Investment markets and key developments

Share markets continued their recovery over the last week helped along by expectations that “Goldilocks” conditions will prevail, with a further slowing in US inflation leaving the Fed on track to cut rates and reasonable economic data helping allay recession fears for now. US shares rose 3.9% for the week making it their strongest week for the year, Eurozone shares rose 3.1% and Japanese shares gained 8.7%. Chinese shares rose 0.4% supported by hopes for more policy stimulus after more soft economic data. Helped by the positive global lead and a reasonable start to the June half profit reporting season, Australian shares rose by 2.5% with gains led by IT, retail and financial shares but mining stocks down on the back of lower iron ore prices. Bond yields fell in the US, UK and Australia, were flat in Germany and rose slightly in Japan. Oil prices fell but only by 0.2% as uncertainty remains around whether Iran will retaliate for Israel’s assassination of Hamas’ leader in Iran. Copper and metal prices rebounded, and the gold price rose to a record high, but the iron ore price continued to slide on worries about Chinese demand. The $A rose and the $US fell consistent with the “risk back on” tone in other financial markets.

Shares remain at high risk of further falls and volatility over the next few months. Shares have seen a strong rebound from their lows earlier this month, recovering about two thirds of their losses. They have been helped by ongoing indications of central bank rate cuts, okay US economic data and mostly good earnings results. Further gains are possible, particularly as US data is unlikely to indicate recession is upon us just yet. However, shares remain vulnerable to further volatility over the next few months as: valuations remain stretched; investment sentiment is still relatively upbeat (with VIX or the “fear index” back to late July levels) which is negative from a contrarian perspective; recession risk is high in the US and Australia with forward looking jobs indicators pointing down; and geopolitical risk is high particularly around the US election and the Middle East; and we have only just started in the seasonally weak period of August and September which can sometimes extend into October/November in US election years.

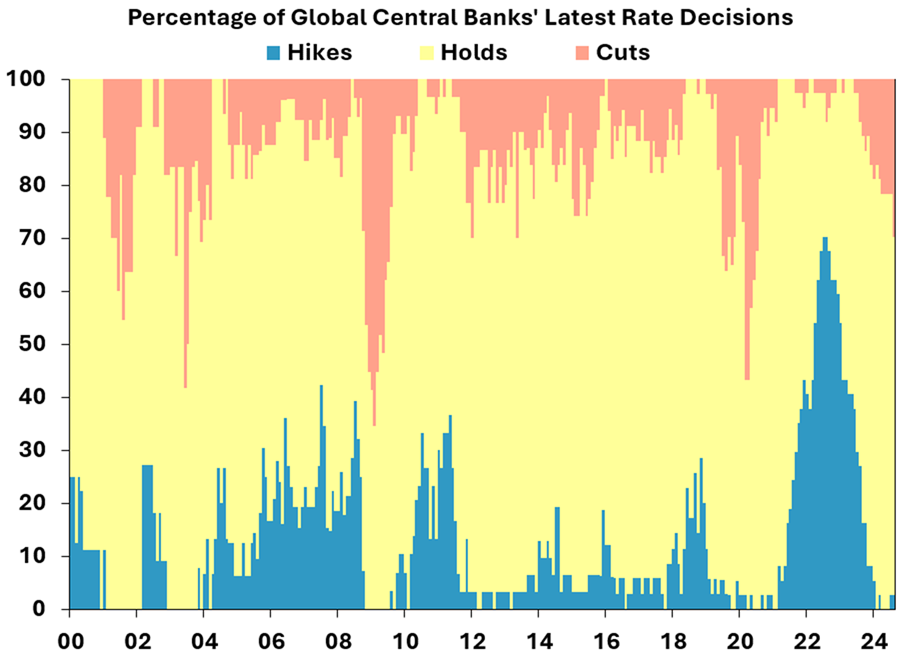

The good news though is that the drum beat of global rate cuts continues with nearly a third of global central banks now cutting rates.

Source: Bloomberg, AMP

- The Fed is on track to start cutting in September. Benign US CPI and producer price inflation data for July indicate ongoing progress in getting inflation back to target. And Fed officials are starting to focus more on the cooling jobs market. A 0.5% cut is possible but in the absence of much weaker jobs data ahead of the 18 September meeting a 0.25% cut is more likely. The US money market though has priced in a 75% chance of a 0.5% cut in September and four cuts by year end.

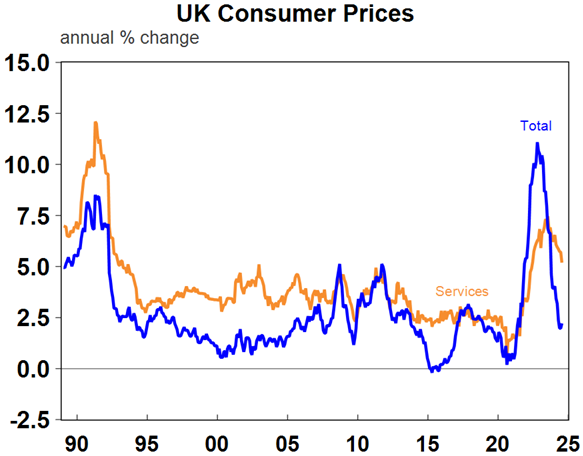

- The Bank of England looks on track to cut rates at least twice more this year. UK inflation in July rose less than expected and core and services inflation fell more than expected. The still high level of services inflation of 5.2%yoy, wages growth at 5.4%yoy and unemployment at 4.2% leave a September cut unclear but it’s likely to cut twice more this year.

Source: Bloomberg, AMP

- The Reserve Bank of New Zealand joined the global rate cutting cycle, cutting its cash rate by 0.25% to 5.25%. It now projects its cash rate falling to 4.92% by year end and 3.85% by end 2025. Don’t forget that back in May it considered a rate hike!

None of this means that the RBA will automatically follow. But just as Australia followed global inflation and rates up in 2022 – despite some saying we wouldn’t because we were different – it’s likely to follow on the way down in the next six months. Yes, disinflation stalled in the June quarter, but it did in the US in the March quarter too. And underlying economic variables are not that different to many countries that are now starting to cut rates – eg, unemployment is similar to that in the US and UK and wages growth has been lower than in the US, UK, Canada and New Zealand. So, while Governor Bullock in Parliamentary testimony reiterated the message that the RBA “does not expect that it will be in a position to cut rates in the near term”, we continue to see it starting to cut in February on the back of slower growth, higher unemployment and lower inflation than its currently forecasting.

Source: Macrobond, AMP

That said, the RBA’s return to time-based interest rate guidance after seemingly swearing off it after the 2021-22 “no rate hike before 2024” experience is surprising. Its current guidance is qualified by being based on “what the Board knows at present” and the Governor noted that “circumstances may change” giving the RBA an off ramp in the event of much weaker economic data or a financial shock – but then the 2021 guidance was qualified too, and the current guidance is getting reported as “ruling out rate cuts this year”. That said, there will be much less community annoyance with an earlier cut as opposed to the response to the start of hikes in 2022!

One concern in Australia remains the role that the public sector is playing in boosting inflation. It’s evident in strong public sector spending, wages growth now being strongest in government related sectors and consumer prices in areas administered by government rising faster than elsewhere. While some of this has arguably been well meaning – eg the rapid growth in NDIS spending and wage rises for aged care workers – as a whole it is working against the RBA’s efforts to cool things down and keeping interest rates higher than would otherwise be the case.

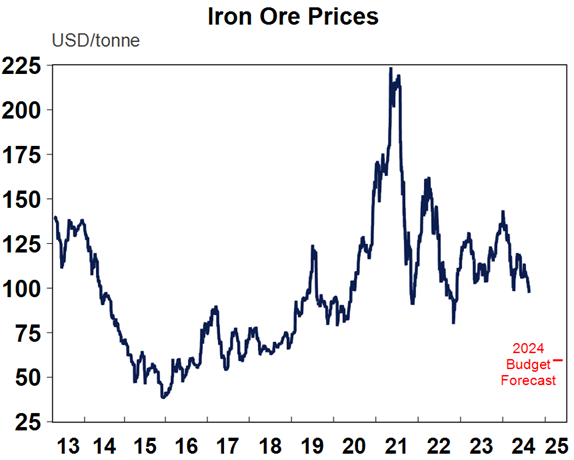

Falling iron ore price reducing the odds of another budget surplus. Over the last two years the Government has been a beneficiary of windfall revenue gains driving budget surpluses. A big part of this was higher than expected iron ore prices. This is now under threat again with the iron ore price falling again on the back of worries about Chinese demand in the face of weaker growth and stockpiles. So far the iron ore price is still well above the Budget assumption of a fall to $US65 a tonne by March quarter next year. But it still faces more short-term downside risks and the lower it is the less the windfall tax revenue going to Canberra, making it unlikely the Government will see another “surprise” Budget surplus this year and removing the Government’s key defence against arguments that its adding to inflation.

Source: Macrobond, AMP

Being 16 August, I couldn’t resist a homage to Elvis with the PNAU Suspicious Minds/Any Day Now mash up.

Major global economic events and implications

US economic data released over the last week was mixed but still consistent with slower but okay growth. On the positive side retail sales rose more than expected in July, jobless claims fell again partly reflecting the unwinding of impacts from Hurricane Beryl and small business confidence rose in August. Against this though industrial production fell more than expected in July (again partly due to Hurricane Beryl), the August Philadelphia Fed manufacturing conditions index fell sharply and while the New York Fed index improved slightly both remain soft (and these regions were not affected by Hurricane Beryl), housing starts fell sharply partly due to Hurricane Beryl but permits and the August home builders’ conditions survey also fell further. The overall picture is that the economy has likely slowed a bit but is continuing to grow supporting expectations for a soft landing. But recession risk still remains high given the ongoing inverted yield curve, large slump in the US leading index and the ongoing deterioration in forward looking jobs data along with the rising trend in unemployment.

Source: Macrobond, AMP

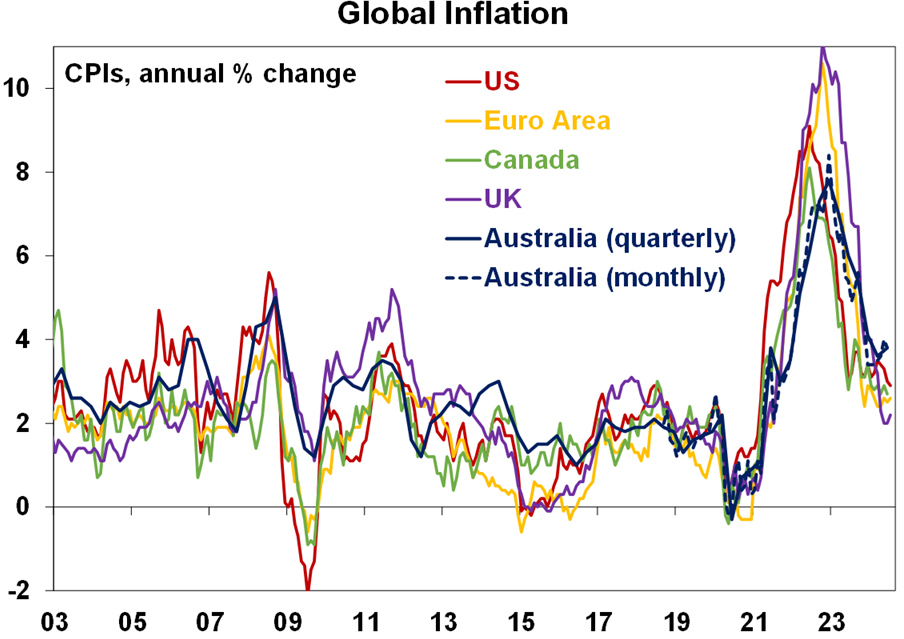

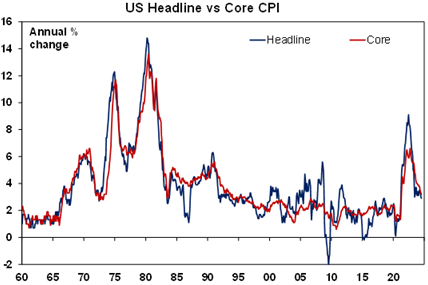

US inflation in July was benign and saw a further fall. Headline and core inflation rose 0.2% which saw headline inflation fall to 2.9%yoy and core inflation fall to 3.2%yoy. In particular, the share of items seeing annualised inflation greater than 3% has plunged to levels last seen prior to the pandemic. Combined with softer than expected producer price inflation it points to core PCE inflation for July of 0.15%mom or 2.6%yoy. Ongoing disinflation leaves the Fed on track for a cut next month, but in the absence of more broadbased weakness in economic data, this looks like being a “good cut” (reflecting lower inflation) rather than a bad cut (responding to plunging economic conditions) and its more likely to cut by 0.25% rather than by 0.5%. So “Goldilocks” continues to prevail for now.

Source: Bloomberg, AMP

Eurozone data was soft with a sharp fall in the ZEW survey.

UK jobs data was stronger than expected resulting in a surprise fall in unemployment to 4.2%. Wages growth slowed but remains high at or 5.4%yoy excluding bonusses. And inflation rose to 2.2%yoy, but it was less than expected and core and services inflation while still high fell to 3.3%yoy and 5.2%yoy.

Source: Bloomberg, AMP

Japanese growth stronger than expected. June quarter GDP accelerated to 0.8%qoq, after a 0.6%qoq fall in the March quarter. It was driven by consumer spending and capex with slight detractions from inventories and net exports. It’s still down 0.8%yoy though.

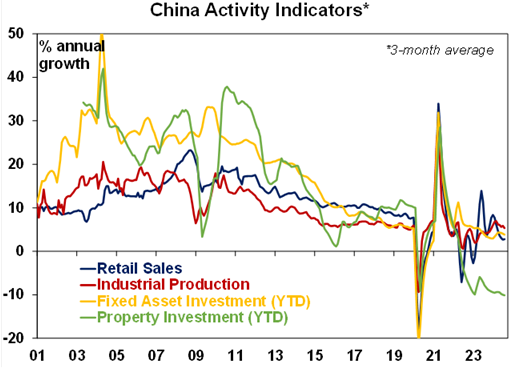

Chinese July data was softish. Retail sales growth rose a bit more than expected, but at 2.7%yoy remains weak and growth in industrial production and fixed asset investment slowed with property indicators staying weak. Chinese bank lending and credit was weaker than expected, with new loans to the real economy down for the first time in 19 years. Expect more incremental fiscal stimulus to just keep GDP growth around 4.5-5% this year.

Source: Bloomberg, AMP

Australian economic events and implications

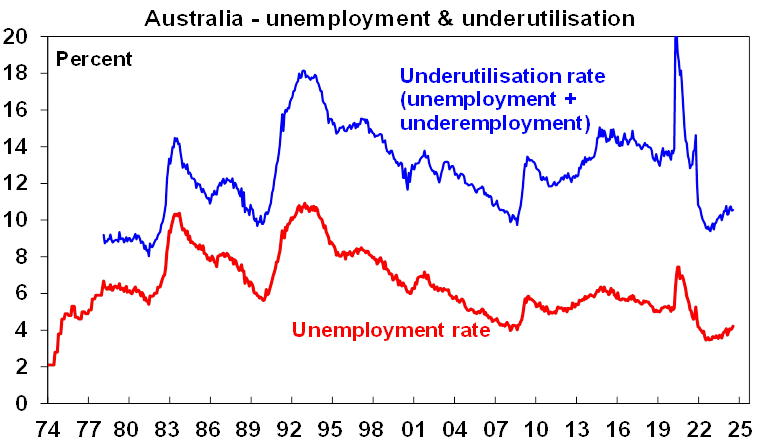

July jobs data was mixed. Employment growth was solid and hours worked rose but unemployment rose again to 4.2% as labour market participation rose to a record high (likely due to immigrants having a higher share of working age people than the existing population along with cost of living pressures forcing more to seek work) and population growth remains very strong. Overall, the labour market is continuing to gradually cool with the rising trend in unemployment indicating that the demand for labour is not quite keeping up with strong growth in the supply of workers and labour underutilisation at 10.6% is well up from its November 2022 low.

Source: ABS, AMP

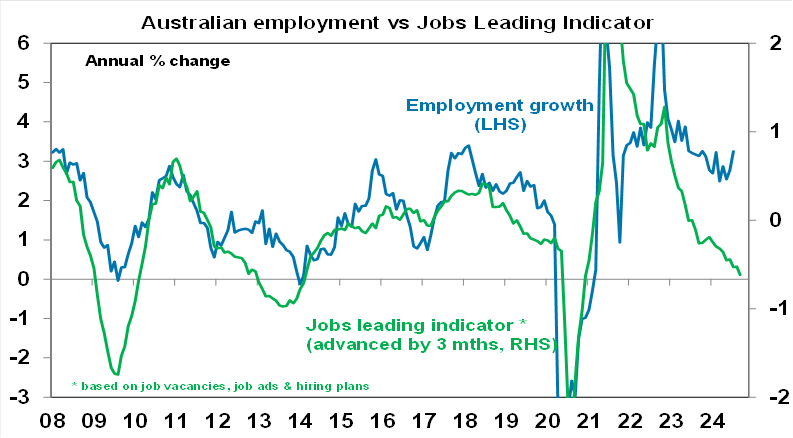

The jobs data likely helps keep the RBA in a holding pattern for now as the labour market is still tight but it is gradually cooling, and the RBA – just like the Fed – does not want to knock it over the edge. With the rise in unemployment due to a rising labour supply, it’s not as bad as a rise in unemployment on the back of job losses. So, it won’t rush the RBA into rate cuts. But it’s still a cooling in the labour market and forward-looking labour market indicators – like job ads and hiring plans - continue to point to slower jobs growth ahead. This is reflected in our Jobs Leading Indicator. Lately it’s been working better for hours worked than employment, suggesting a degree of labour hoarding by employers. But it’s doubtful this will be sustainable if consumer demand growth remains weak as employers will then likely lay off more workers.

Source: ABS, AMP

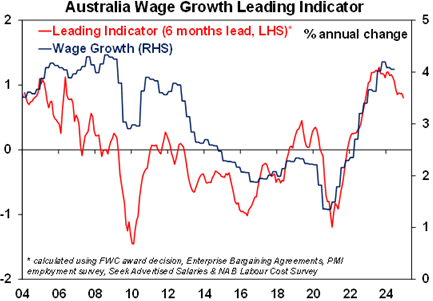

Wage growth past the peak. June quarter data showed wages growth of 0.8%qoq and 4.05%yoy. The annual growth rate was a bit higher than expected due to revisions to past quarters, but the quarterly increase was slower than consensus and RBA expectations and adds to evidence that wages growth is past the peak. While public wages growth is yet to start slowing, there are increasing signs of a slowing in the private sector where quarterly wages growth slowed to 0.7%qoq its lowest since December quarter 2021 and the proportion of private workers getting a wage rise in the quarter (11%) and their average wage rise (4.2%) has slowed from a year ago. What’s more the September quarter spike in wages this year will be well down on previous years due to the lower rise in award wages this year, increases under enterprise bargaining agreements look to have peaked and the slowing jobs market evident in a rising trend in unemployment and falling job vacancies point to less bargaining power all of which points to a further slowing in wages growth by year end. This is consistent with the signal from our Wages Growth Leading Indicator which is slowing. Annual wages growth at just over 4% remains too high relative to productivity growth to be consistent with the 2-3% inflation target and so will leave the RBA on edge, but the evidence is growing that its cooling so overall we see the wages data as consistent with the RBA leaving rates on hold for now as opposed to hiking.

Source: Bloomberg, AMP

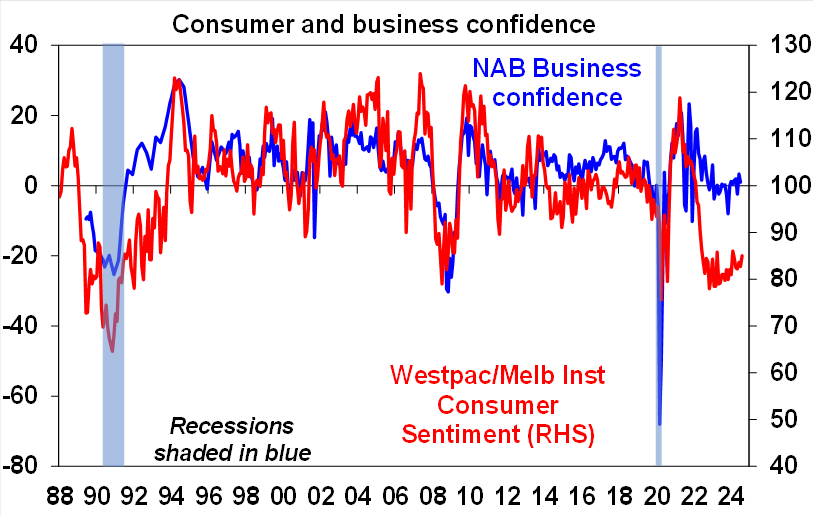

Consumer confidence rose in August. Tax cuts, rates on hold and slight increases in real wages are all helping drive a slight rising trend. It remains depressed though as real wages are down 5% from the end of 2021 and high rates remain an ongoing drag.

Source: Westpac/Melbourne Institute, AMP

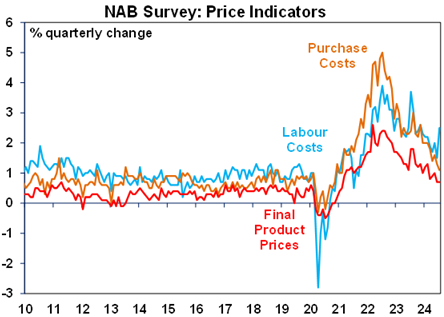

While the July NAB business survey showed a lift in business conditions, the trend remains down, and business confidence fell. The NAB survey showed that labour cost growth rose in July reflecting the annual award wage rise (although far less than last year) but growth in purchase costs & final product prices continue to trend down which is good news for inflation.

Source: NAB, AMP

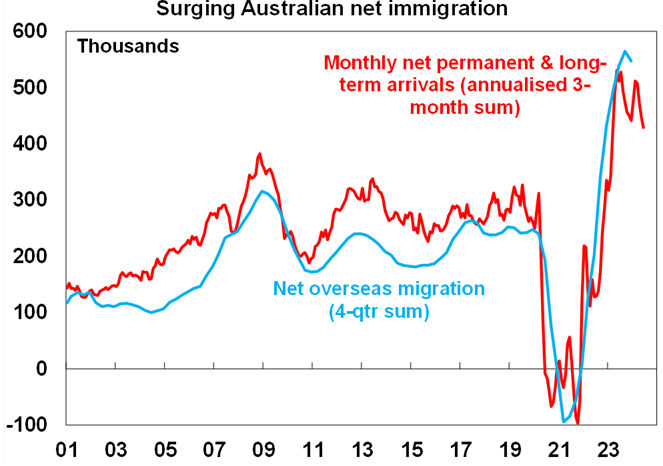

More signs that population growth is slowing. July net permanent and long-term arrivals data point to still strong but slowing immigration levels into Australia.

Source: ABS, AMP

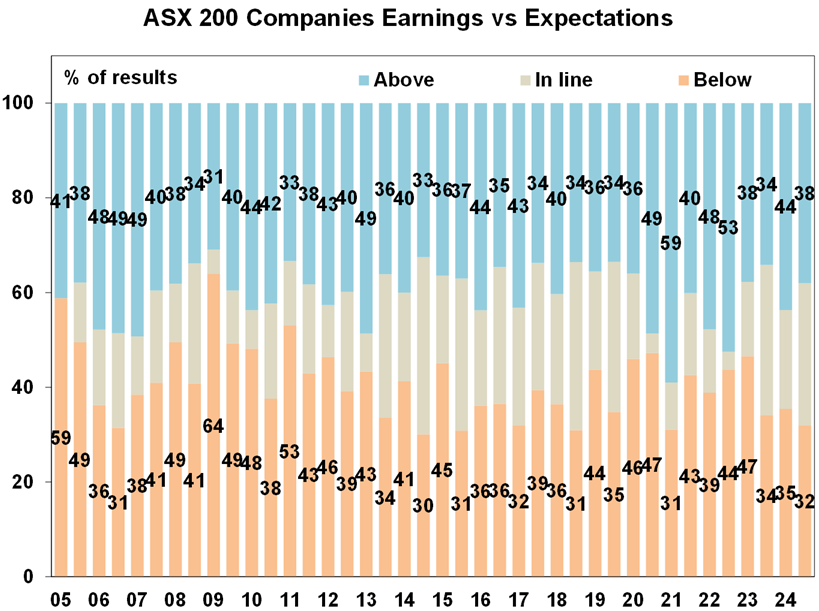

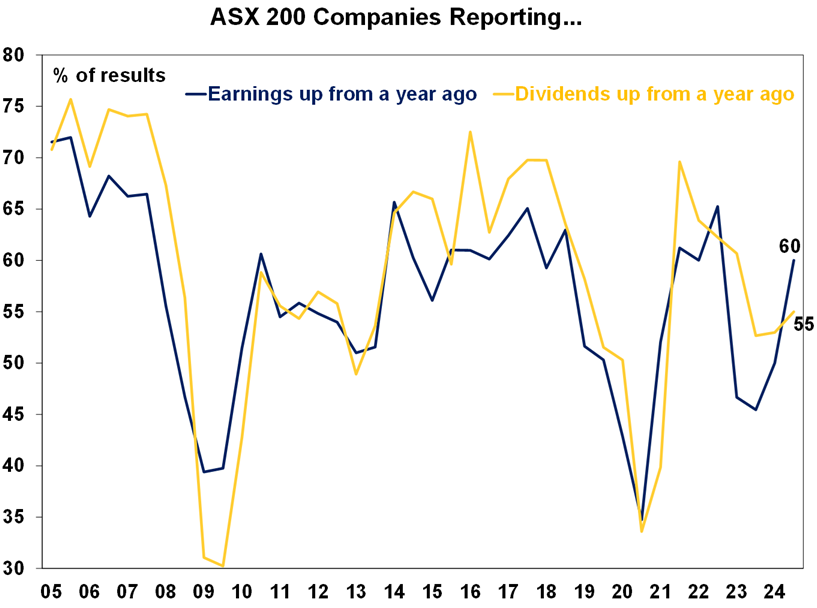

Its early days in the Australian June half earnings reporting season with only about a third of major companies having reported. So far results have been okay with slightly less than normal upside surprise, but also less than normal downside surprise and an increase in the number of companies reporting profits or dividends up on a year ago compared to the December half reporting season. Consensus expectations are for a 3.6% fall in profits in 2023-24 with a big fall in energy sector profits on the back of lower oil, coal and gas prices and small falls in profits in the mining, consumer staples, IT and financial sectors but other sectors seeing profit gains. The signal on consumer spending has been soft with sales generally down and media advertising weakening, although some like JB HiFi have come in better than expected. CBA reported a less than expected fall in profits, but both CBA and NAB reported increasing loan arrears albeit from a low base. The ongoing high level of interest rates is also evident in REA and Domain results benefitting from higher listings, an increasing amount of which are likely distressed. Overall, investors appear to be looking through the mixed picture with hopes for relief ahead from lower interest rates. Just bear in mind though that there is a tendency for companies with good results to report early so results may soften over the next couple of weeks. This may reflect many of the biggest, and hence more resilient, companies reporting early in the reporting season.

- So far 38% of results have surprised consensus earnings expectations on the upside which is less than the norm of 40%, but on the other hand 32% have surprised on the downside which is also less than the norm of 41%. So not great, but okay.

Source: Bloomberg, AMP

- 60% of companies have seen earnings rise on a year ago, and this is better than the norm of 56%. But don’t forget that falls in profits in 2023-24 are likely to be concentrated in energy stocks.

- 55% of companies have increased their dividends on a year ago which is below the norm of 59%, suggesting some caution.

Source: Bloomberg, AMP

What to watch over the next week?

In the US, the minutes from the Fed’s last meeting (Wednesday) will likely confirm that it’s gaining more confidence that inflation is falling to target and reinforce expectations for a start to rate cuts next month. Fed Chair Jerome Powell’s comments at the Jackson Hold central bankers gathering (Friday) will likely also take a dovish stance preparing the way for a September rate cut. He will also be watched for any signs of support for a bigger than normal cut as the focus shifts towards the employment side of the Fed’s mandate, but it’s doubtful he would support that at this stage. The subject of the 2024 Jackson Hole symposium is “Reassessing the Effectiveness and Transmission of Monetary Policy.” On the data front, existing and new home sales (Thursday and Friday) are likely to see modest gains after recent falls and August business conditions PMIs (Thursday) are likely to soften.

Canadian inflation (Tuesday) for July is expected to edge lower to 2.4%yoy, with core measures also likely to fall slightly.

Eurozone business conditions PMIs (Thursday) are likely to remain soft). The Swedish central bank (Tuesday) is expected to leave rates on hold.

Japanese business conditions PMIs (Thursday) are likely to remain okay. Inflation for July is likely to fall back to 2.7%yoy with core inflation falling to 1.7%yoy.

In Australia, the minutes from the last RBA meeting (Tuesday) are likely to reinforce the Bank’s somewhat hawkish stance on interest rates. The business conditions PMIs for August (Thursday) is likely to remain subdued.

The Australian June half profit reporting season will see its busiest week with 64 major companies reporting including GPT, Lend Lease, BlueScope and Suncorp (Monday), Ansell, Monadelphous and Hub24 (Tuesday), Santos, Breville and IAG (Wednesday), Medibank Private, Sonic and Stockland (Thursday) and the Latitude (Friday). Key to watch will be guidance around how the consumer is holding up with high interest rates and cost of living pressures along with indications around input cost pressures and pricing power. It’s a bit of a make-or-break earnings season in terms of guidance because after two years of earnings falls, they are expected to rebound to 4.8% growth this financial year.

Outlook for investment markets

Easing inflation pressures, central banks moving to cut rates and prospects for stronger growth in 2025-26 should make for reasonable investment returns over 2024-25. However, with a high risk of recession, poor valuations and significant geopolitical risks particularly around the US election, the next 12 months are likely to be more constrained and rougher compared to 2023-24 and there is a high risk of a further correction in the next few months.

A recession is the main threat for shares and there is a risk that we may have already seen the high for the year in the Australian share market after it reached our year-end target of 8100 in early August.

Bonds are likely to provide returns around running yield or a bit more, as inflation slows, and central banks cut rates.

Unlisted commercial property returns are likely to remain negative due to the lagged impact of high bond yields and working from home reducing office space demand.

Australian home prices are likely to see more constrained gains over the next 12 months as the supply shortfall remains, but still high interest rates constrain demand and unemployment rises. The delay in rate cuts and talk of rate hikes risks renewed falls in property prices as its likely to cause buyers to hold back and distressed listings to rise.

Cash and bank deposits are expected to provide returns of over 4%, reflecting the back up in interest rates.

A rising trend in the $A is likely taking it to $US0.70 over the next 12 months, due to a fall in the overvalued $US and a narrowing in the interest rate differential between the Fed and the RBA. A recession is the main downside risk.

Weekly marketing update 29-11-2024

29 November 2024 | Blog Shares have been mixed over the last week with lots of noise around Trump including tariff posts, political uncertainty in France and another elevated inflation reading in the US, but mostly solid US economic data and news of a cease fire between Israel and Hezbollah. Read more

Weekly market update 22-11-2024

22 November 2024 | Blog Against a backdrop of geopolitical risk and noise, high valuations for shares and an eroding equity risk premium, there is positive momentum underpinning sharemarkets for now including the “goldilocks” economic backdrop, the global bank central cutting cycle, positive earnings growth and expectations of US fiscal spending. Read more

Oliver's insights - Trump challenges and constraints

19 November 2024 | Blog Why investors should expect a somewhat rougher ride, but it may not be as bad as feared with Donald Trump's US election victory. Read moreWhat you need to know

While every care has been taken in the preparation of this article, neither National Mutual Funds Management Ltd (ABN 32 006 787 720, AFSL 234652) (NMFM), AMP Limited ABN 49 079 354 519 nor any other member of the AMP Group (AMP) makes any representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided and must not be provided to any other person or entity without the express written consent AMP. This article is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives and does not constitute a recommendation, offer, solicitation or invitation to invest.

The information on this page was current on the date the page was published. For up-to-date information, we refer you to the relevant product disclosure statement, target market determination and product updates available at amp.com.au.