Key points

- Post pandemic, the supply of labour has increased in many major economies, including the US and Australia, through elevated immigration and a lift in the participation rate to a record high.

- This positive supply shock is helpful in allowing economic growth to remain positive (rather than decline significantly) but at the same time put downward pressure on inflation.

- In this environment, employment growth is likely to remain positive, from the simple fact that the inflow of workers into the labour force is elevated. But this doesn’t mean that wages growth (and therefore inflation) will keep rising.

- A better guide to wages growth is to focus on labour market tightness, by looking at whether labour demand is exceeding labour supply (which is a sign of a tight labour market).

- Central banks are paying more attention to these supply shocks in assessing their outlook for inflation.

Introduction

Inflation has declined across the major advanced economies from its 2022 highs (despite hitting a speed bump in the first quarter of this year) and economic growth has mostly been positive and in the case of the US has been exceptionally strong. The unemployment rate has also remained lower than expected across the major economies. More economic pain was expected throughout 2023 and 2024 after the major global central banks raised interest rates significantly. One explanation for this situation is the increase in the supply side of the economy.

The basics of supply and demand

Economics 101 is all about the movement of demand and supply in an economy. If there is an increase in demand, the demand curve shifts outwards, increasing the quantity of items demanded (demand moves from Demand 1 in the next chart to Demand 2) which leads to an increase in prices (from P1 to P2). This movement in demand reflects the experience of major advanced economies after the pandemic thanks to large monetary and fiscal stimulus (we didn’t include the impacts of the supply shortages during the pandemic but it’s important to note this also contributed to higher prices).

Source: AMP

Tracking demand is quite straightforward through the many basic economic growth indicators.

However, changes in supply are also important, although they tend to be slower moving and harder to measure than demand. When supply increases (from Supply 1 to Supply 2 in the chart below), the quantity of goods produced increases (the quantity moves from Q1 to Q2), which puts downward pressure on prices. This situation seems to explain the current environment that has seen a slowing in inflation since its 2022 high. There are two main inputs that determine supply in an economy which are labour and capital (which refers to things that are used in production like buildings, machinery and equipment or intangibles like research and development).

Source: AMP

Labour supply

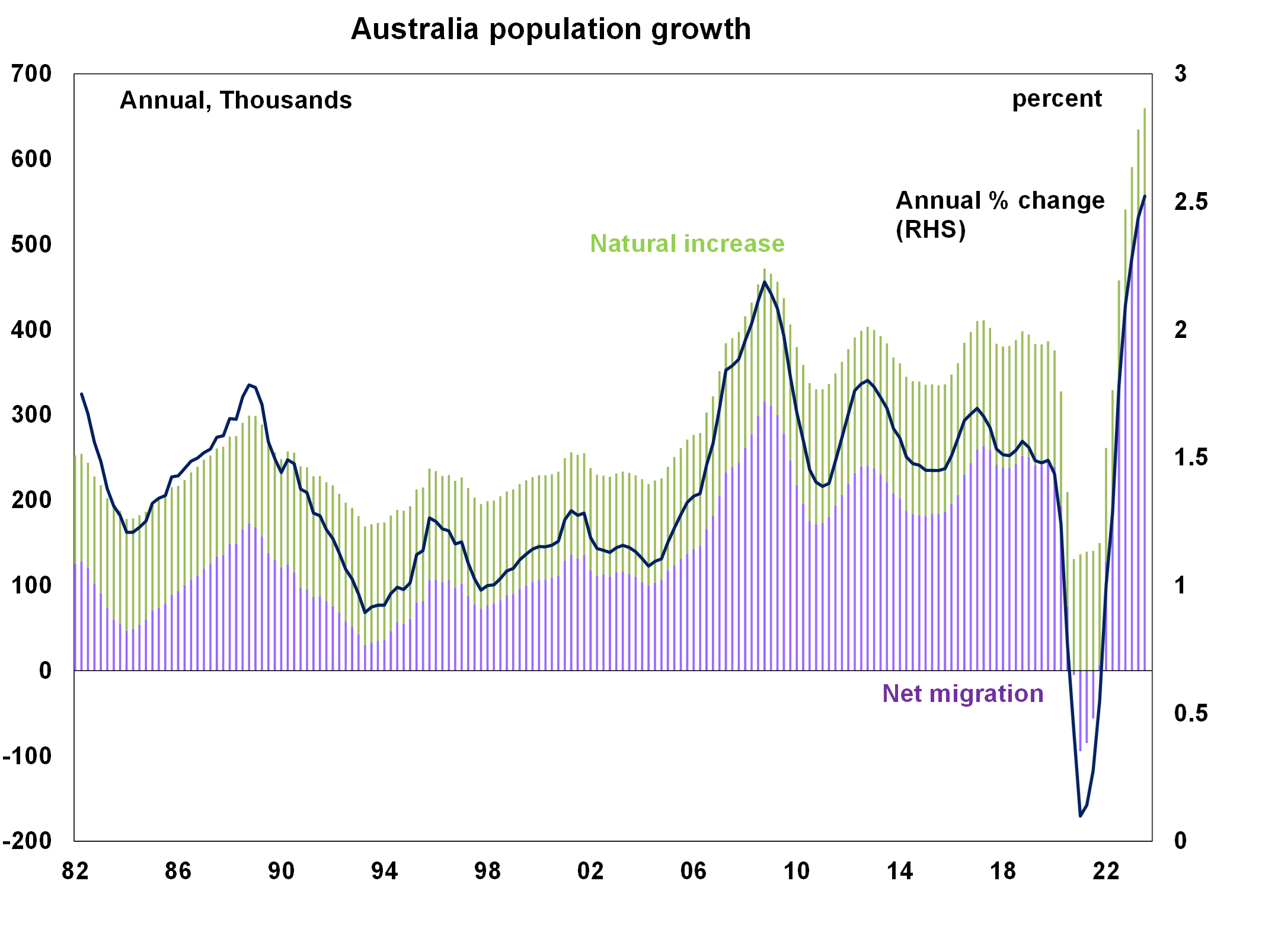

The easiest way to see the lift in supply has been in the labour force. In Australia, the reopening after the pandemic resulted in a massive lift in immigration. Prior to the pandemic, Australia had elevated population growth of 1.6% which was above the OECD average of ~0.6%. Since then, population growth has surged to 2.5% per annum, its highest annual rate since post World War II. More than 80% of the recent lift in population is thanks to immigration (see the next chart).

Source: ABS, AMP

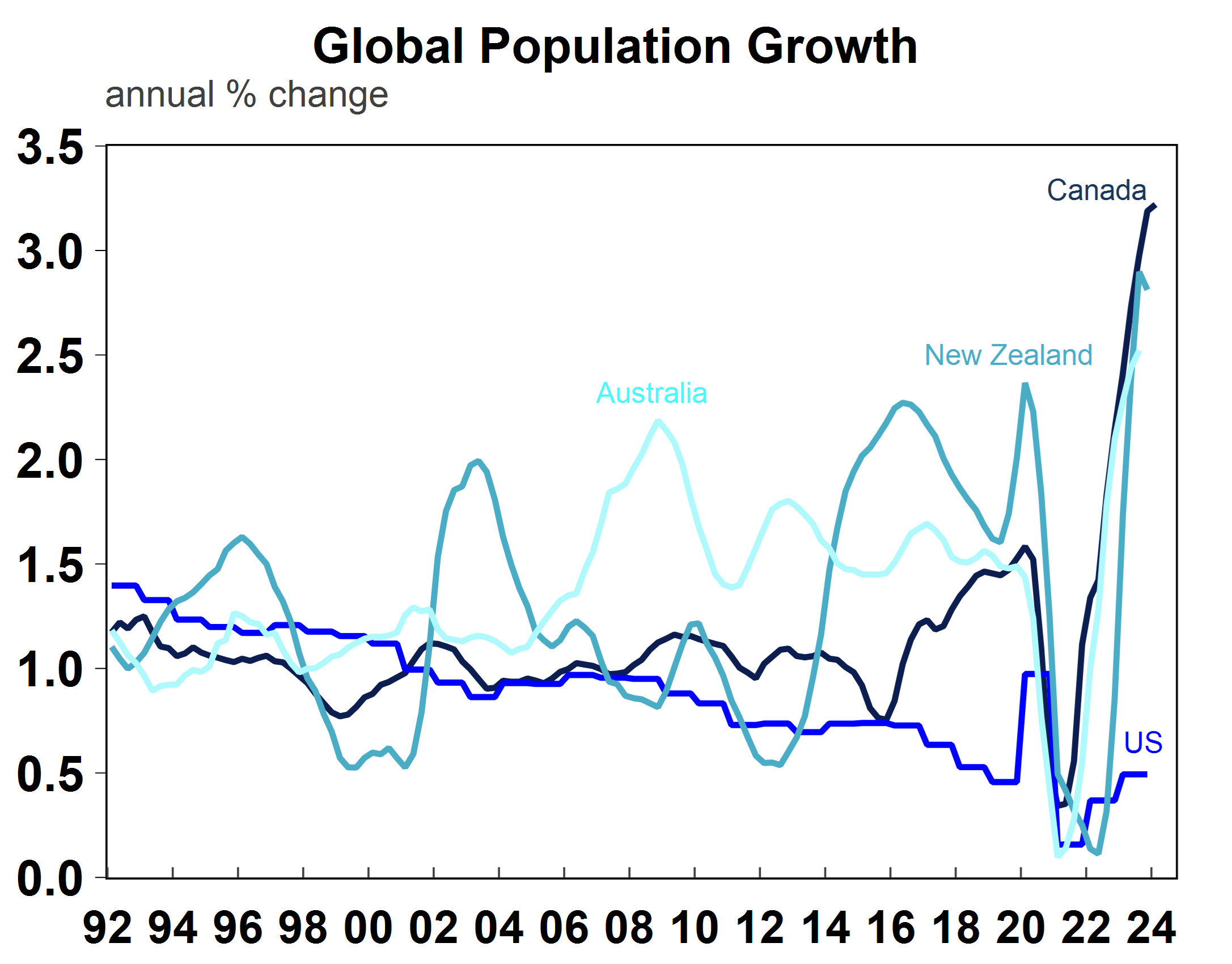

Australia’s experience has been in line with other economies like New Zealand and Canada who have all seen a big lift in population growth (see the chart below) as a post-COVID normalisation in immigration.

Source: Macrobond, AMP

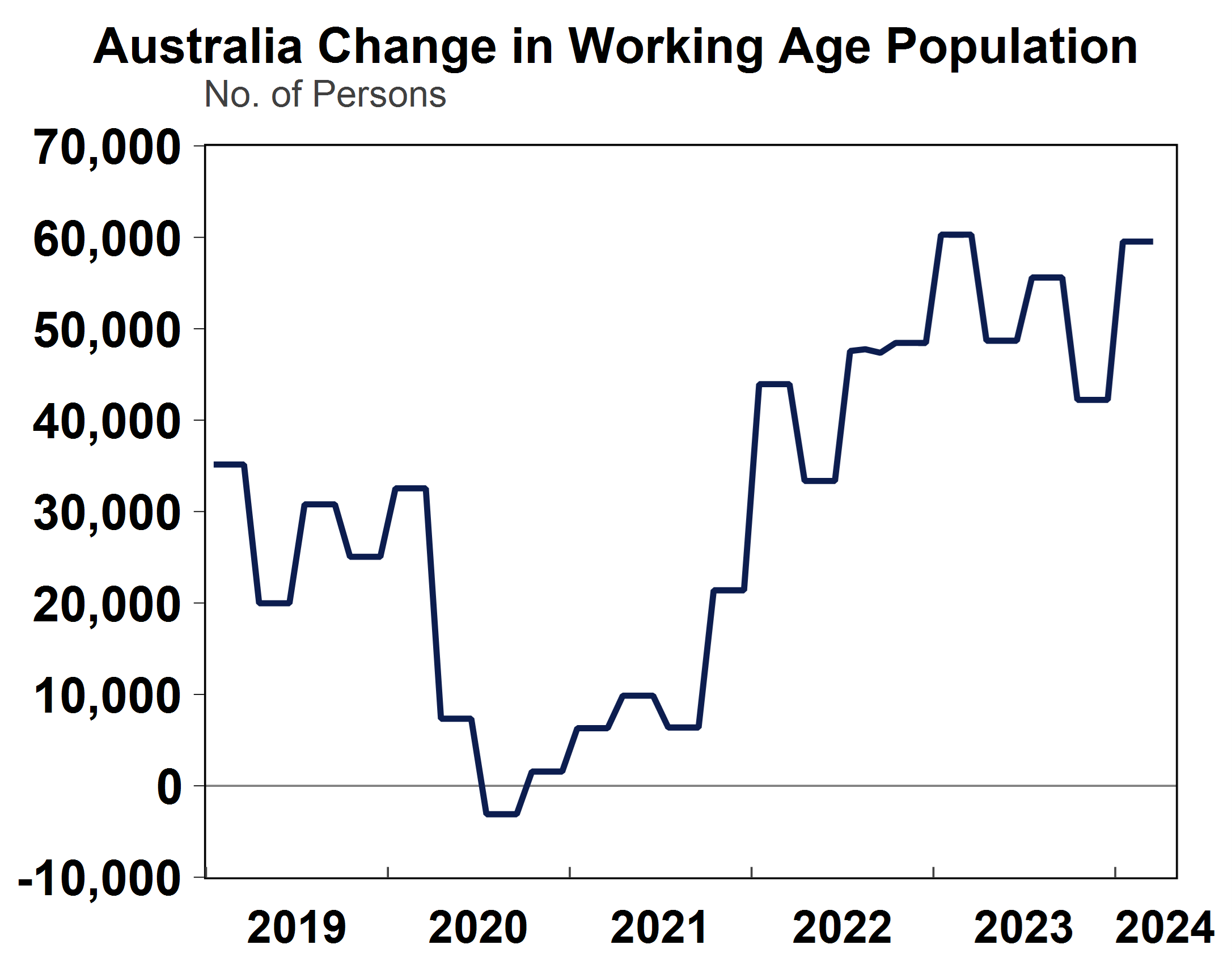

This has resulted in a big inflow of workers into the labour force (the sum of employed and unemployed) every month which is currently running around 60K every month (see the next chart).

Source: Macrobond, AMP

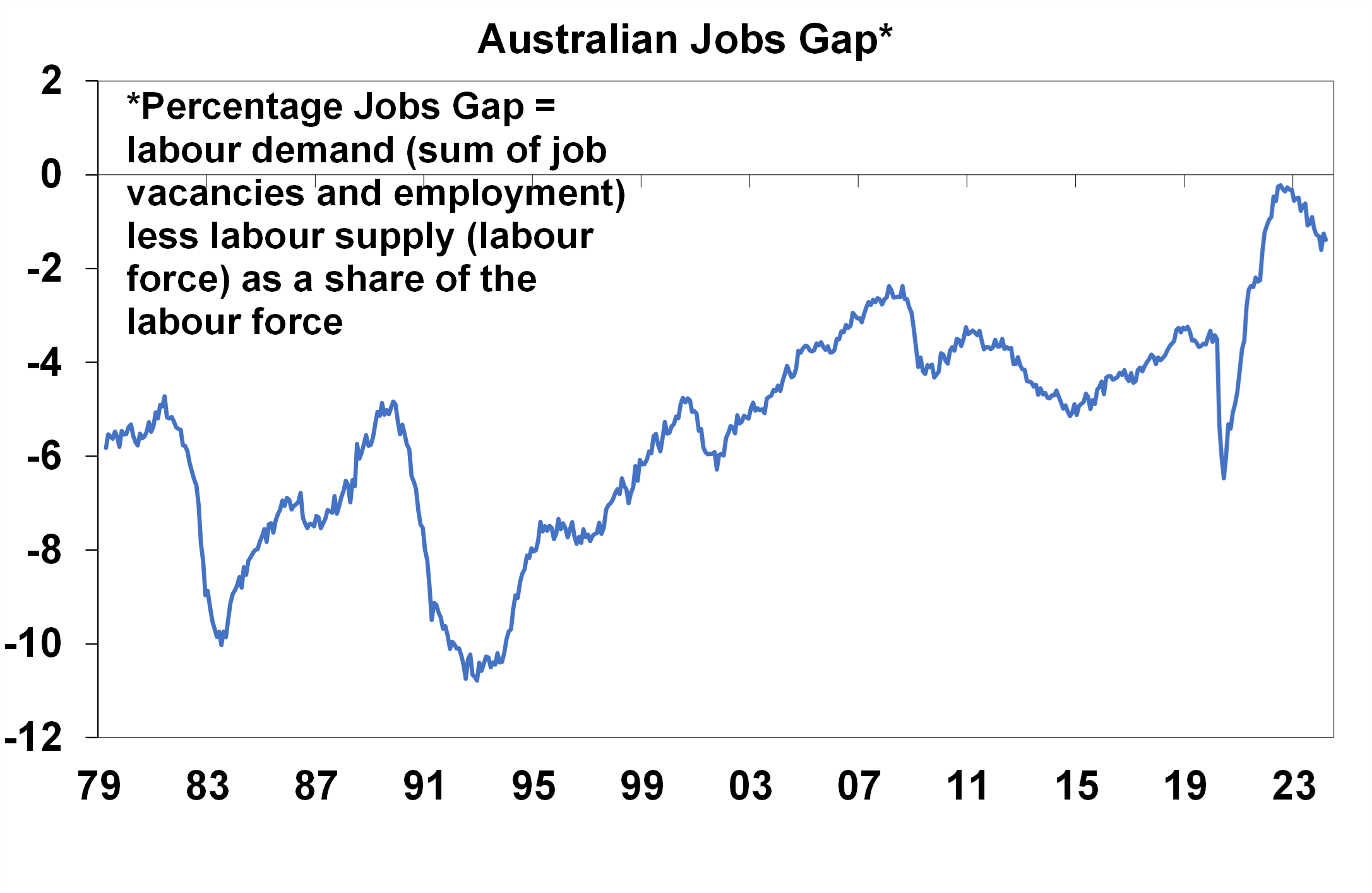

A massive inflow of workers and an increase in the Australian labour force participation rate to a record high (at 67%) has increased labour supply. The pandemic appears to have permanently shifted the labour participation rate higher as more flexibility in the labour market allows a larger pool of workers to better match their skills to a job. Labour demand (a function of employment and job vacancies) has also been strong. In late 2022, labour demand and supply were basically equal (see the next chart) for the first time since 1979 (when the data started) which signals a super tight labour market. Since then, the growth in labour supply has exceeded demand which is resulting in a less tight labour market (i.e. the line in the next chart is moving back down). This is despite continued strong headline jobs growth.

Source: ABS, AMP

We think that the scale of labour market tightness is the best guide to wages growth (and therefore inflation), rather than the headline employment figures which may still look high thanks to high labour supply.

Central banks are also paying more attention to the supply story, particularly as it relates to inflation. Recently, US Federal Reserve Chair Jerome Powell said that the strength in jobs is not necessarily a concern because it reflects the strength in the supply side of the economy.

The other component of supply is capital, which refers to changes in business investment which has also been solid in Australia, especially in plant and equipment and engineering work. Although in Australia, the increase in labour supply has been the more dominant driver of the outward shift in supply.

Implications for investors

We have been too pessimistic about the outlook for Australian consumers partly because we had been looking for a faster unwinding in the labour market and a higher unemployment rate. While Australian consumers are under pressure from high interest rates, elevated inflation and a rising burden from taxes they have been able to offset these negatives by maintaining their wages from employment, as the unemployment rate has remained low. The leading indicators of jobs growth in the business surveys and job vacancies data have slowed but are certainly not collapsing. Yet given the positive labour supply shock that has occurred, you don’t need to see a large fall in jobs to see slower wages growth and some further rise in the unemployment rate. Just to keep the unemployment rate unchanged, employment growth needs to average at 40K/month – this is quite high. Investors should focus on the tightness in the labour market. We think labour supply will outstrip labour demand and see a further slowing in wages growth and a rise in the unemployment rate towards 4.3%, which is still below its pre-pandemic level of over 5%.

Weekly market update 22-11-2024

22 November 2024 | Blog Against a backdrop of geopolitical risk and noise, high valuations for shares and an eroding equity risk premium, there is positive momentum underpinning sharemarkets for now including the “goldilocks” economic backdrop, the global bank central cutting cycle, positive earnings growth and expectations of US fiscal spending. Read more

Oliver's insights - Trump challenges and constraints

19 November 2024 | Blog Why investors should expect a somewhat rougher ride, but it may not be as bad as feared with Donald Trump's US election victory. Read more

Econosights - strong employment against weak GDP growth

18 November 2024 | Blog The persistent strength in the Australian labour market has occurred against a backdrop of poor GDP growth, which is unusual. We go through this issue in this edition of Econosights. Read moreWhat you need to know

While every care has been taken in the preparation of this article, neither National Mutual Funds Management Ltd (ABN 32 006 787 720, AFSL 234652) (NMFM), AMP Limited ABN 49 079 354 519 nor any other member of the AMP Group (AMP) makes any representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided and must not be provided to any other person or entity without the express written consent AMP. This article is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives and does not constitute a recommendation, offer, solicitation or invitation to invest.

The information on this page was current on the date the page was published. For up-to-date information, we refer you to the relevant product disclosure statement, target market determination and product updates available at amp.com.au.