Key points

- Global growth has picked up in early 2024, and is broadening out, after being dominated by the US last year.

- Better global growth is lifting commodity prices, along with other factors like heightened geopolitical concerns and central bank demand for commodities like gold.

- Higher raw materials prices are an upside risk to inflation. If inflation starts rising again, central banks will be forced to delay cutting interest rates or even start hiking again which would be negative for sharemarkets.

- But the current rise in commodity prices has occurred predominantly in metals, which don’t always flow through to inflation. After reaching record highs in recent weeks, gold and copper prices have fallen.

- We expect that most major central banks will be cutting interest rates by the end of the year as inflation slows and economic growth is low.

Introduction

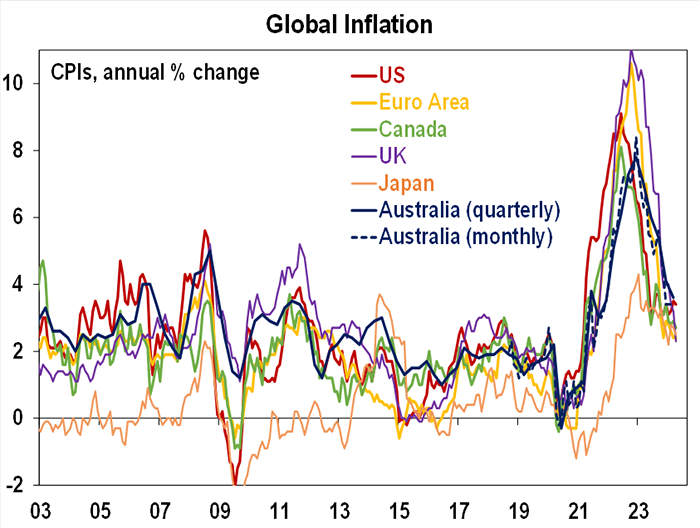

The release of global PMI indicators recently indicated that global growth is ticking up and broadening out around the world, after being dominated by the US in 2023. Stronger global growth (as well as other factors like geopolitical concerns) are lifting commodity prices, which is causing renewed concern about the inflation outlook and leading to financial markets pushing back expectations for rate cuts. Global headline inflation has fallen significantly from its 2022 highs (see the chart below) and is running between 2.5%-3.5% across major economies. But, core inflation is still too high, and has been slower to decline. In this Econosights we look at the impact of stronger global growth on the trajectory for inflation.

Source: Bloomberg, AMP

Global growth and commodity prices

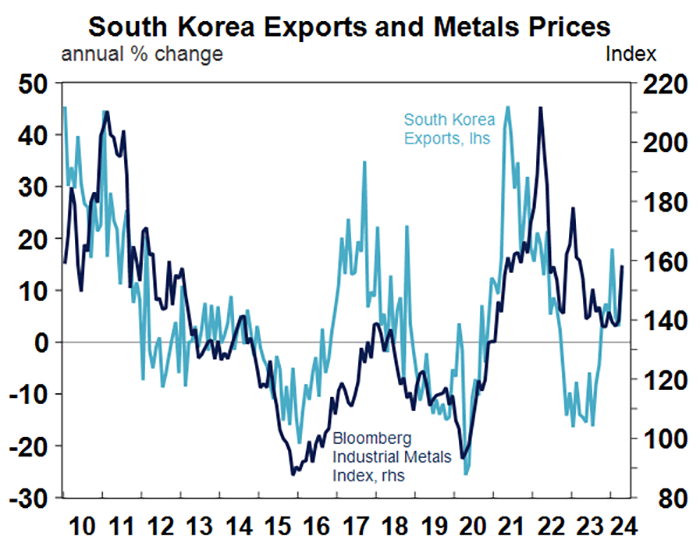

The tick-up in global growth is one explanation for the increase in commodity prices, through the associated lift in demand, particularly for heavy industries. South Korean exports are often considered a bellwether for global growth (because of the high share of semiconductors, chips and motor vehicles and accessories) and have been increasing in early 2024. This has occurred alongside a pickup in industrial metals prices (see next chart).

Source: Macrobond, AMP

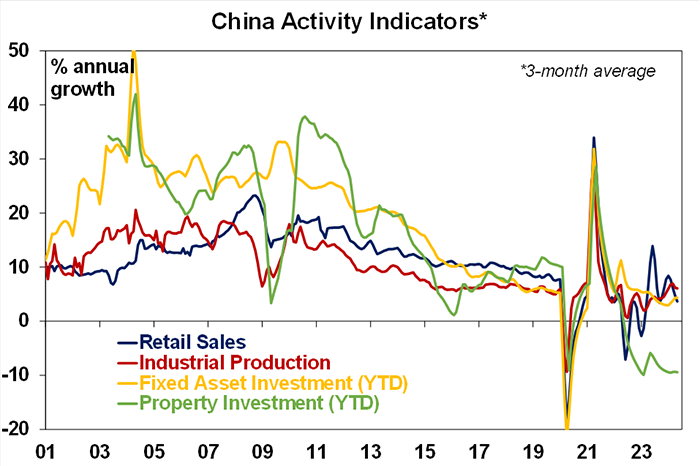

Despite a lot of negative headlines and concerns around Chinese GDP growth (particularly with regards to the property sector), industrial production has held up in China (see the chart below), and industrial metals demand from China accounts for around 40-60% of global industrial metals demand. This reflects the strong growth in areas like solar panels, electric cars, airplanes and infrastructure construction.

Source: Bloomberg, AMP

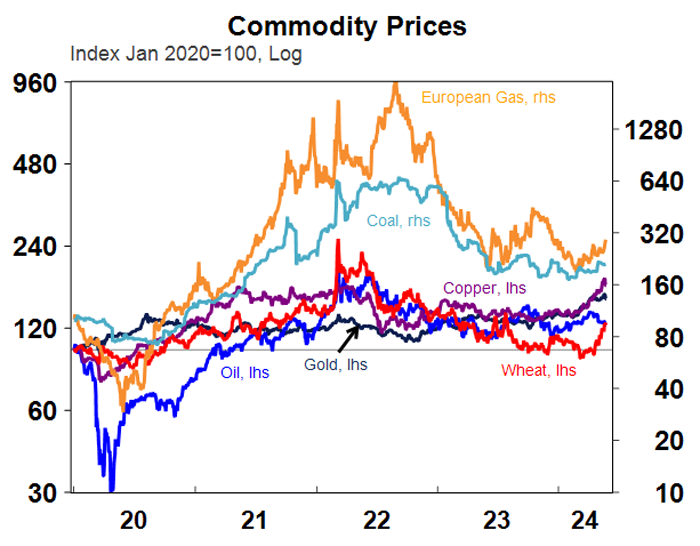

The lift in metals prices has occurred in copper (around a record high), gold (around a record high), aluminium, nickel and silver. But, other commodity markets have also seen a lift, including gas, corn and wheat (due to poorer Russian crop prospects). Oil prices are around $80USD/barrel, down from their highs of ~$90USD/barrel in early April.

Source: Macrobond, AMP

Other explanations for the rise in commodity price include a heightened geopolitical climate (with increasing threats in the Middle East) which usually lifts gold prices (typically seen as a safe haven), central banks buying gold or selling out of US treasuries and purchasing gold and expectations for lower interest rates through this year which decreases the opportunity cost of holding gold and also boosts growth prospects in the future.

Commodity prices and inflation

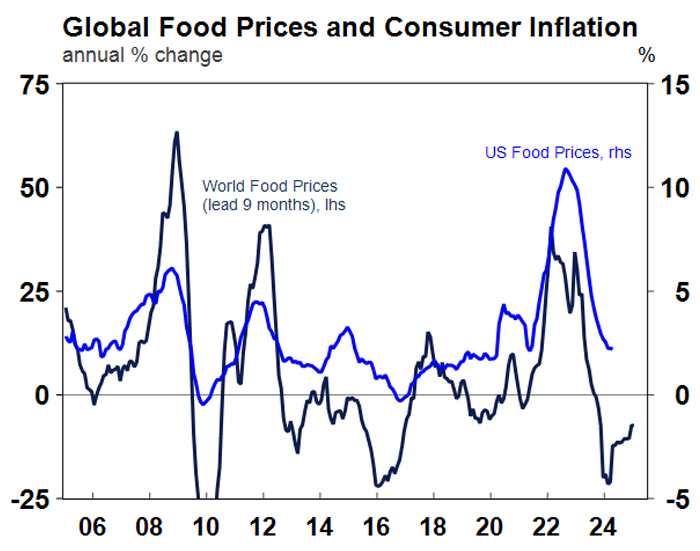

The broad fall across commodity prices in 2023 led to lower goods prices and helped to reduce inflation. So, if the recent tick up in commodity prices is sustained, it is an upside risk for inflation, as raw materials are used in production for many items, especially food. US food inflation has remained elevated (see the chart below) despite a steep fall in world food prices (although the chart below indicates that food prices should fall further).

Source: Macrobond, AMP

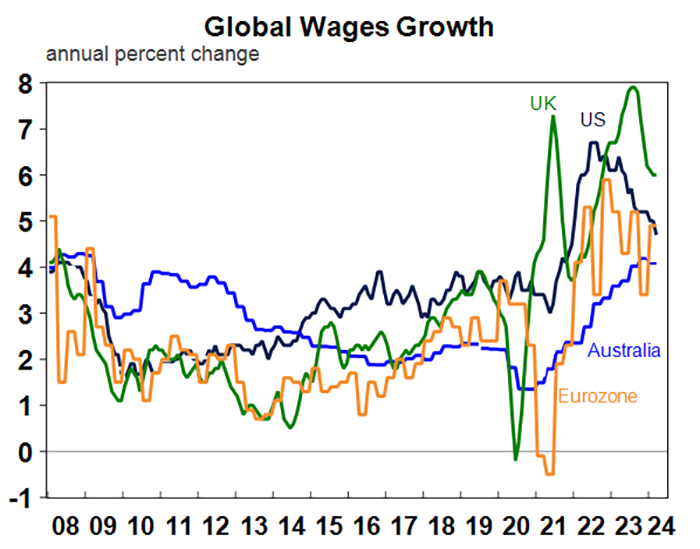

However, the current economic backdrop is quite different to 2022. Across major economies like the US and Australia, multiple rate hikes have weakened the consumer. This is particularly evident in Australia with the faster cash flow transmission from the interest rate set by the central bank to the outstanding mortgage rate paid by households, with consumers drawing down on their accumulated savings. As a result, even if producer prices rise due to higher raw materials, they may not be able to pass on these prices as easily to consumers. As well, wages growth is slowing around the world (see the next chart) and should offset any potential rise in inflation as a result of higher commodity prices. Lower wages growth is needed to reduce services inflation. Although, wages growth still needs to decline further to be back to around 3-3.5%, to be closer in line to central bank inflation targets.

Source: Macrobond, AMP

Implications for investors

We have been expecting inflation to decline further in 2024. The lift in commodity prices is an upside risk to our inflation projections but it’s too soon to be certain that higher raw materials prices will be sustained or passed on to consumers. Global growth improved in early 2024, but the US economy is weakening, China still faces many issues in its property sector and many advanced economies are being negatively impacted by high interest rates. So, the stronger growth backdrop since the start of the year probably doesn’t have much further to rise. We see the current macroeconomic environment as being quite different to 2021/22. In the immediate post-COVID period, producers were able to pass on higher raw materials prices to consumers because consumer demand was strong. But now, growth is softer and consumers are in a weaker position after numerous rate hikes and the draw-down on their accumulated savings. As a result, we expect that there is further downside to inflation and we expect most major central banks to be cutting interest rates by the end of the year. But, the slow progress on reducing services inflation means that any rate cuts will be minimal and central banks will be slow to unwind prior interest rate increases (unless there is a growth downturn or a recession!).

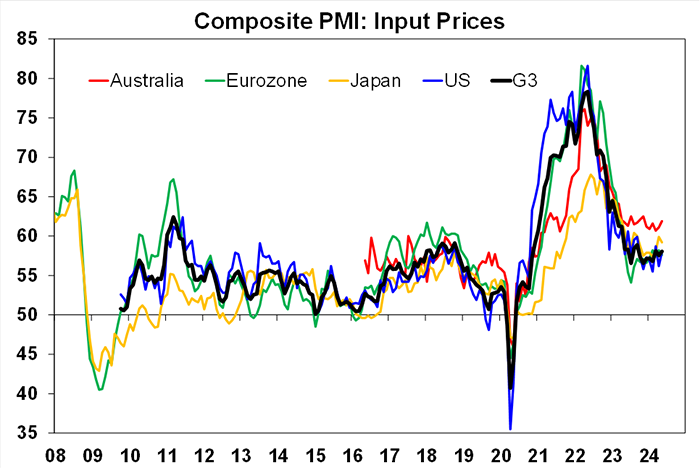

Something for investors to watch are the price indicators in the PMI surveys which are a good leading indicator for inflation. Input prices have mostly been stable in recent months, but it would be good to see some further downside from here.

Source: Bloomberg, AMP

Weekly market update 28-06-2024

28 June 2024 | Blog Dr Shane Oliver observes strong financial year returns - but can it continue?; Trump odds up after debate - watch trade war risks; risk of another RBA hike up but not fait accompli; Australian jobs market cooling; another big Australian budget surplus and more. Read more

Oliver's insights - investing 40 years

25 June 2024 | Blog Dr Shane Oliver shaes his nine most important lessons from investing over the past 40 years. Read more

Weekly market update 21-06-2024

21 June 2024 | Blog This week, narrowing US share gains; drip feed of falling global inflation & rates is good sign for RBA; Federal & state governments making the RBA's job harder; the pros & cons of nuclear; and more. Read moreWhat you need to know

While every care has been taken in the preparation of this article, neither National Mutual Funds Management Ltd (ABN 32 006 787 720, AFSL 234652) (NMFM), AMP Limited ABN 49 079 354 519 nor any other member of the AMP Group (AMP) makes any representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided and must not be provided to any other person or entity without the express written consent AMP. This article is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives and does not constitute a recommendation, offer, solicitation or invitation to invest.

The information on this page was current on the date the page was published. For up-to-date information, we refer you to the relevant product disclosure statement, target market determination and product updates available at amp.com.au.