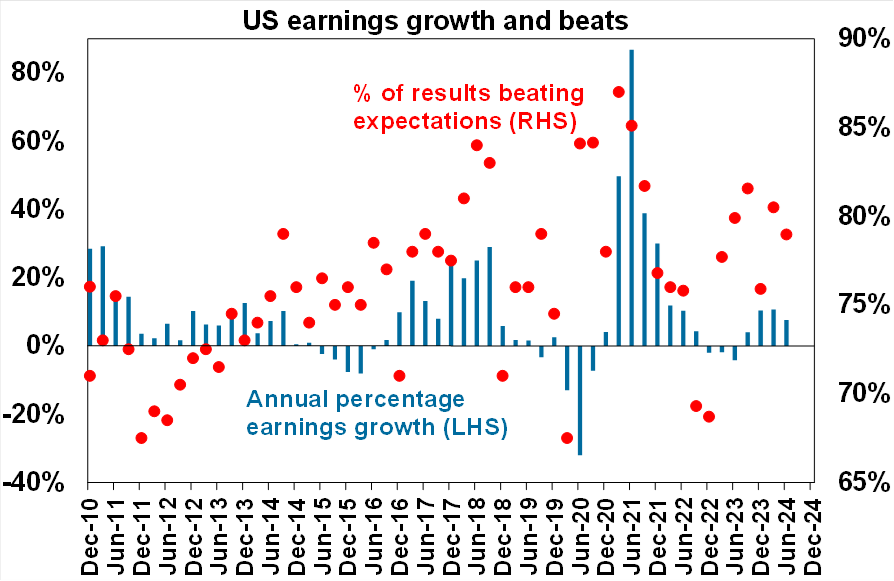

41% of US S&P 500 companies have now reported June quarter earnings, but the results are looking a bit softer this time around with only 78.6% beating expectations which is above the norm of 76% but below the experience of the last reporting season. Consensus expectations for earnings growth are now at 7.6%yoy, down from 7.8% at the start of the reporting season.

Source: Bloomberg, AMP

Along with the weak European PMI readings for July the German IFO business climate index and the French business confidence index fell and bank lending growth remains around zero. Consumer sentiment is up sharply but remains weak.

Source: Macrobond, AMP

More policy easing in China. There has been some step up in policy stimulus measures over the last week consistent with the commitment to “unswervingly achieve the full year growth target.” China’s PBOC cut its 7-day policy rate by 0.1% and this was then followed by a 0.2% cut to its Medium term Lending Facility rate taking it to 2.5%. These moves are small and may be pushing on a string, but a move to provide 300bn RMB (or $A63bn) in subsidies for capital equipment, EVs and consumer appliances may have a more significant impact. These moves still remain modest though suggesting further policy stimulus will remain incremental, including following the upcoming Politburo meeting. They will probably be enough to achieve GDP growth around 4.5% to 5% though.

Australian economic events and implications

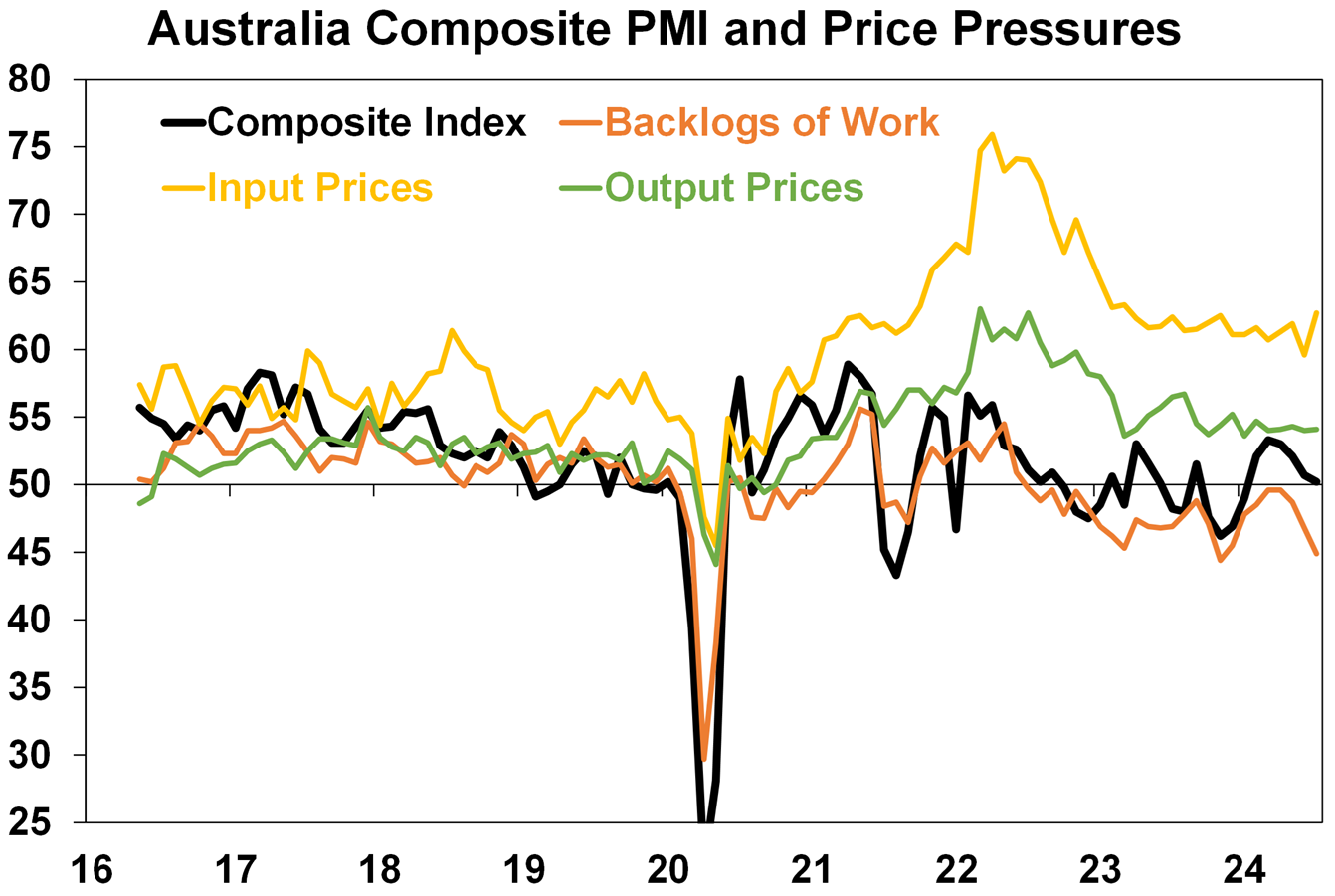

Australian business conditions PMIs for July showed a further deterioration, driven by both services and manufacturing. New orders fell again. Input prices rose likely reflecting award wage rises and higher energy prices from July 1. They have tended to spike in July I in most years outside Covid. But output prices went sideways and work backlogs are weak.

Source: Bloomberg, AMP

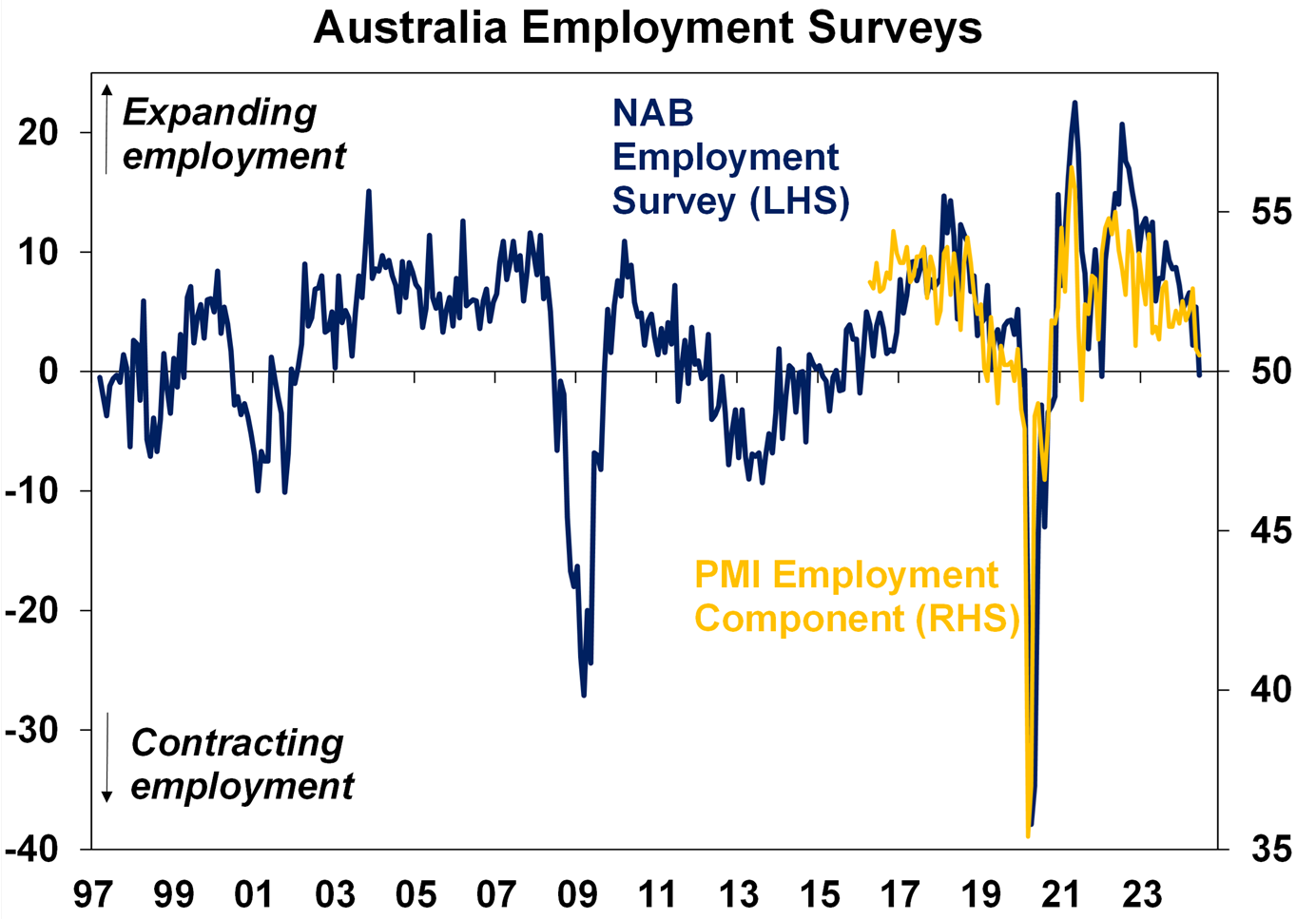

The Australian PMI survey also showed softness in employment, consistent with the NAB survey in pointing to lower jobs growth ahead.

Source: Bloomberg, AMP

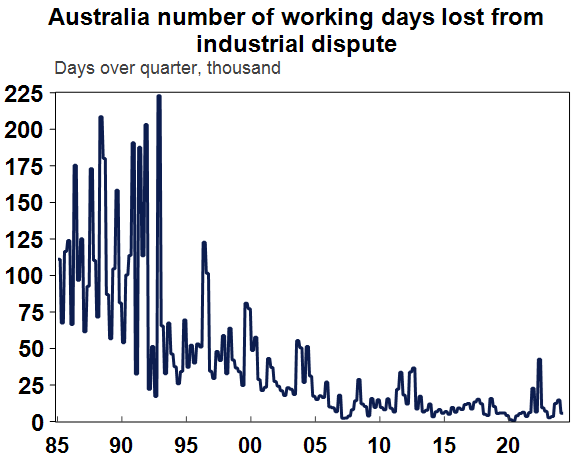

With all the talk about union problems in the building and construction industry it’s worth noting that the number of industrial disputes in Australia and days lost to industrial disputes remain well down on where they were 40 years ago.

Source: Macrobond, AMP

What to watch over the next week?

In the US, the Fed (Wednesday) is expected to leave interest rates on hold at 5.25-5.5% but indicate that its confidence is building that inflation is heading sustainably back to target and that if this continues as expected it will soon be able to start cutting interest rates, setting the stage for a September cut. This is likely to reinforce market expectations for a first cut in September and two or three cuts this year. On the data front expect softer job openings, consumer confidence and home price growth (Tuesday), slowing growth in June quarter employment costs to 1%qoq from 1.2%qoq (Wednesday), another soft manufacturing ISM index (Thursday), a 175,000 gain in July payrolls but with unemployment remaining at 4.1% with wages growth slowing to 3.7%yoy (Friday). The June quarter earnings reporting season will continue with consensus expectations for a 7.6%yoy rise in earnings, which is likely to end up being around 10%yoy again. Apple, Amazon, Meta and Microsoft will all report in the week ahead.

In Europe, inflation for July (Wednesday) is expected to fall to 2.4%yoy with core inflation falling to 2.8%yoy with unemployment (Thursday) unchanged at 6.4%. June quarter GDP growth (Tuesday) is expected to come in at 0.2%qoq/0.5%yoy.

The Bank of England (Thursday) is expected to cut its key policy rate by 0.25% to 5%, on the back of lower inflation and weak growth despite still sticky services inflation and solid wages growth.

The Bank of Japan (Wednesday) is expected to announce detailed plans to slow its bond buying and probably raise rates by another 0.1% or 0.15% with inflation continuing to remain around target. Data for jobs will be released Tuesday with industrial production and retail sales data due Wednesday.

Chinese business conditions PMIs for July (Wednesday and Thursday) are expected to remain soft.

In Australia, long awaited June quarter inflation data (Wednesday) is likely to show a 1.1%qoq rise taking annual inflation to 3.9%yoy from 3.6% with trimmed mean inflation of 1%qoq or 4%yoy. The key drivers are likely to be solid increases in prices for food, health, rent, electricity, petrol, clothing and insurance but softness in communication, car prices, recreation and culture and education. Our forecasts are slightly above the RBA’s forecast for a 1%qoq headline CPI rise and a 0.8%qoq rise in the trimmed mean making another rate hike a high risk, but on balance we continue to see the RBA holding rates where they are if inflation comes in at or below our forecasts as: monetary policy is already restrictive, the risk of recession is high and falling inflation is likely to resume as we have seen in the US this year. And for what it’s worth, June monthly inflation is likely to signal a slight slowing to 3.8%yoy from 4%yoy in May. So on balance providing inflation is no worse than expected we expect the RBA to hold, with the first cut in February. That said if trimmed mean inflation comes in above our forecast at 1.1%qoq or more the RBA would likely see it as too high for comfort and so would likely hike again. The money market is now pricing in just a 21% probability of another hike and the first cut in May.

In terms of other data in Australia, expect a 3% fall in building approvals (Tuesday), a 0.1% rise in June retail sales after a strong bounce in May and a 0.2% fall in June quarter sales (Wednesday), a slight pickup in housing credit but modest credit growth overall (also Wednesday), CoreLogic data for July to show a slowing in house price growth to 0.5%mom (Thursday) and housing finance (Friday) to show a 1% fall.

Outlook for investment markets

Easing inflation pressures, central banks moving to cut rates and prospects for stronger growth in 2025-26 should make for reasonable investment returns over 2024-25. However, with a high risk of recession, poor valuations and significant geopolitical risks particularly around the US election, the next 12 months are likely to be more constrained and rougher compared to 2023-24 and there is a high risk of another correction in the next few months.

We have raised our year end forecast for the ASX 200 to 8100. A recession is probably the main threat.

Bonds are likely to provide returns around running yield or a bit more, as inflation slows, and central banks cut rates.

Unlisted commercial property returns are likely to remain negative due to the lagged impact of high bond yields and working from home.

Australian home prices are likely to see more constrained gains over the next 12 months as the supply shortfall remains, but still high interest rates constrain demand and unemployment rises. The delay in rate cuts and talk of rate hikes risks renewed falls in property prices as its likely to cause buyers to hold back and distressed listings to rise.

Cash and bank deposits are expected to provide returns of over 4%, reflecting the back up in interest rates.

A rising trend in the $A is likely taking it to $US0.70 over the next 12 months, due to a fall in the overvalued $US and a narrowing in the interest rate differential between the Fed and the RBA.

Weekly market update 22-11-2024

22 November 2024 | Blog Against a backdrop of geopolitical risk and noise, high valuations for shares and an eroding equity risk premium, there is positive momentum underpinning sharemarkets for now including the “goldilocks” economic backdrop, the global bank central cutting cycle, positive earnings growth and expectations of US fiscal spending. Read more

Oliver's insights - Trump challenges and constraints

19 November 2024 | Blog Why investors should expect a somewhat rougher ride, but it may not be as bad as feared with Donald Trump's US election victory. Read more

Econosights - strong employment against weak GDP growth

18 November 2024 | Blog The persistent strength in the Australian labour market has occurred against a backdrop of poor GDP growth, which is unusual. We go through this issue in this edition of Econosights. Read moreWhat you need to know

While every care has been taken in the preparation of this article, neither National Mutual Funds Management Ltd (ABN 32 006 787 720, AFSL 234652) (NMFM), AMP Limited ABN 49 079 354 519 nor any other member of the AMP Group (AMP) makes any representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided and must not be provided to any other person or entity without the express written consent AMP. This article is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives and does not constitute a recommendation, offer, solicitation or invitation to invest.

The information on this page was current on the date the page was published. For up-to-date information, we refer you to the relevant product disclosure statement, target market determination and product updates available at amp.com.au.