Investment markets and key developments

It was all about the US Presidential election this week. Despite concerns that the election outcome would be extremely close, the Republican victory was stronger than the polls and betting markets were suggesting into the lead up. Trump’s re-election into the White House led to a big rally in sharemarkets (US is up 4.7% over the week to a record high, Australia +2.2%, Eurozone was down by 1.6% and Chinese shares up by 5.5%), some initial rise in bond yields which faded by the end of the week, a rally in cryptocurrencies (with Bitcoin reaching a record high of over $95K) and a slightly higher US dollar (with the $A down to 0.6583USD).

Trump will become the 47th President of the US. This is only the second time since 1892 that a president has won a second, non-consecutive term. Trump again won the “Rust Belt” or working class states of Pennsylvania, Michigan and Wisconsin (like in 2016) reflecting the manufacturing “recession” in the US manufacturing sector and household concern about high inflation and the subsequent deterioration in real wages growth. The Republicans won 301 seats in the Electoral College (versus 226 for the Democrats), with 270 needed for a majority, 51.4% of the popular vote and a majority (53 v 46 seats) in the Senate. Counting is still ongoing for the House of Representatives, which so far has 211 seats for the Republicans (versus 200 seats for the Democrats), with 218 needed for a majority. So, while there hasn’t technically been a “Red Sweep” yet it could still happen.

The makeup of Congress (i.e. if the Republicans win the House) is important because it will determine the Republicans ability to pass policies which impact government spending and revenue measures (i.e. everything related to the budget). Keep in mind though that the Republicans would need more than a simple majority in the Senate (60 votes) to pass any policies (which they don’t have) so would need to pass any measures via “Budget Reconciliation” which is what happened with Trump 1.0 but this also has limits around the impact of any spending measures on the budget deficit over the forward years.

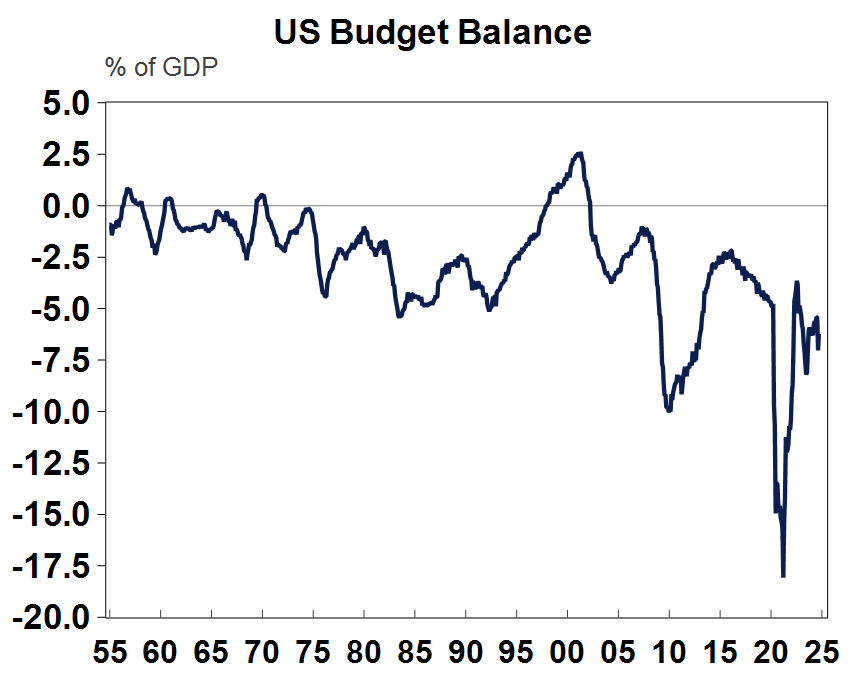

Our Chief Economist Shane Oliver wrote a note this week about the implications of a Trump 2.0 Presidency here. To summarise, the main impacts from Trump 2.0 are: an extension of personal income tax cuts, lower corporate taxes which will be easier to do if the Republicans control the House and Senate, some cut to government spending (Trump wants to appoint Elon Musk to Department Of Government Efficiency or D.O.G.E which is why dogecoin has rallied this week) paid for by higher tariffs, further deregulation and a big rise in tariffs on US imports (particularly on Chinese imports). The market is focusing on the short-term stimulus measures of taxes and deregulation which will boost the budget deficit (already high at over 6% of GDP – see the chart below) which has led to a big rise in bond yields with the US 10-year at over 4.3%, its highest level since June but still below its highs a year ago (when yields closed in on 5%).

Source: Macrobond, AMP

So overall in the short-term, sharemarkets and cryptocurrencies can rally a bit further and US shares can outperform global shares. And bond yields can easily rise further on concern about the US fiscal situation but are unlikely to settle above 4.5%. Higher bond yields will also threaten equities, especially because of further compression to the equity risk premium. In the longer-term, the Trump administration may actually result in slower economic growth because of lower population growth (as the Republicans want to tighten border restrictions and deport some illegal immigrants) and through lower trade growth if tariff restrictions erupt into a global trade war. Everything will depend on the policies that are announced and the timing of these.

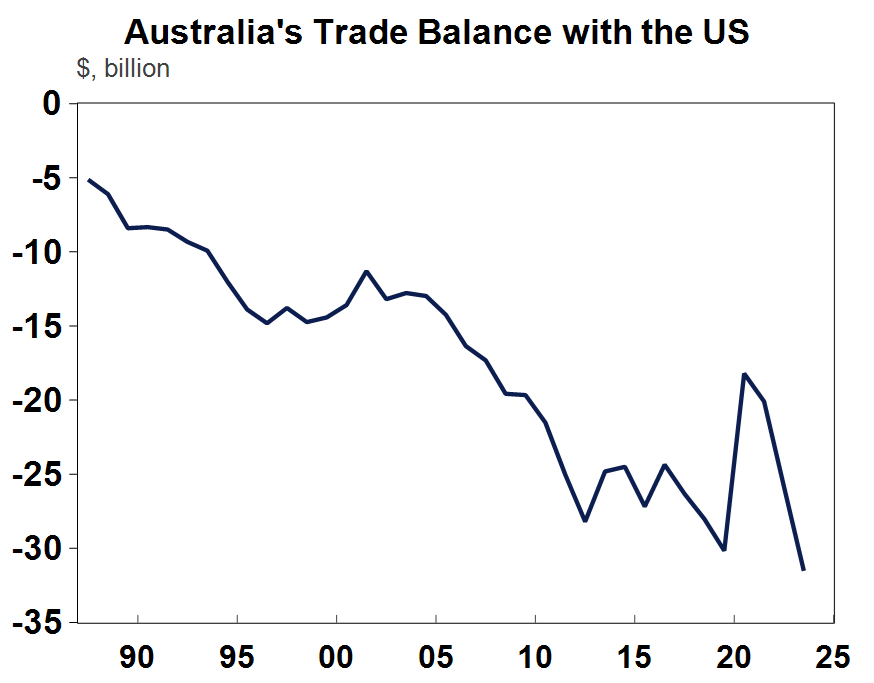

On the tariff front, Australia imports more from the US than it exports there, which means it runs a trade deficit with the US (see the chart below).

Source: Macrobond, ABS, AMP

This means that Australia will probably avoid being hit directly by tariffs because the point of the tariffs is for the US to reduce its reliance on global imports and produce them domestically. The impact from US tariffs will be more on the impact to global trade (likely to be a negative) and the larger impacts on China, which are likely to be hit by larger tariffs which could lead to lower Chinese exports and therefore lower demand for raw commodities (which will hurt Australia). The risk is that countries like China and Europe start imposing tariffs like in 2018 which would lead to market uncertainty and concern about a global trade war which would hit economic growth. But we don’t know how other countries would respond and if the tariff route is actually Trump’s “maximum pressure” strategy to get direct investment into the US economy, bypassing the tariff. As well, if China is hit with large tariffs which weakens growth, Australia may be able to find other markets for its exports (which is what happened in the recent trade dispute between Australia with China). And China may respond with large stimulus packages to offset the negative hit to the economy (which is why Chinese shares are rallying so hard). Basically, there are so many “known unknowns” and even “unknown unknowns” it’s not time to hit the panic button just yet! There is a well known saying now that we should “take Trump seriously but not literally” and giving direct point forecasts right now about the impact of the Trump administration on the economy is fraught with problems.

There are no implications to Australian monetary policy right now as a result of the Trump presidency. Inflation is being driven by “home grown” services inflation which are not impacted by changes to US politics. The most direct impact of any immediate reactions to the election is through the currency. A higher USD doesn’t necessarily lead to a lower Australian dollar (and therefore higher imported inflation) on the Australian Trade Weighted index if other currencies will decline against the USD. At the Senate Economics Legislation Committee this week, Governor Michelle Bullock and Assistant Governor for financial markets Chris Kent were grilled about their scenario analysis around a Trump presidency but they said it was too soon to make concrete judgements about policies that haven’t occurred yet. The RBA has to respond to actual conditions in the economy and does not set monetary policy for potential future conditions.

And going back to the RBA, the central bank met this week and left the cash rate unchanged at 4.35% at its meeting this week, where it has kept the cash rate for the past 12 consecutive months. This was universally expected by economists and financial markets. Economists expected that there could be some tweak to its neutral language, but the Board still maintained that it was “not ruling anything in or out” which means that the Board could still consider an interest rate hike – seems like a very small probability at a time of slowing inflation and sluggish growth. Financial markets have pushed back pricing for the first cut to May 2025 after the stronger labour force figures last month. We think the first cut could come sooner in February because we are more optimistic on inflation figures.

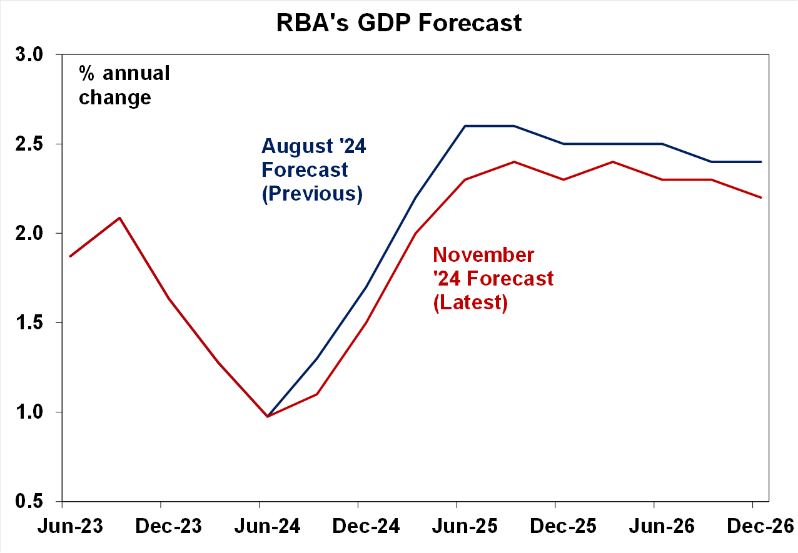

The RBA’s Statement on Monetary Policy included the RBA’s new forecasts. GDP growth was revised down, partly reflecting a slower pick-up in consumer spending (see the chart below). The RBA expected stronger pick up in consumption growth in September quarter.

Source: RBA, AMP

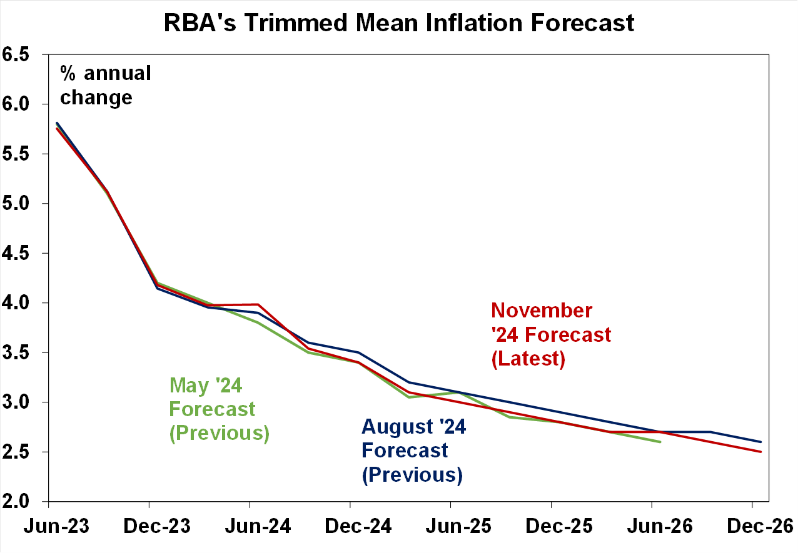

The RBA’s inflation forecasts were revised back down, similar to May levels (see the chart below). But underlying inflation (which is indicative of inflation momentum) is still too high, with the RBA forecasting inflation to be sustainably in the target band until the end of 2026.

Source: RBA, AMP

The US Federal Reserve met this week and delivered on expectations of a 0.25% rate cut, taking interest rates to 4.5%-4.75%, as was expected which takes total easing to 0.75% in this cycle. There was a slight change in the post-meeting statement, removing prior commentary that the Fed had greater confidence about inflation moving sustainably towards the target which some have interpreted to be a sign the Fed could skip a December rate cut. However, there are two more inflation reports before the December meeting which will give the Fed enough time to assess conditions. Markets are pricing in a another 3 rate cuts over the next 12 months which is a slow easing cycle. On the election, Powell said “in the near term the election will have no effect on our policy decisions” and that he would not step down as Chair if directed to by Trump (previously Trump said he would fire Powell although retracted those comments later on).

Source: Bloomberg, AMP

Major global economic events and implications

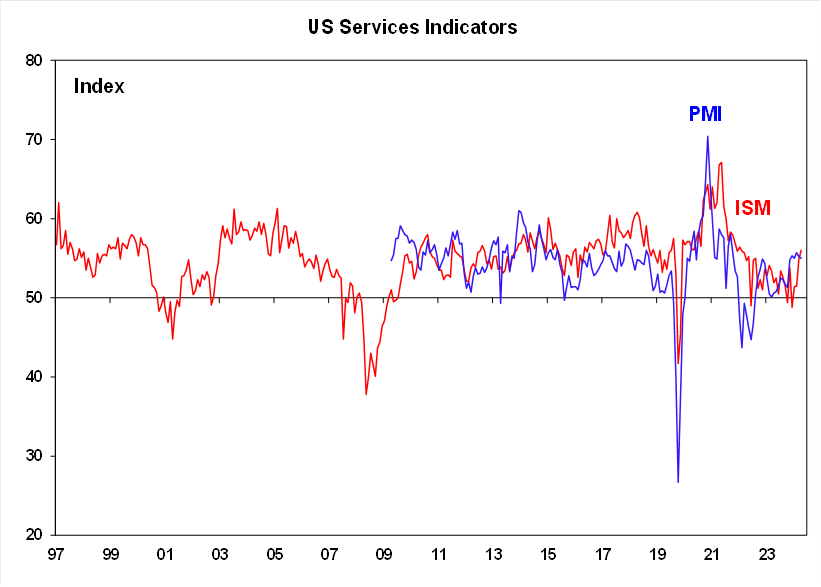

US data this week included factory orders which fell by 0.5% in September (as expected), the services ISM index rose to 56, with prices paid up, employment stronger but new orders softened (although were still positive). This is the same signal from the services PMI (see the chart below) which indicates that services activity is holding up in the US, at the expense of manufacturing.

Source: Bloomberg, AMP

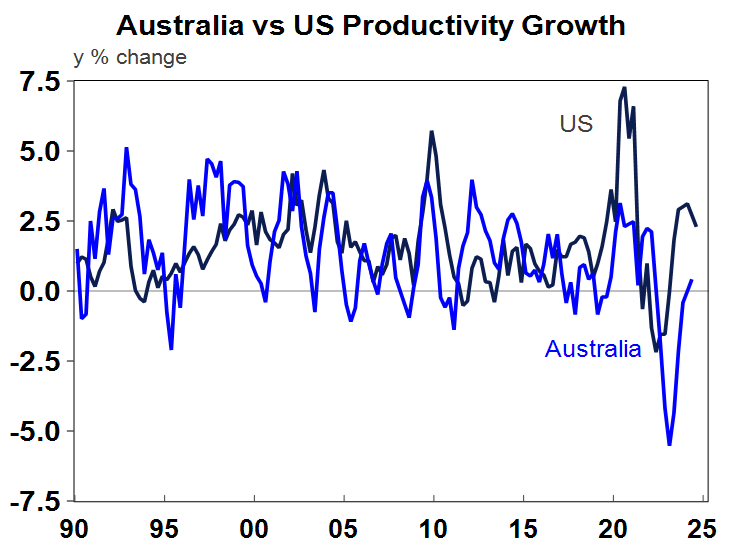

US consumer sentiment according to the University of Michigan improved in November, 1-year inflation expectations fell to 2.6% (from 2.7%) while 5-10 year rose to 3.1% (from 3%). US non-farm productivity growth was up by 2.2% in the September quarter (up from 2.1% last quarter) – well above Australia.

Source: Macrobond, AMP

US September quarter earnings are nearly complete with 90% of S&P500 companies having reported (Nvidia is still to come through). 75% of results have surprised on the upside, which is just below the norm of 76%. The final earnings growth number should come in around 7% yoy which is still good, but down from 11.6%yoy in the June quarter.

The Bank of England met this week and cut the policy rate by 0.25% to 4.75% which takes total easing to 0.50% in this cycle. The BoE signalled that a quarterly pace of rate cuts was likely from here, as services inflation is still high in the UK and fiscal stimulus in the near-term from recent government announcements will boost growth and upside risks to inflation.

Source: Bloomberg, Macrobond, AMP

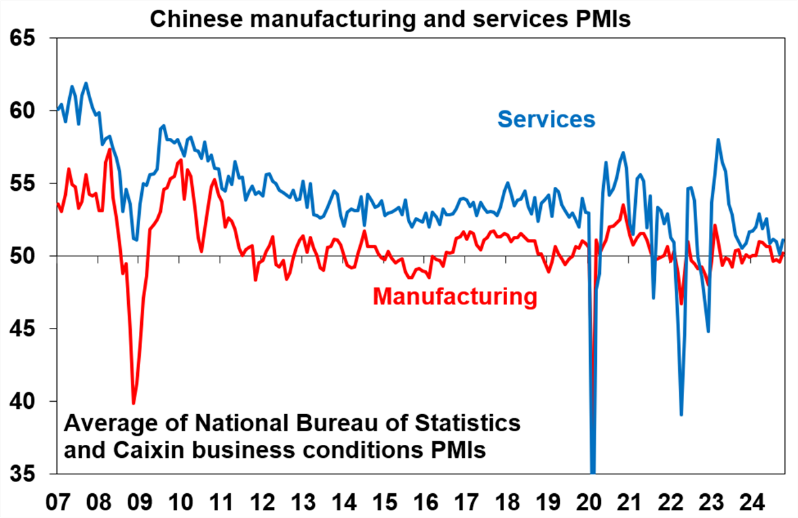

The Chinese Caixin services PMI improved in October to 52 (from 50.3 last month), another sign of a stabilisation in growth (see the chart below).

Source: Bloomberg, AMP

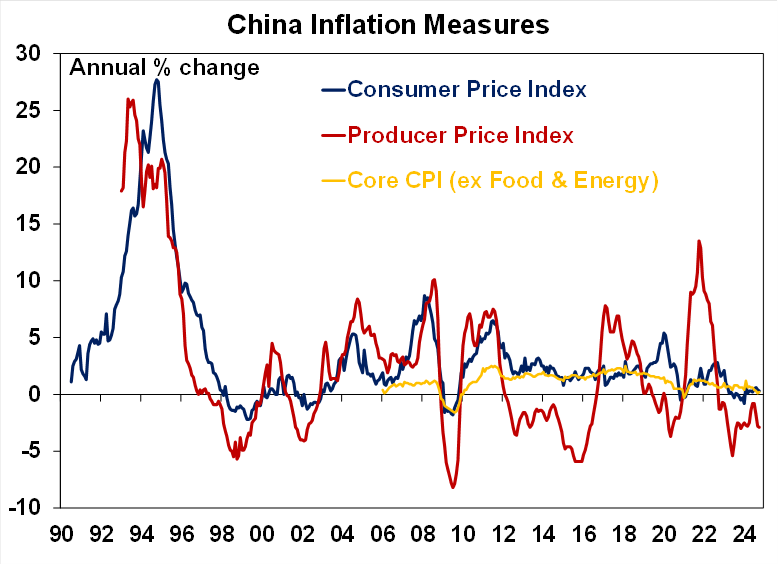

Chinese producer prices fell by 2.9% over the year to October and consumer prices were up by just 0.3%. The persistent of low price growth is a sign of the weakness in the consumption side of the Chinese economy.

Source: Bloomberg, AMP

There were high expectations that China’s National’s People Congress Standing Committee meeting which concluded this week would give some more clarity around the size of the fiscal stimulus but the outcome fell short of expectations. The sole focus of the meeting was the local government debt swap plan that is due to start immediately. The debt swap package is stimulus because it gives local governments room to spend. The finance minister said that Beijing is “actively planning the next steps of fiscal policy” including tax policies around the real estate market, issuing Special Sovereign Bonds, and local government special bonds. This stimulus may only arrive next year, especially once more is known around potential US tariffs on China. The disappointing Chinese fiscal stimulus risks some downside to Chinese sharemarkets which have been performing well on expectations of concrete details of the stimulus measures.

The New Zealand unemployment rate rose to 4.8% in September, up from 4.6% in the June quarter, but below expectations of 5%.

Source: Macrobond, AMP

Australian economic events and implications

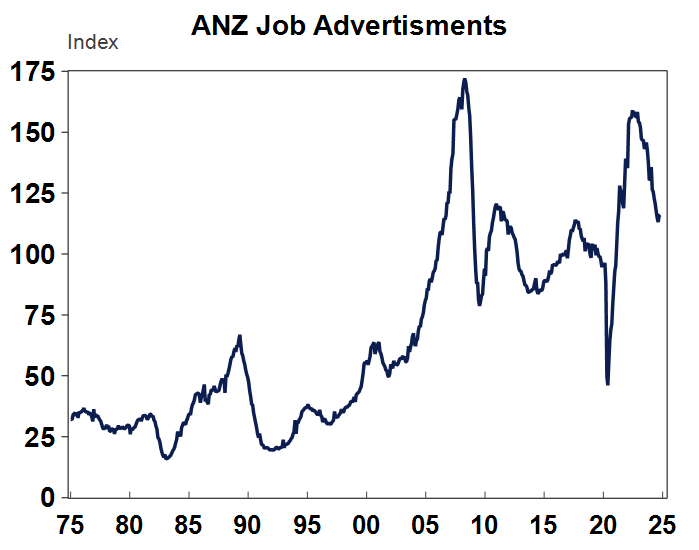

ANZ job ads rose by 0.3% in October but are down by 15.8% over the year (see the chart below) which shows that some moderation in employment growth is likely.

Source: Macrobond, AMP

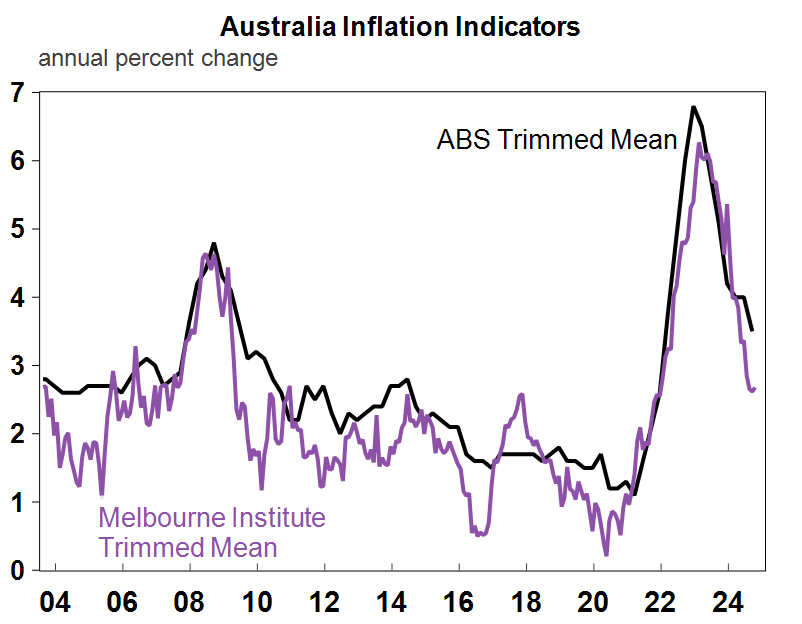

The Melbourne Institute inflation gauge on the trimmed mean measure ticked up to 2.7% year on year (see the chart below) but hasn’t been a great guide to inflation recently.

Source: Macrobond, AMP

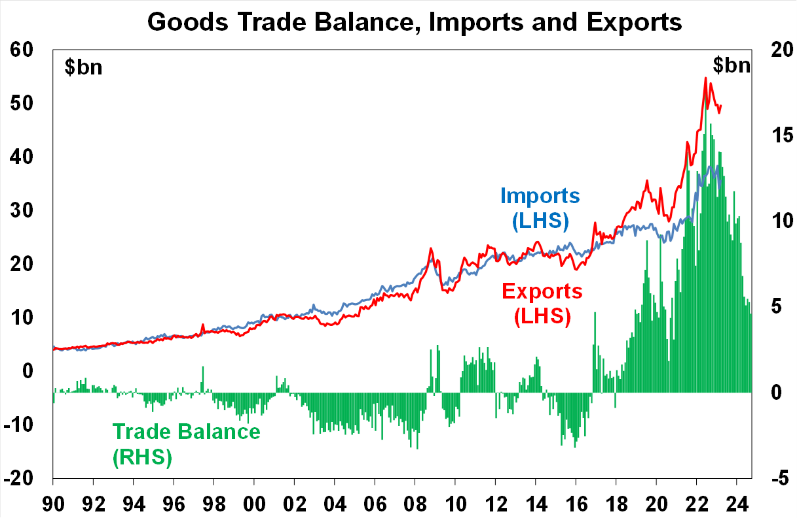

Australia’s trade balance narrowed in September to $4.6bn from $5.3bn last month, as export growth declined more than imports. However, our trade balance is still very high relative to historical averages (see the chart below). Net exports should add 0.3 percentage points to Q3 GDP growth.

Source: ABS , AMP

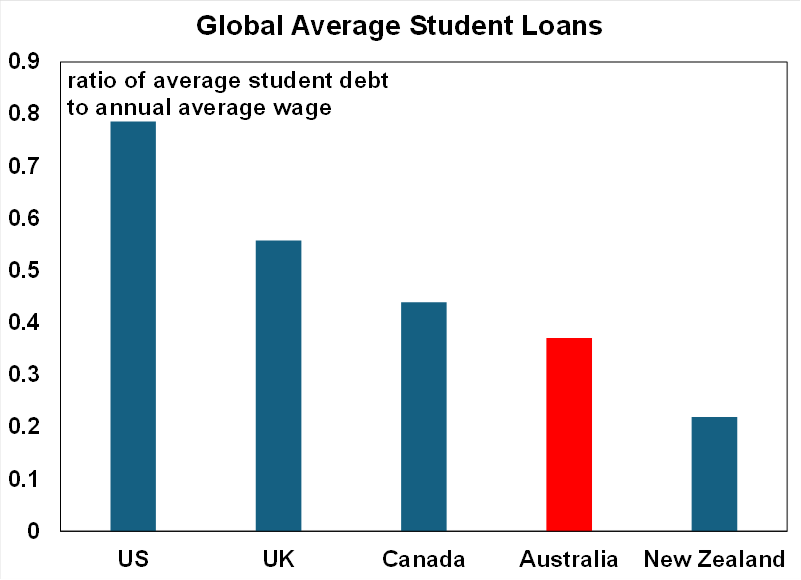

The Labor government announced a pre-election pledge to cut student debt by 20%, starting from 1 June 2025. The average student loan is $27,600 so this would save $5,520. This will cost the government $16bn (or more likely to be $11bn because not all student debt was going to be recouped) but won’t impact the budget because it is considered “off budget spending” (as student debt is a loan from the government) and doesn’t qualify as government expenditure (which is an “on” budget measure). The optics of this policy change is clear – intergenerational wealth inequality angst is very high as young people feel like owning a home is unattainable for them whilst baby boomers have enjoyed large gains in the property market over the last few decades. Student debt relief was popular in the US recently during the Biden administration when up to $20,000 in debt relief was wiped off. Australia’s student debt levels look reasonable relative to global peers (see the chart below) with the ratio of student debt to an annual average wage at 0.4 times – well below the US at nearly 0.8 times. The government’s other proposed policies to increase the minimum income before debt payments are necessary was a good change along with rolling back the increase in fees for some courses like arts and humanities while reducing costs for STEM subjects (implemented by the Morrison government). But, just cutting student debt as a once-off still means that the taxpayer will eventually pay for this policy.. in economics there is no such thing as a free lunch!

Source: Australia Treasury, Macrobond, Bloomberg, AMP

What to watch over the next week?

In the US the focus will be on the October consumer price data (released on Wednesday in the US). Headline CPI is expected to by up by 0.2% or 2.6% year on year. Core CPI is likely to rise by 0.3% or 3.3% year on year which will keep the Fed on track to slowly keep reducing interest rates.

There is also the NFIB small business optimism index to watch which may get a boost from the outcome of the election, New York Fed 1-year inflation expectations are expected to be unchanged at 3%. The October producer price data is expected to rise by 0.2% in headline terms (just under 3% year on year) or 0.3% in the core reading. October retail sales are expected to rise by a modest 0.3%m after a 0.4% lift last month. October industrial production is likely to fall by 0.3%. There is also a flurry of Fed speakers, with Powell the main one to watch. We also get some more reports from US companies around earnings season.

In Australia, the Westpac/Melbourne Institute November consumer sentiment reading should show further improvement, as the RBA kept rates steady. The NAB business survey for October. September quarter wages data is released on Wednesday. We expect quarterly growth of 0.9% (up from 0.8% last quarter because of the impact of the minimum and award wage increases) with annual growth at 3.6% which would still be in line with a slowing in the pace of wages growth. The October labour force figures are expected to show a slowing in employment growth, jobs up by 20K after months of strength and the unemployment rate rising to 4.2%. RBA Bullock speaks at a panel at the ASIC Annual forum in Sydney as does Brad Jones the following day.

In Europe, there is the ZEW business survey, Q3 GDP (annual growth is likely to be low at ~1%) and the October ECB meeting minutes.

Chinese economic data released next week includes industrial production, property investment, unemployment rate.

Outlook for investment markets

Easing inflation pressures, central banks cutting rates, China ramping up policy stimulus and prospects for stronger growth in 2025-26 should make for reasonable investment returns over the next 6-12 months. However, with a high risk of recession, poor valuations and significant geopolitical risks particularly around the Middle East and US election, the next 12 months are likely to be more constrained and rougher compared to 2023-24.

Bonds are likely to provide returns around running yield or a bit more, as inflation slows, and central banks cut rates.

Unlisted commercial property returns are likely to start to improve next year as office prices have already had sharp falls in response to the lagged impact of high bond yields and working from home.

Australian home prices are likely to see some further slowing over the next few months as the supply shortfall remains, but still high interest rates constrain demand and unemployment rises. Lower interest rates should help the market next year though and we see average property prices rising by around 5% in 2025.

Cash and bank deposits are expected to provide returns of over 4%, reflecting the back up in interest rates.

A rising trend in the $A is likely taking it to $US0.70 over the next 12 months, due to a fall in the overvalued $US and a narrowing in the interest rate differential between the Fed and the RBA. A recession and/or a Trump victory are the main downside risks.

Oliver's insights - staying focused as an investor

12 November 2024 | Blog Dr Shane Oliver suggests five ways to help manage the noise and stay focussed as an investor with the changes in the macro enviroment. Read more

Oliver's insights - elected President of the US

07 November 2024 | Blog The return of Donald Trump to the US presidency brings the prospect of more US tax cuts and deregulation, but also more tariff hikes and trade wars and policy uncertainty. Read more

Weekly market update 01-11-2024

01 November 2024 | Blog Global shares markets remained under pressure over the last week from bonds; US election implications; Australian inflation falls but still too high; RBA to hold but forecasted to soften slightly; and more. Read moreWhat you need to know

While every care has been taken in the preparation of this article, neither National Mutual Funds Management Ltd (ABN 32 006 787 720, AFSL 234652) (NMFM), AMP Limited ABN 49 079 354 519 nor any other member of the AMP Group (AMP) makes any representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided and must not be provided to any other person or entity without the express written consent AMP. This article is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives and does not constitute a recommendation, offer, solicitation or invitation to invest.

The information on this page was current on the date the page was published. For up-to-date information, we refer you to the relevant product disclosure statement, target market determination and product updates available at amp.com.au.