Investment markets and key developments

Share markets mostly rose over the last week, with US shares buoyed by increasing confidence in Fed rate cuts this year and strength in tech stocks, Eurozone shares boosted by reduced fears about the outcome of the French election and Japanese shares rebounding to a new high after a consolidation since March. Chinese shares fell though. Reflecting the positive global lead Australian shares rose around 0.6% driven by resources and property shares but other sectors fell. Bond yields were mixed – down in the US and much of Europe, but up in Germany, Japan and Australia. Oil, metal and iron ore prices rose as did the $A and the $US fell.

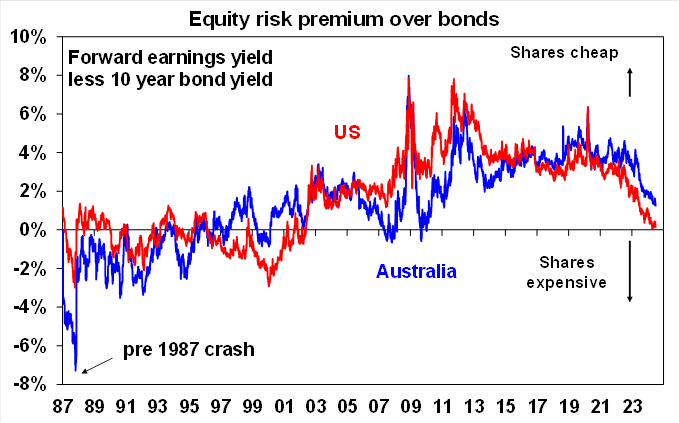

Expect a rougher more constrained ride from shares, but with a still rising trend over the next 12 months. The bad news is that shares are offering a low risk premium over bonds, investor sentiment is elevated (but at least not euphoric), US shares are increasingly relying on a narrow group of AI/tech stocks, the key US economy seems to be slowing rapidly (the Atlanta Fed’s GDPNow estimate for June quarter growth has plunged from 4.2% annualised to just 1.5% since mid-May) risking recession which would be bad for earnings expectations and geopolitical uncertainty is on the rise again with the French election, the US election and ongoing issues in the Middle East and Ukraine. This risks a deeper correction in the seasonally weak August/September period and more volatility. The good news though is that central banks are getting back on track for more rate cuts which should boost growth expectations for 2025-26 and lower bond yields ultimately supporting share returns.

Source: Bloomberg, AMP

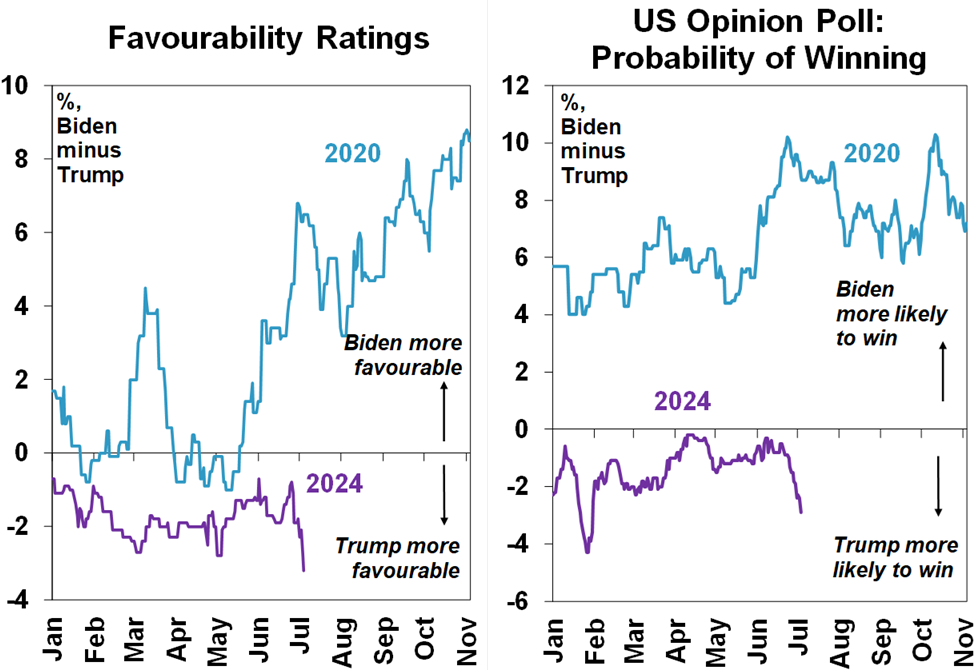

With increasing talk Biden will be replaced as the Democrat candidate and Trump’s lead continuing to widen to now around 3% in general polls and the PredictIt betting market putting the Republican’s probability of winning at 59% versus the Democrat’s (whether Biden or a replacement) at 45% the focus will increasingly turn to Trump’s policies. Tax cuts and deregulation will be cheered by share markets – but his policies for much higher tariffs on imports, lower immigration and a less independent Fed suggest higher inflation with more tax cuts likely to add to the already big US budget deficit (which is around 7% of GDP) all of which is bad for bonds and could put pressure on share market valuations. Of course there is a way to go yet.

Source: Real Clear Politics, Bloomberg, AMP

Bond vigilantes and the French election. The first round French parliamentary election that saw the far-right National Rally “win” but with a slightly lower percentage of the vote than indicated in polls (33% v 36%) and the withdrawal of left and centre candidates going into the final round as part of a “cordon sanitaire” to reduce 3 way races that would split the vote and favour NR has seen some easing in fears of another Eurozone crisis including some easing in the spread between French and German bond yields. Going into this Sunday’s second round election, NR are likely to get more seats than any other alliance but probably not enough to form government. A hung parliament would not be good in terms of reducing the deficit and implementing reform – but could be seen as a least bad outcome for markets as it would reduce the chance of a conflict over fiscal policy and head off extremist NR policies. By contrast if NR is able to form government it would add to fears of conflict with the European Commission over fiscal policy which could if NR digs its heals in set off another crisis. That said its worth bearing in mind that the NR is unlikely to go down the path of trying to leave the Euro as it is popular in France. Secondly, just as surging bond yields – the “bond vigilantes” – headed off economically irresponsible fiscal policies in parts of Europe through the Eurozone crisis last decade, notably in Greece (under far left Syriza in 2015), and also in the UK (under Truss) and in Italy in 2022 (under PM Meloni and the Brothers of Italy), the same would likely happen again if NR is able to form government and tries to do the same. Note bond investors are not being mean or vindictive but just trying to protect their investments – in other words the message to errant governments is “you can do whatever you want, but if it’s going to unsustainably blow out the budget deficit we won’t lend to you!” Finally, the ECB has tools that can be deployed to calm individual bond markets if necessary (providing the country meets certain criteria). That said it could be a bit rough for markets in the interim if NR is able to form a government. So, all eyes will be on the outcome from Sunday’s election.

The UK election as expected saw Labour returned to power with a huge majority, but its in a far more centrist iteration than on offer five years ago under Jeremy Corbyn so big policy changes are unlikely with little major market implications. Labour has promised a growth first strategy – which implies measures and reforms to boost growth rather than an old fashioned left wing big tax and spend program. So far they have only committed to very minor increases in taxes and only slightly higher public spending is expected. So, no Truss style budget shock is likely and not much if any impact on global markets.

Globally, progress towards lower interest rates continued over the last week. Softish US economic data, cautious but dovish leaning minutes from the Fed’s last meeting and comments by Fed Chair Power that recent inflation data “suggest we are getting back on a disinflationary path” reinforced expectations for the Fed to start cutting in September. ECB President Lagarde sounded cautious at the ECB’s conference in Sintra and inflation was mixed in June with a fall in headline inflation but core inflation unchanged at 2.9%, but the ECB still looks on track to cut rates again at its September meeting.

Source: Bloomberg, AMP

Australia remains the odd one out for now on interest rates. The minutes from the last RBA meeting provided no surprises but reiterated the RBA’s hawkish lean with the implication that it would raise rates again if it judges that inflation would not return to target by 2026 and/or it concludes that demand is not falling enough relative to supply. Higher than expected inflation and retail sales data and the continuation of home price gains since the last RBA meeting two weeks ago therefore add to the risk that the RBA will hike again to further bear down on demand and inflation.

However, we remain of the view that rates have peaked – here are seven reasons why. Put simply the RBA needs to be very wary of doing too much:

- the lagged impact of past rate hikes is still feeding through the economy with the RBA itself describing monetary policy as restrictive”;

- while retail sales in May were stronger than expected this looks distorted by earlier EOFY sales and the ABS’ May Household Spending Indicator is warning of a new leg down in already depressed consumer spending;

- the RBA is likely to revise down its growth forecasts heading off any upwards revision of its assessment of demand relative to supply;

- evidence is building that wages growth has peaked;

- the US economy is slowing significantly which will impact our the global economy and Australia;

- the monthly inflation data up to May is likely exaggerating the upside risks for June quarter CPI inflation; and

- headline inflation is set to fall below 3% in the September quarter as a result of energy rebates, which will lower inflation expectations, lower administered price increases and lower wage demands and make for difficult optics for the RBA in trying to explain a rate hike at a time when inflation numbers are set to fall sharply.

So, while we acknowledge that the risk of another hike is high and put the probability at 45%, our base case remains that rates have peaked ahead of rate cuts starting early next year. June quarter CPI data along with June retail sales and jobs data along with any early readings of how the tax cuts are impacting spending ahead of the August RBA meeting will be key.

Happy songs = happy share markets, or vice versa. A 2022 study in the Journal of Financial Economics “Music sentiment and stock returns around the world” found a positive correlation between share market returns and the positivity of songs people are listening to and a negative correlation to bond returns consistent with safe haven demand. Of course, correlation does not necessarily tell us much about causation – and it may just be that when people are happy they listen to happy songs and buy shares. But anyway, here are some upbeat songs - Love Affair’s “Everlasting Love” and Yaz and the Plastic Population’s “The Only Way Is Up”.

Major global economic events and implications

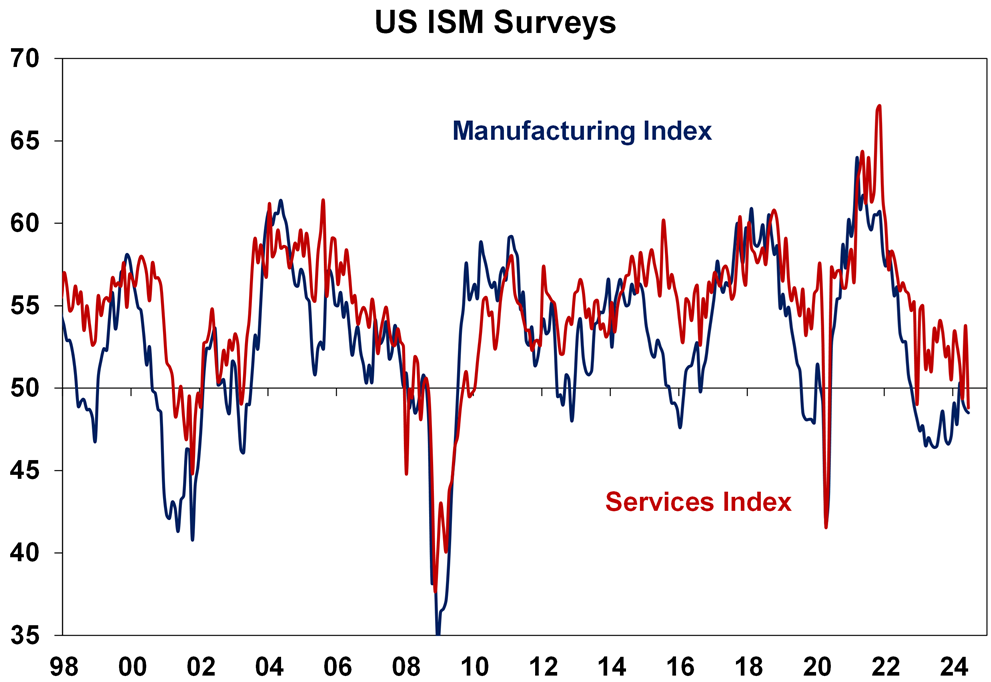

US economic data over the last week was soft. Both the manufacturing and services ISM indexes fell with both below 50. And both saw weak employment readings and falls in prices paid.

Source: Bloomberg, AMP

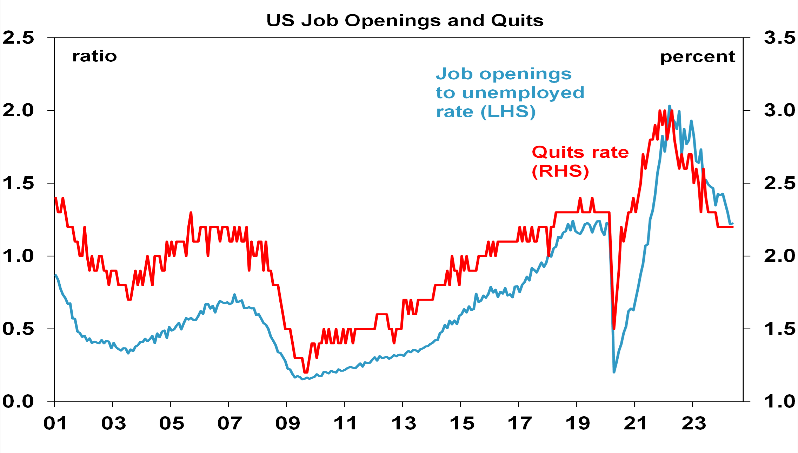

US job openings rose slightly in May and quits were unchanged but the trend in both remains down pointing to a weakening labour market. Similarly, the June ADP employment survey points to softer jobs growth (although it’s been an unreliable guide to payrolls) and initial and continuing jobless claims rose.

Source: Bloomberg, AMP

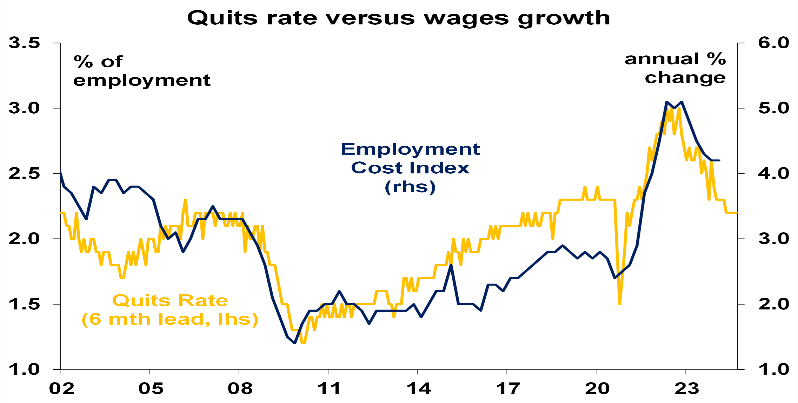

The fall in the US quits rate, ie less people quitting jobs for new jobs, points to a further slowing in wages growth ahead.

Source: Bloomberg, AMP

Eurozone inflation fell to 2.5%yoy in June from 2.6%, with core flat at 2.9%yoy. Unemployment was unchanged in May at 6.4%.

The Bank of Japan’s June quarter Tankan business survey showed mostly solid business conditions.

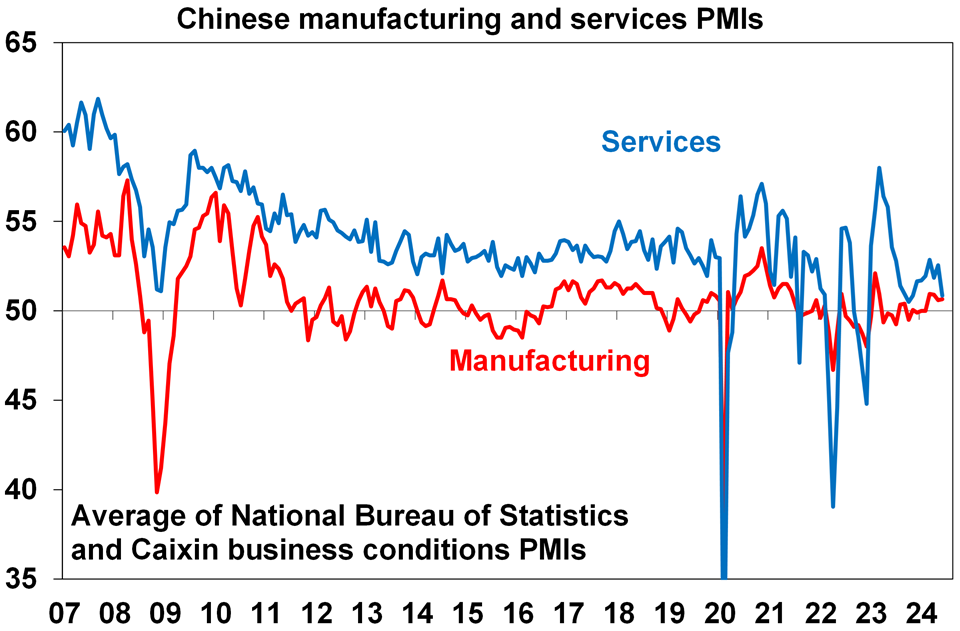

Chinese business conditions PMIs were on the soft side in June with the average of the official and Caixin PMIs showing a sharp weakening in services conditions and continued softness in manufacturing.

Source: Bloomberg, AMP

Australian economic events and implications

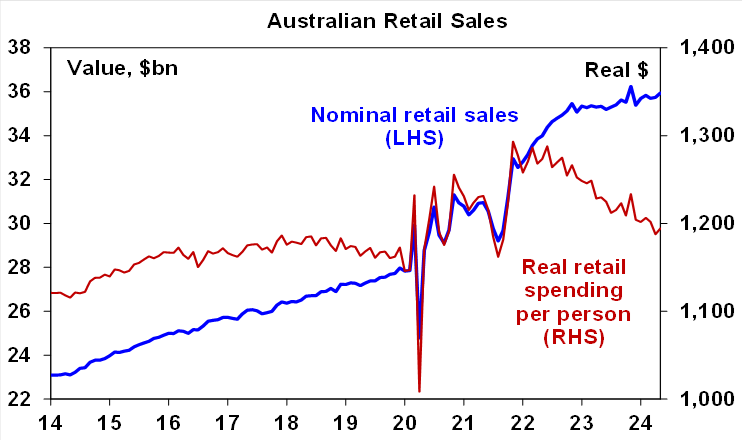

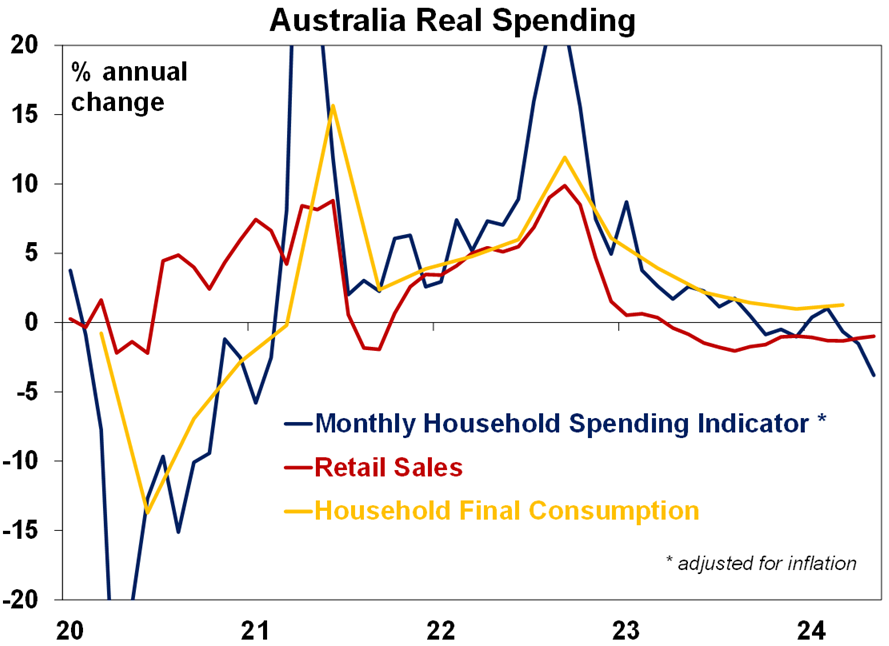

Australian economic data surprised on the upside a bit over the last week, but it’s not so good beneath the surface. After two weak months retail sales rose a stronger than expected 0.6% in June. However, it looks mostly due to cash strapped consumers taking advantage of early end of financial year sales and the trend remains weak with nominal retail sales inflated by price rises and the population surge. Real per person retail sales are down 7.5% or so from their record high leaving them almost back to their post Delta lockdown lows. Six months ago spending was boosted by sales in November with a fallback in December. June data which is due on 30 July ahead of the next RBA meeting may show something similar.

Source: ABS, AMP

The weakness in consumer spending was also highlighted by the ABS’ Monthly Household Spending Indicator covering both retail sales and wider services for May which slowed to just +0.1%yoy, led by a further slowing in both discretionary (-1.9%yoy) and non-discretionary spending (+1.8%yoy). With inflation around 4%yoy, this means a further leg down in already negative real spending growth.

Source: ABS, AMP

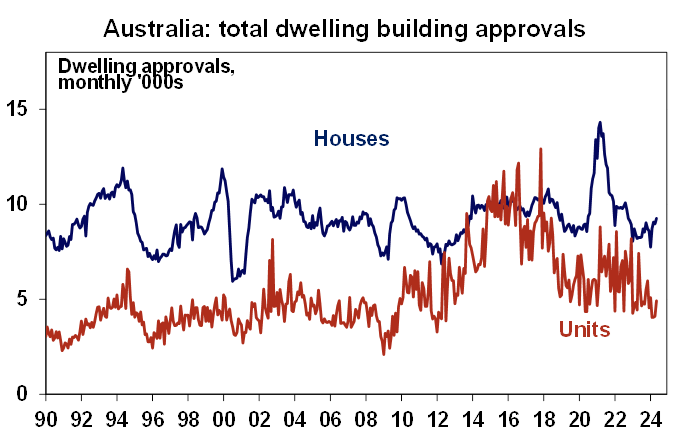

Home building approvals for May also bounced a more than expected 5.5%mom, but this followed several weak months, was mainly due to a 19.7%mom bounce in normally volatile unit approvals and much of the rise in house approvals was just due to WA. Normally lower interest rates are required for a sustained upswing and they are still a way off. Meanwhile, approvals are running around an annual pace of 161,000 pa which is way below current underlying demand for around 250,000 dwellings a year and well below the objective of Australian governments under the Housing Accord to build 240,000 homes pa over the next five years, starting now.

Source: ABS, AMP

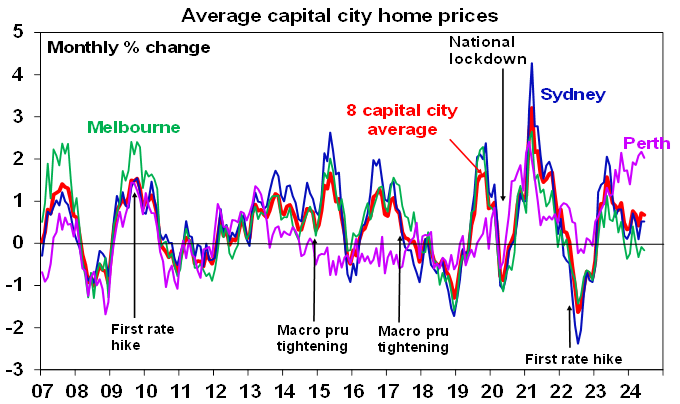

CoreLogic home price data showed another lift in national average home prices of 0.7% in June, resulting in an average price growth of 8% through the last financial year. The housing shortage continues to dominate the drag from high mortgage rates. However, there remains a huge divergence between cities with Perth, Brisbane and Adelaide booming but Hobart and Melbourne weak. The housing shortage continues to point up for home prices, but the delay in rate cuts and talk of rate hikes risks renewed falls in property prices as its likely to cause buyers to hold back and distressed listings to rise. The weakness in Melbourne despite Victoria having the second strongest population growth in Australia across states and territories warns that the housing shortfall is no guarantee that prices will continue to rise when mortgage rates remain high.

Source: CoreLogic, AMP

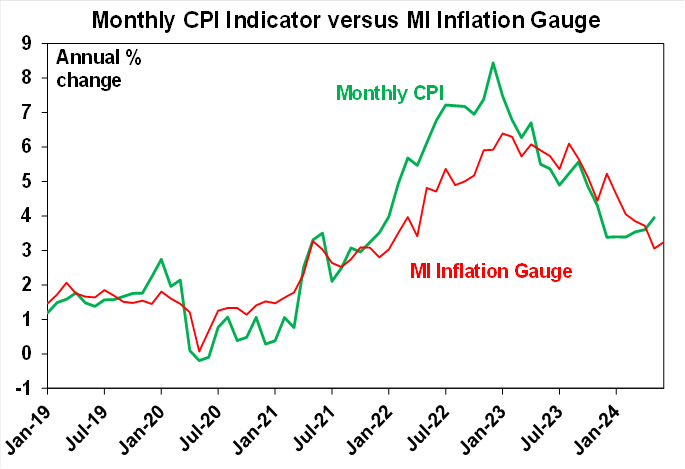

The Melbourne Institute’s monthly Inflation Gauge for June continues to point to a resumption of falling CPI inflation.

Source: Melbourne Institute, AMP

The rate of wages growth in new Enterprise Bargaining Agreements appears to have peaked supporting the view that overall wages growth has likely peaked too.

Source: Fair Work Commission, AMP

Finally, the trade surplus remained around the $6bn level in May, well down from its peak of nearly $20bn in 2022, with imports up a bit more than exports.

What to watch over the next week?

In the US, the focus will be back on inflation with the June CPI (Thursday) expected to show a fall to 3.1%yoy from 3.3% and core inflation unchanged at 3.4%yoy. Producer price inflation (Friday) is also expected to show a slowing in the annual rate. And small business optimism (Tuesday) is likely to remain weak. The US June quarter reporting season will start to get underway. Consensus expectations are for a 7.8%yoy rise in earnings, which is likely to end up being around 10%yoy again. Excluding tech, the consensus expectations are for 2.5%yoy growth.

In Europe, the focus will be on the results from the final round of the French parliamentary elections on Sunday. Investors are likely assuming that National Rally wins the most number of seats but not enough to form government resulting in a hung parliament – which would not be great but would be less disruptive and less threatening of another Eurozone crisis than seeing a National Rally government. NR being able to form government though would be taken badly by markets resulting in a further leg down in French shares and a blow out in bond yield spreads to Germany.

The Reserve Bank of New Zealand (Wednesday) is expected to leave its cash rate on hold at 5.5%.

Chinese inflation for June (Wednesday) is expected to remain weak but edge up slightly to 0.4%yoy (from 0.3%) with producer price inflation at -0.8%yoy (up from -1.4%). Trade data (Friday) is expected to show a slight improvement in export and import growth.

In Australia, housing finance data for May (Monday) is expected to show a 2% gain. The Westpac/Melbourne Institute’s consumer sentiment index for July (Tuesday) is likely to remain weak and could fall again following increased talk of another rate hike although this may be partly offset by high media coverage around the tax cuts. The June NAB business survey will also be released Tuesday.

Outlook for investment markets

Easing inflation pressures, central banks moving to cut rates and prospects for stronger growth in 2025-26 should make for reasonable investment returns over 2024-25. However, with a high risk of recession, possible delays to rate cuts and significant geopolitical risks, the next 12 months are likely to be more constrained and rougher compared to 2023-24.

We expect the ASX 200 to return 9% this calendar year and end the year around 7900. A recession is probably the main threat.

Bonds are likely to provide returns around running yield or a bit more, as inflation slows, and central banks cut rates.

Unlisted commercial property returns are likely to remain negative due to the lagged impact of high bond yields and working from home.

Australian home prices are likely to see more constrained gains over the next 12 months as the supply shortfall remains, but still high interest rates constrain demand and unemployment rises. The delay in rate cuts and talk of rate hikes risks renewed falls in property prices as its likely to cause buyers to hold back and distressed listings to rise.

Cash and bank deposits are expected to provide returns of over 4%, reflecting the back up in interest rates.

A rising trend in the $A is likely taking it to $US0.70 over the next 12 months, due to a fall in the overvalued $US and a narrowing in the interest rate differential between the Fed and the RBA.

Financial year end performance update - July 2024

04 July 2024 | Blog Hear from Stuart Eliot, Head of Portfolio, Stephen Flegg, Senior Portfolio Manager and My Bui, Economist at AMP Investments as they will provide an overview of the financial year end performance for June 2024, and discuss the key drivers and trends in the economy. Read more

Oliver's insights - strong investment returns

02 July 2024 | Blog There has been a wall of worry for investors over the last year but as is often the case share markets climbed it. This resulted in another financial year of strong investment returns in 2023-24. But can it continue? Read more

Weekly market update 28-06-2024

28 June 2024 | Blog Dr Shane Oliver observes strong financial year returns - but can it continue?; Trump odds up after debate - watch trade war risks; risk of another RBA hike up but not fait accompli; Australian jobs market cooling; another big Australian budget surplus and more. Read moreWhat you need to know

While every care has been taken in the preparation of this article, neither National Mutual Funds Management Ltd (ABN 32 006 787 720, AFSL 234652) (NMFM), AMP Limited ABN 49 079 354 519 nor any other member of the AMP Group (AMP) makes any representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided and must not be provided to any other person or entity without the express written consent AMP. This article is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives and does not constitute a recommendation, offer, solicitation or invitation to invest.

The information on this page was current on the date the page was published. For up-to-date information, we refer you to the relevant product disclosure statement, target market determination and product updates available at amp.com.au.