Key points

- The US election has significant potential to impact markets. A Harris victory would mean more of the same, but a Trump victory could lead to uncertainty particularly around trade.

- Australia would be vulnerable to a rapid intensification of trade wars which is looking likely under a Trump presidency.

- Historically, shares have performed better under Democrat than Republican presidents with the best outcome being a Democrat president and Republican House and/or Senate.

Introduction

The US election is less than a month away. So far investment markets seem to be paying little attention to it. However, this could change as Donald Trump’s policies are very different to Kamala Harris’ with significant implications for the global economy and Australia. A Trump victory could lead to a weakening in US institutions, democracy and global alliances and a narrow Trump loss could see political unrest. Being unable to run for a third term, a second Trump presidency will lack the electoral constraints of his first term and is likely to have less “adults in the room”.

The resilient economy and shares favour Harris

Strong economic and financial conditions tend to point to a Harris victory.

- The US economy remains strong, avoiding so far the much feared recession. Even if one arrives this quarter (which looks unlikely) it will arguably be too late to impact the election in a month.

- The so-called Misery Index (unemployment + inflation) has been falling and is down on a year ago, which historically points to a victory for the incumbent party (Democrats). According to research house Strategas, it has correctly predicted 15 of the past 16 election results since 1980.

- US shares are strong – if they are up over the 3 months prior to the election the incumbent party tends to win & vice versa. This has been 83% accurate since 1928. Right now, it’s up 10.9% since 5th August.

Of course, none of these are infallible. US shares rose 2.3% over the three months prior to the 2020 election and yet Trump lost (although there was a recession that year) and the incumbent party (with Hilary Clinton) lost in 2016 despite the absence of recession. And in this election, the cost-of-living surge and immigration blow out under the Biden Administration is an ongoing drag for Harris even though the rate of inflation has fallen and several key battleground states (which will likely determine the election under the US electoral college system) have seen economic conditions weaken lately – notably Michigan, Nevada, Wisconsin and Georgia.

But polling is very close

The replacement of Biden with Harris saw a spike in Democrat prospects, but this has faded and the election looks very close.

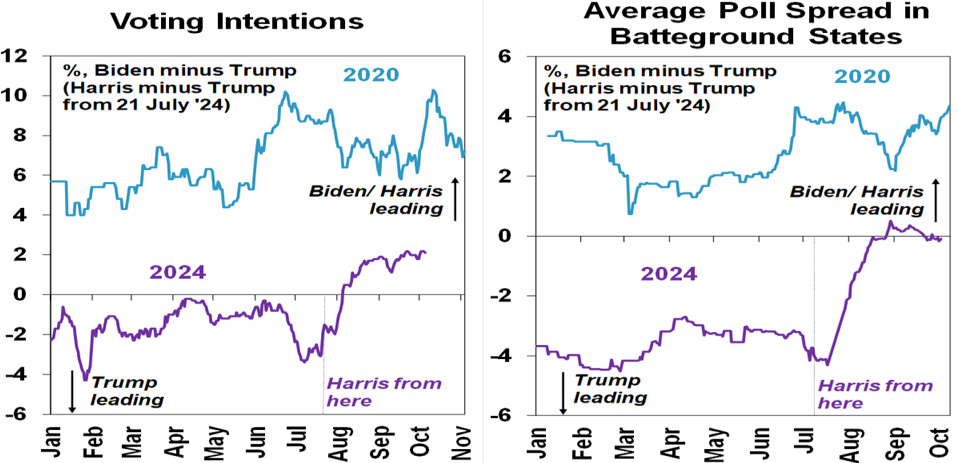

- Real Clear Politics poll average has Harris leading Trump by 2 points in terms of presidential voting intentions, but this is well behind where Biden was at the same point in 2020. See next chart at left.

- And the RCP poll average of battleground states has Harris lagging Trump by 0.2 points with Harris ahead in 3 and Trump ahead in 4. This is well down from Biden’s lead in 2020. See next chart at right.

Source: Real Clear Politics, Bloomberg, AMP

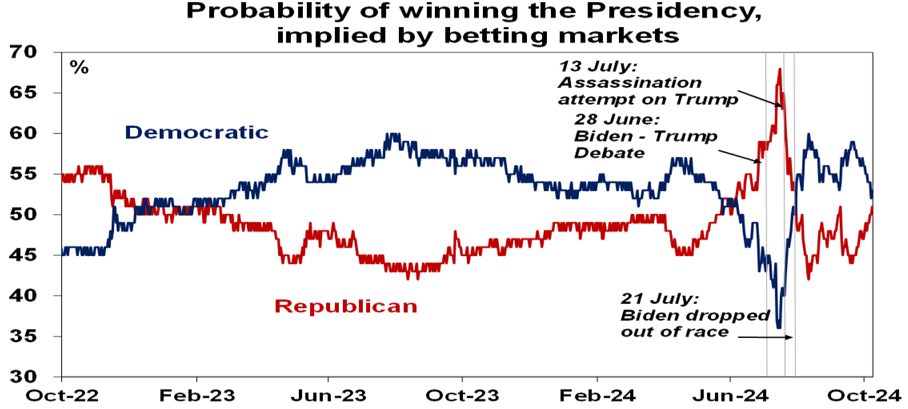

- The ‘PredictIt’ betting market has the Democrats only just ahead, with the Democrats down from a boost from the Harris/Trump debate & the RCP average of betting markets has Trump ahead.

Source: PredictIt, AMP

- If Trump wins, it’s likely the Republicans would regain control of the Senate (where they have an edge as the Democrats need to defend more seats) and possibly keep the House, resulting in a clean sweep.

- If Harris wins, it’s likely the Democrats retain the House, but lose the Senate (having to defend more seats), resulting in divided government.

Key Trump policy differences versus Harris

Taxation: Trump would make the 2017 personal tax cuts (which took the top marginal tax rate to 37%) permanent (as they expire in 2025) and cut the corporate tax rate to 20% with 15% for domestic manufacturing. Harris would extend the expiring 2017 tax cuts for those earning under $400,000, provide bigger tax credits for caring, raise the corporate tax rate to 28%, raise the capital gains tax rate to 28% for those earning more than $1m and tax unrealised capital gains. Note that the corporate and capital gains tax increases will be very hard to legislate as Biden found.

Trade: Harris would basically continue current policies which have kept Trump’s first term tariffs, added some and focussed on subsidies for green manufacturing in America. Trump is threatening a much bigger ramp up in protectionism though with a 10-20% tariff on all imports and a 50-60% tariff on imports from China. This would take the average US tariff rate from around 2.5% to around 17%, a level last seen in the 1930s. In practice, Trump is likely to target countries with a trade surplus with the US (notably China, Europe and Japan), the tariffs may not get as high and it may be part of a “maximum pressure” campaign to bring production, including by Chinese manufacturers, back to the US (as occurred with Japan in the 1980s). The latter may be the case, but we could go through a lot of disruption as Trump initially ramps up the pressure resulting in a much bigger impact on share markets than seen in 2018 (where Trump’s trade wars contributed to an almost 20% fall in shares). This will likely be made worse as impacted countries respond with tariffs on US imports in retaliation. The impact will be an acceleration in the process of deglobalisation. Trump’s inability to have a 3rd term may see him act earlier on trade and more aggressively than was the case in his first term as he will be less constrained by political considerations.

Immigration: Immigration surged under Biden making it a big issue but has been limited lately with Harris likely to continue this. Trump will aggressively curtail immigration threatening mass deportation.

Cost of living: Harris is proposing a ban on grocery price gouging, support for home buyers and drug price caps

Fed independence: Trump would seek to replace Jerome Powell, and his supporters are looking at ways to roll back the Fed’s independence.

Climate policy: Trump will likely reverse the US’ net zero commitments and the policies Biden introduced to support it and support fossil fuels (“drill baby drill”). Subsidies for green manufacturing are likely to be replaced with wider support for domestic manufacturing (eg, a 15% corp tax rate).

Regulation: Trump is likely to slash energy and financial regulation.

Budget deficit: The deficit – already huge at 6% of GDP - would likely get bigger under Trump (+2-3% of GDP) than under Harris (+1-2% of GDP).

Economic impact of a Trump victory

A Harris victory would mean a continuation of the status quo – unless she raises the corporate and capital gains tax rates. Raising these tax rates is unlikely though unless Democrats win both the House and Senate, but even then, it’s difficult to get through as Biden found. Trump would be far from the status quo though.

His policies in support of tax cuts and deregulation could help boost the supply side of the US economy via a boost to productivity (which is already good). However, on balance Trump’s policies – with higher tariffs resulting in higher import prices, lower labour force growth and potential moves to weaken the Fed’s credibility – risk adding to inflation.

There is also a risk that an even higher budget deficit, with no sign of improvement when US public debt is already very high (at 125% of GDP), will result in a market backlash (like Liz Truss saw) and higher bond yields. Furthermore, his brinkmanship and erratic policy making style is likely to add to policy uncertainty which could hamper business investment.

Much will depend on sequencing. If he runs with tax cuts and deregulation first (as in 2017) it could boost shares and the economy in say 2025, but if he runs first with sharp tariff hikes and immigration cuts it could be taken more negatively early on. In 2017 he ran with the positives first to help boost the economy, but this time around he may run with negatives first as there will be no constraint from the desire to win another election.

Finally, a Trump victory could add to geopolitical uncertainty by weakening US institutions and democracy and weakening US alliances. It could also lead to a quicker end to the Ukraine war, but with loss of territory.

Likely investment market implications

Firstly, despite the heightened policy uncertainty the election year is normally okay for US shares. Since 1927, the election year, or year 4 in the presidential cycle, has had an average return of 12%, which is also the average across all years. So far, they have returned 22%. It’s usually years 1 and 2 which are below average.

Second, the next few weeks could see increased volatility if investors start to focus on the risks of a new trade war, a hit to the US labour force and increased uncertainty under Trump. After Trump’s victory in 2016 shares soared 38% to January 2018 as the focus in his first year was on business-friendly tax cuts and deregulation but they fell in 2018 as the focus shifted to trade wars. So, Trump wins, the market reaction in the first 6-12 months will be heavily influenced by the sequencing of tariff hikes versus tax cuts.

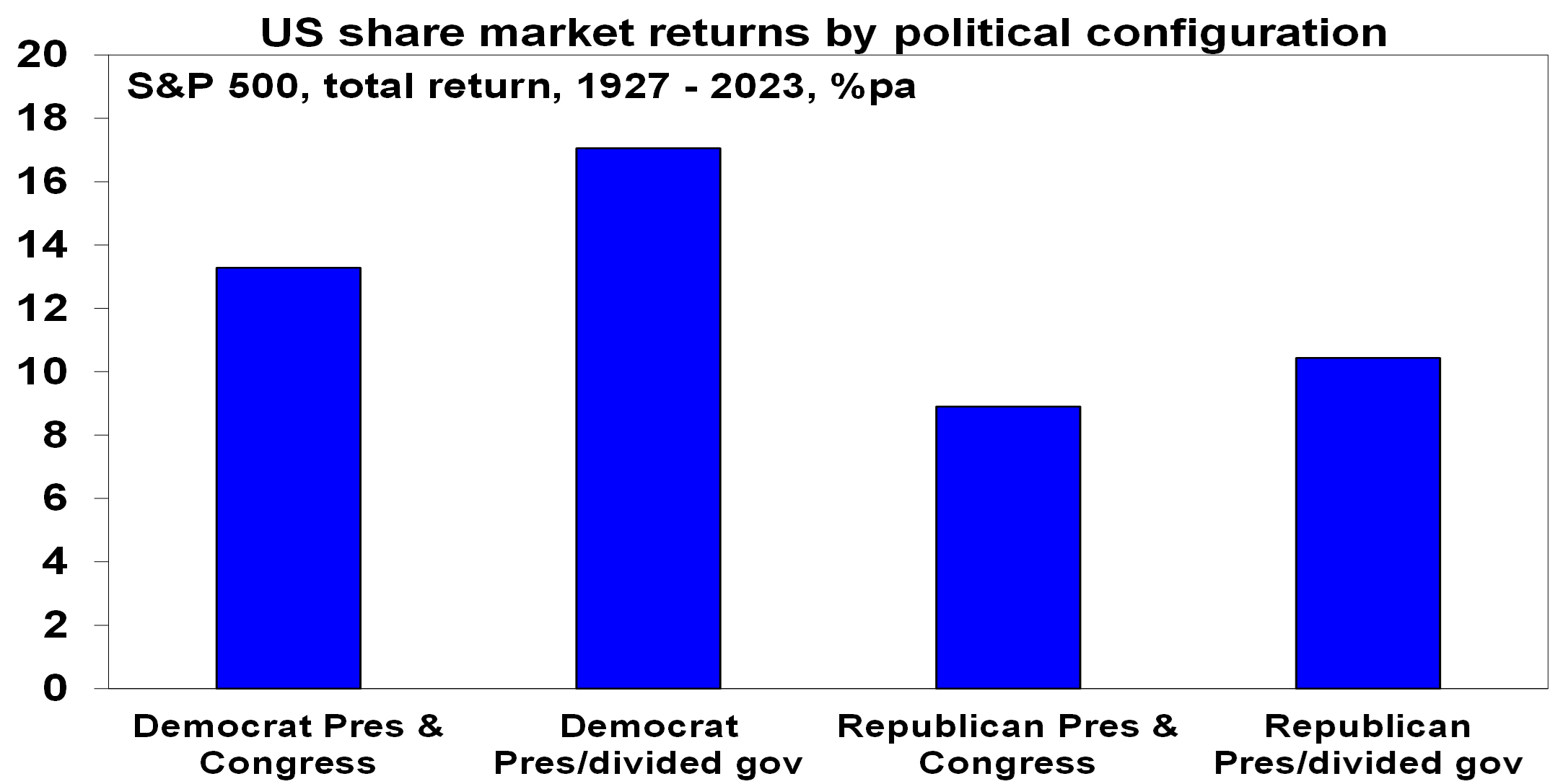

Third, historically US shares have done best under Democrat presidents with an average return of 14.4% pa since 1927 compared to an average return under Republican presidents of 10% pa. However, the best average result has actually occurred when there has been a Democrat president and Republican control of the House, the Senate or both and the worst average return has been when there’s been a clean Republican sweep.

Source: Bloomberg, AMP

Fourth, a Trump presidency would likely mean higher bond yields (with slightly higher inflation, budget deficits and US policy uncertainty) and a higher $US (with higher global uncertainty and the impact of US tariffs).

Finally, a narrow Trump loss would likely see him challenge the result which could lead to political uncertainty adding to market volatility. Although US democratic institutions should hold as they did back in 2020.

Australia is vulnerable to a new Trump trade war

Exports to the US are only 4% of Australia’s total exports and may be spared from Trump’s tariffs as Australia has a trade deficit with the US. However, as an open economy with high trade exposure to China, Australia would be vulnerable to an intensification of global trade wars as a result of a Trump victory, particularly if it weighs on demand for Chinese exports. An OECD study showed that Australia could suffer a 1.2% reduction in GDP as a result of a 10% reduction in global trade between major countries. Resources shares would be most at risk and the $A would likely fall. Of course, similar fears existed during the last Trump trade war, and it didn’t turn out so bad. And there would still be demand for iron ore somewhere – it just may switch from China to the US and elsewhere. Much would depend on how other countries respond and how hard Trump goes. Of course, he may not win!

Oliver's insights - Trump challenges and constraints

19 November 2024 | Blog Why investors should expect a somewhat rougher ride, but it may not be as bad as feared with Donald Trump's US election victory. Read more

Econosights - strong employment against weak GDP growth

18 November 2024 | Blog The persistent strength in the Australian labour market has occurred against a backdrop of poor GDP growth, which is unusual. We go through this issue in this edition of Econosights. Read more

Weekly market update 15-11-2024

15 November 2024 | Blog Global share markets were messy over the last week, not helped by the ongoing rise in bond yields and a wind back in Fed rate cut expectations after some elevated US inflation data and slightly hawkish comments from Fed chair Powell. Read moreWhat you need to know

While every care has been taken in the preparation of this article, neither National Mutual Funds Management Ltd (ABN 32 006 787 720, AFSL 234652) (NMFM), AMP Limited ABN 49 079 354 519 nor any other member of the AMP Group (AMP) makes any representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided and must not be provided to any other person or entity without the express written consent AMP. This article is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives and does not constitute a recommendation, offer, solicitation or invitation to invest.

The information on this page was current on the date the page was published. For up-to-date information, we refer you to the relevant product disclosure statement, target market determination and product updates available at amp.com.au.