Investment markets and key developments

Global share markets mostly rose over the last week. US shares rose 0.9% on the back of solid economic data and a mixed but okay start to earnings reporting season. Eurozone shares rose 0.2% with the ECB cutting rates again. Japanese shares fell 1.6%, but Chinese shares rose 1% helped by better than feared economic data despite a lack of detail about fiscal stimulus plans. Australian shares benefitted from the solid US lead and made it to record highs, rising 0.8% for the week. Gains on the Australian share market were led by financial, industrial and health care shares offsetting weakness in energy and IT shares. Oil prices fell 8.4% and metal and iron ore prices also fell, but gold prices rose to a record high. The $A fell as the $US rose.

Shares continue to face the risk of another correction, but the broad trend is likely to remain up. The key risks are that valuations are stretched particularly for US tech stocks, the risk of recession remains high in the US and Australia, the expansion of the war in the Middle East threatens to impact oil supplies and a Trump victory in the US election (with polling moving his way) could spark fears around another trade war. On a 6-12 month view though shares are likely to head higher on the back of the success in getting global inflation down, central bank rate cuts (with the RBA getting closer to joining in) and China ramping up policy stimulus. October can often see high levels of share market volatility, but beyond that we are coming into a positive time of the year for shares from a seasonal perspective.

Middle East uncertainty remains high – but at least Israel appears to have indicated to the US that when retaliating against the Iranian missile attacks it will strike Iranian military rather than oil or nuclear facilities, which should avoid a disruption to oil supplies and further escalation. At least for now! Uncertainty still remains as the retaliation is yet to occur, but oil prices are now only just 1.5% above their pre-Iran attack levels posing no upwards pressure on Australian petrol prices.

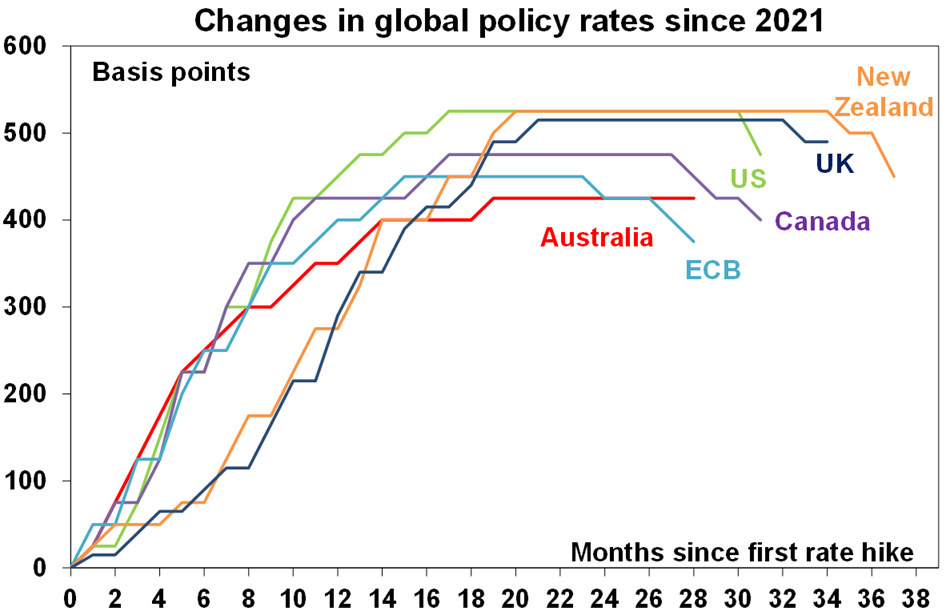

Global disinflation and rate cuts continued over the last week.

- September inflation data in Canada and the UK saw inflation fall below 2% and September quarter data saw New Zealand’s inflation rate fall to 2.2%yoy, which is back within the target range for the first time since March quarter 2021. This leaves the Bank of Canada on track to cut rates again in the week ahead, possibly by 0.5%, the Bank of England on track for another rate cut in November probably of 0.25% and the RBNZ also on track to cut in November by 0.5% but possibly by 0.75% as it doesn’t meet again until Feburary.

Source: Bloomberg, AMP

- The ECB cut its key policy rates by another 0.25% taking its deposit rate to 3.25% and its main refinancing rate to 3.4% noting that “the disinflationary process is well on track”. While President Lagarde provided no forward guidance and noted that the ECB will remain data dependent the overall tone of the ECB’s communications was dovish with Lagarde seeing the risks to inflation as being on the downside. The ECB is likely to cut again at its next meeting in December.

Source: Bloomberg, AMP

- Central banks in the Philippines and Thailand both cut their key policy rates by another 0.25%.

The past few weeks have provided mixed messages as to the outlook for Australian interest rates. On the one hand falling global inflation is a good sign that Australian inflation will continue to fall. This is backed up by falls in forward looking output price indicators – in the NAB and PMI surveys - and the Melbourne Institute’s Inflation Gauge which are pointing to more good news on underlying inflation. And the RBA appears to be getting a bit less hawkish - with no consideration of another hike at its September meeting, the RBA dropping the “no rate cut expected in the near term” line from its formal communication and RBA Chief Economist Hunter noting that its less concerned about a rise in inflation expectations. Against this though, the September jobs data came in on the strong side with unemployment falling back to 4.1% reducing the pressure to ease to help the economy and likely reinforcing RBA concerns that the jobs market is still too tight risking wages growth greater than is consistent with the 2-3% inflation target. That UK and US unemployment is also around 4% and yet they are seeing slowing wages growth and slowing inflation may provide the RBA with a bit of confidence not to be too concerned. But the September jobs data on its own reduces the possibility of a cut by year end (the money market now puts the probability at 26%) and puts greater importance on upcoming inflation releases. We think a December cut is still possible if underlying inflation comes in much weaker than expected, but our base case remains for the first cut to come in February.

Australia’s plunging birth rate – is it time for another “one for mum, one for dad and one for the country baby bonus”? ABS data shows that the fertility rate (births per woman) fell to a record low of 1.5 last year down from a post war high in 1961 of 3.5. The downtrend briefly reversed in the late 2000s helped by the “baby bonus” and the impact of women delaying children into their 30s. But the fertility rate for women in their 30s now looks to have peaked and the baby bonus is long gone. The long-term decline reflects a combination of factors including falling teenage births (with better birth control), better social security (less need for children to look after you in old age), falling infant mortality (so no need to have lots of kids as insurance), better career options for women, more things to spend money on and the perceived rising cost of having children made worse by deteriorating housing affordability. Australia is not alone - the UK is at 1.5, Japan is at 1.3, China 1.2, Italy 1.3, Singapore 1.1 and South Korea at 0.9. And global comparisons show that rising per capita GDP correlates with falling fertility over long periods. The falling birth rate means an aging population and an increasing reliance on a relatively smaller group of workers to cover the costs to the economy of a relatively rising group of retirees. Australia is better off than most countries as it can run high immigration levels to offset the slowdown in natural population growth. But that also has issues, and the population will still age. So, what about another baby bonus? It may have worked with Gen X in the 2000s but its doubtful it will work with younger Millennials and Gen Z now and the experience of other countries trying to boost fertility doesn’t provide much cause for optimism that such policies will work in Australia now.

Source: ABS, Bloomberg, AMP

Copacabana has been in the headlines a bit over the last week! It wasn’t Barry Manilow’s best song…in it’s kind of annoying. Looks Like We Made It and I Write the Songs (which was written by a Beach Boy) are way better. And I would prefer Ipanema.

Major global economic events and implications

US economic data releases over the last week were mostly solid. Industrial production fell in September with strikes and hurricanes impacting, housing starts and permits also fell and the October New York regional manufacturing index also fell but the Philadelphia regional manufacturing index rose, home builder’s conditions improved, jobless claims remained low & retail sales rose more than expected with real consumer spending on track for a rise of around 3.5% annualised in the September quarter. Partly reflecting this the Atlanta Fed’s GDP Now puts September quarter GDP growth at 3.4% annualised. At the same time price components of the regional manufacturing indices remained benign. So, Goldilocks continues!

Source: Macrobond, AMP

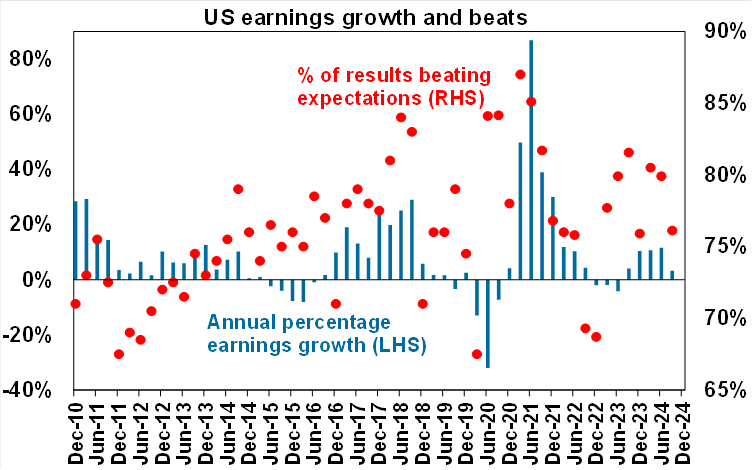

Slower US earnings growth? Only 14% of US S&P companies have reported September quarter earnings, so it’s too early to form a strong assessment. So far 76.4% of results have surprised on the upside which is in line with the norm of 76% and the consensus earnings growth expectation is for just 3.2%yoy. That said earnings surprise is averaging around 6.5% so the final earnings growth number should come in around 7%yoy.

Source: Bloomberg, AMP

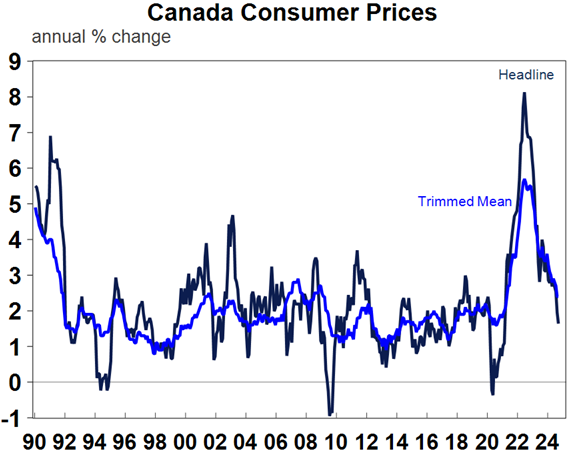

Canadian inflation for September fell below target to 1.6%yoy with its core trimmed mean underlying inflation measure unchanged at 2.4%yoy.

Source: Macrobond, AMP

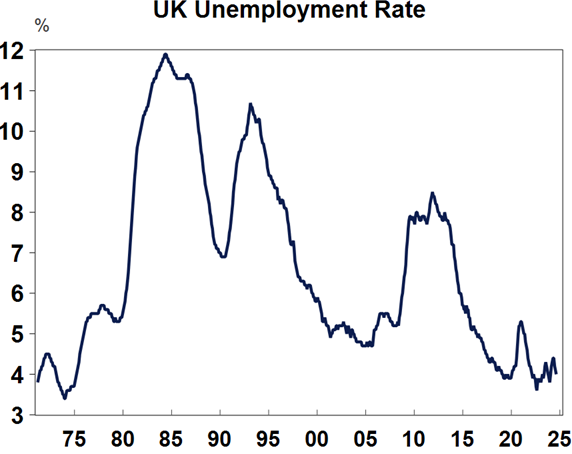

UK inflation for September also fell below target to 1.7%yoy with core inflation falling to 3.2%yoy. Labour market data was mixed though with employment up and unemployment falling to 4% but wages growth slowing to 3.8%yoy.

Source: Macrobond, AMP

Japanese CPI inflation slowed to 2.5%yoy in September from 3%, as the Government reintroduced electricity and gas price controls. Core (ex food and energy) inflation was unchanged though and inflation remains consistent with the Bank of Japan continuing with a modest and gradual approach to tightening monetary policy.

New Zealand inflation for the September quarter fell to 2.2%yoy taking it back within the 1-3% target range for the first time since March quarter 2021. Core inflation fell to 3.1%yoy.

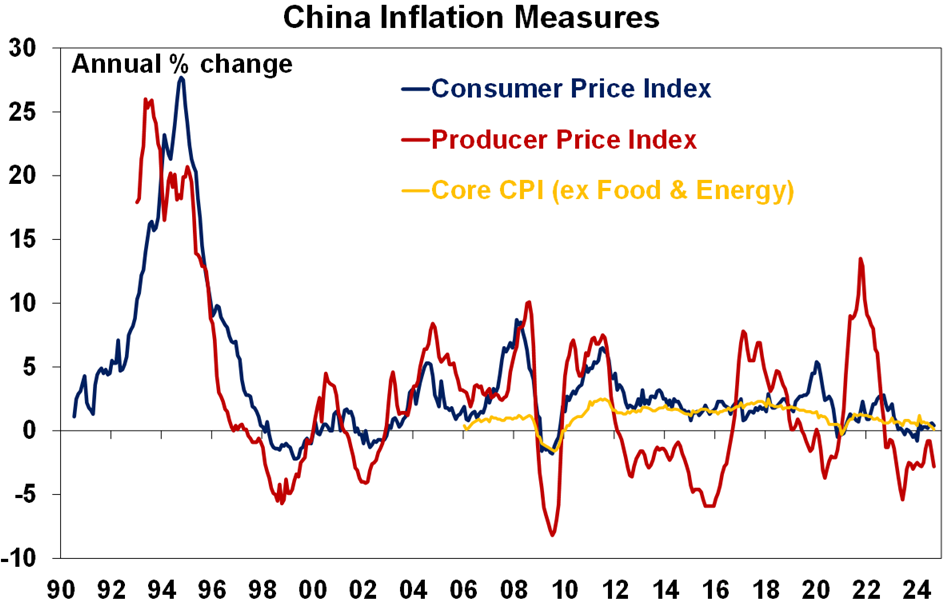

Chinese September quarter data showed a further slowing in growth, but stimulus should help a bit over the year ahead. GDP growth slowed to 4.6%yoy, but September monthly growth for industrial production picked up to 5.4%yoy and that for retail sales improved but to a still weak 3.2%yoy. Monthly investment growth remained weak though at 3.4%yoy, annual credit growth slowed to a record low and exports and imports came in even weaker than expected. And property sales, investment and prices keep falling with the property sector remaining a key drag on growth. Growth this year may come in a bit below the 5% level, with policy stimulus providing some help but it’s getting a bit late to impact this year.

Source: Bloomberg, AMP

Reflecting the weakness in demand inflation fell further in September with core CPI inflation of just 0.1%yoy and producer price deflation accelerating to -2.8%yoy.

Source: Bloomberg, AMP

Still waiting for Chinese stimulus details. A press conference by the Ministry of Finance ticked many of the right boxes with more bond issuance to resolve local government debt, allow local governments to buy unsold property and help banks boost capital. But a Housing Ministry press conference provided only incremental moves. We are left waiting for the National People’s Conference Standing Committee meeting expected later this month to confirm the size of the fiscal stimulus package. And so far, there is not much on help for consumers. Our view remains that policy stimulus will provide a short term cyclical boost to maybe 5.5% growth next year, but won’t really address China’s longer term structural problems.

Australian economic events and implications

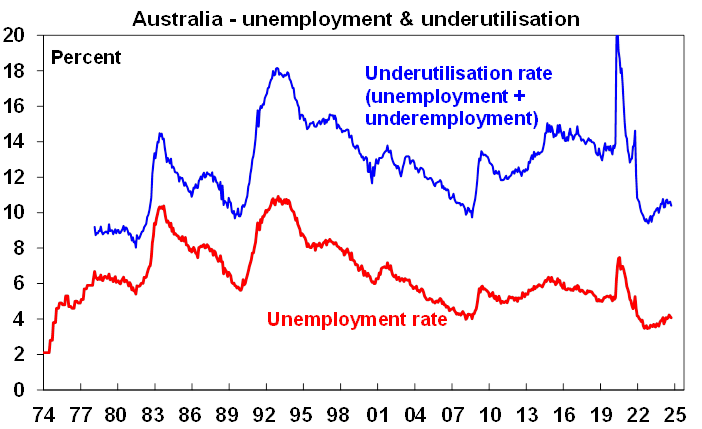

September jobs data remained surprisingly strong. Employment growth was solid again, full time employment was the main contributor to jobs growth and so hours worked rose and unemployment was unchanged at a downwardly revised 4.1% with underemployment down slightly to 6.3%. While labour force participation rose to a record high, jobs growth was faster than growth in the workforce and the share of the population in jobs also rose to a record high.

Source: ABS, AMP

The still rising trend in unemployment and labour market underutilisation tells us that the jobs market is cooling but its only gradual and the relatively low level for both tells us that right now the labour market remains relatively tight.

Source: ABS, AMP

Falling job vacancies and business hiring plans evident in our Jobs Leading Indicator continue to point to slower employment growth ahead. But for now the RBA will regard the jobs market as remaining relatively tight and indicative of a lack of spare capacity in the economy so, as noted earlier in this report, on its own it reduces the possibility of a rate cut by year end with our base case remaining for the RBA starting to cut in February.

Source: ABS, AMP

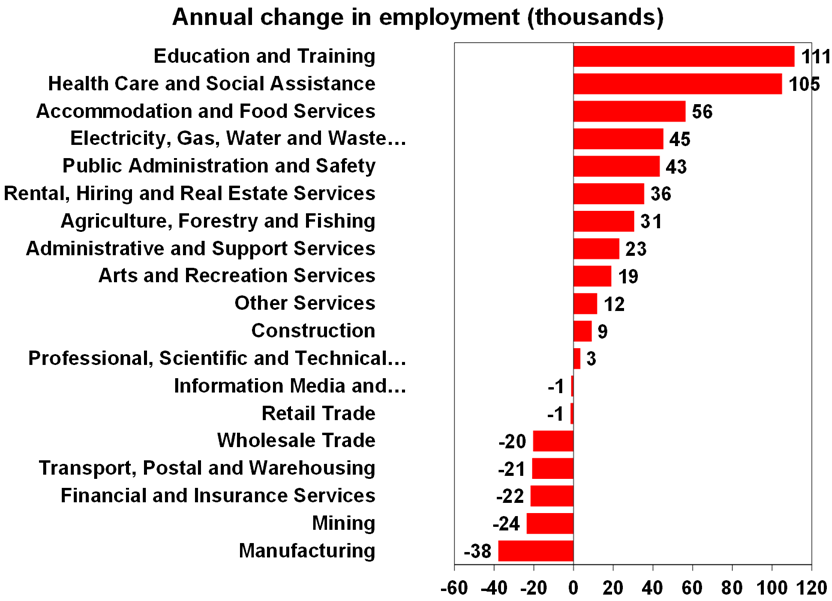

What sectors are driving the jobs growth? Over the last year public sector related industries figure highly in the areas of strongest jobs growth – notably education, health and public administration, whereas market sector related industries figure highly in areas of weak employment – notably manufacturing, mining and finance. In other words, the boom in public spending is a key factor behind the strength in jobs. This is good for employment but is likely keeping interest rates higher for longer and depressing productivity growth.

Source: ABS, AMP

What to watch over the next week?

The week ahead will see business conditions PMIs released for October on Thursday. These are likely to show some softening from a solid level in the US but continuing soft conditions in Europe and Australia with softness remaining concentrated in manufacturing. Key to watch will be whether the broad-based weakness in manufacturing conditions starts to flow through to services.

Apart from the PMIs, US durable goods orders (Friday) are likely to show ongoing flat conditions for capital goods orders and shipments along with a slight rise in existing home sales (Wednesday). The September quarter earnings reporting season will ramp up with consensus expectations for a 3.2%yoy rise, ranging from -27%yoy for energy to +16%yoy for technology. After upside surprises its likely to come in around 7%yoy.

The Bank of Canada (Wednesday) is expected to cut its policy rate by another 0.25% taking it to 4%, with some chance it could be a 0.5% cut. Its guidance its likely to remain dovish.

Comments by RBA Deputy Governor Hauser (Monday) will be watched for clues on the outlook for interest rates, particularly given recent indications (in the minutes to its last meeting and in a speech by Chief Economist Hunter) that it may be tilting in a slightly less hawkish direction.

Outlook for investment markets

Easing inflation pressures, central banks cutting rates, China ramping up policy stimulus and prospects for stronger growth in 2025-26 should make for reasonable investment returns over the next 6-12 months. However, with a high risk of recession, poor valuations and significant geopolitical risks particularly around the Middle East and US election, the next 12 months are likely to be more constrained and rougher compared to 2023-24.

Bonds are likely to provide returns around running yield or a bit more, as inflation slows, and central banks cut rates.

Unlisted commercial property returns are likely to remain negative due to the lagged impact of high bond yields and working from home reducing office space demand.

Australian home prices are likely to see more constrained gains over the next 12 months as the supply shortfall remains, but still high interest rates constrain demand and unemployment rises. Lower interest rates should help the market next year though and we see average property prices rising by around 5% in 2025.

Cash and bank deposits are expected to provide returns of over 4%, reflecting the back up in interest rates.

A rising trend in the $A is likely taking it to $US0.70 over the next 12 months, due to a fall in the overvalued $US and a narrowing in the interest rate differential between the Fed and the RBA. A recession and/or a Trump victory are the main downside risks.

Oliver's insights - Trump challenges and constraints

19 November 2024 | Blog Why investors should expect a somewhat rougher ride, but it may not be as bad as feared with Donald Trump's US election victory. Read more

Econosights - strong employment against weak GDP growth

18 November 2024 | Blog The persistent strength in the Australian labour market has occurred against a backdrop of poor GDP growth, which is unusual. We go through this issue in this edition of Econosights. Read more

Weekly market update 15-11-2024

15 November 2024 | Blog Global share markets were messy over the last week, not helped by the ongoing rise in bond yields and a wind back in Fed rate cut expectations after some elevated US inflation data and slightly hawkish comments from Fed chair Powell. Read moreWhat you need to know

While every care has been taken in the preparation of this article, neither National Mutual Funds Management Ltd (ABN 32 006 787 720, AFSL 234652) (NMFM), AMP Limited ABN 49 079 354 519 nor any other member of the AMP Group (AMP) makes any representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided and must not be provided to any other person or entity without the express written consent AMP. This article is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives and does not constitute a recommendation, offer, solicitation or invitation to invest.

The information on this page was current on the date the page was published. For up-to-date information, we refer you to the relevant product disclosure statement, target market determination and product updates available at amp.com.au.